Berkshire Hathaway released 2022 financial results this weekend along with Warren Buffett’s annual letter to shareholders. I recommend reviewing results for any company you own before reading the opinions of others. Here are the materials released this weekend in case you would like to read them before reading this article:

Press Release

Warren Buffett’s 2022 letter to shareholders

Berkshire Hathaway’s 2022 annual report

At just over eight pages, the letter is shorter than last year’s letter and much shorter than letters that shareholders have become accustomed to reading in the past. Although he does highlight a few figures, Mr. Buffett directs those who are interested in “almost endless details” to the discussion of financial results in the annual report.

Berkshire’s approach to communications is to provide detailed information in the annual letter along with a five hour question and answer session at the annual meeting. This is far better than what nearly all public companies provide. Still, I was hoping to read more in the letter about GEICO. As I discussed after the Q3 2022 report was released, GEICO has experienced strong headwinds in recent quarters. My recent profile of Progressive contains a great deal of information about GEICO and the competitive pressures in auto insurance over the past few years.

Andrew Bary, who has been writing about Berkshire for decades in Barron’s, suggests that Berkshire should start holding quarterly earnings calls. I suspect that this will eventually happen, but I prefer very detailed and candid commentary in lengthy annual letters. Perhaps Ajit Jain and Greg Abel will start writing their own letters to shareholders in the future covering their areas of oversight, with Warren Buffett focusing on big picture topics and major capital allocation decisions.

This article highlights aspects of the letter that I found particularly interesting.

Managing Savings for Individuals

The letter begins with Warren Buffett emphasizing that his job is to manage the savings of a great number of individuals, many of whom entrust their funds to Berkshire for “much of their adult lifetimes”.

When I read this section of the letter, I thought of my twenty-three years of Berkshire ownership and calculated that this span accounts for about 47% of my entire lifetime, and 73% of my adult lifetime. My situation is apparently not at all uncommon.

Money Unmasks Humans

Mr. Buffett states that “the disposition of money unmasks humans” which is a message quite similar to my article about how wealth clarifies a person’s character. His point is related to philanthropy, noting with satisfaction that Berkshire shareholders are typically big donors to charity and shun ostentatious lifestyles.

It seems like knowing that shareholders designate much of their wealth to charity is a motivating factor for Mr. Buffett, and that isn’t surprising for a man who has pledged the vast majority of his wealth to philanthropic causes.

Mistakes are Inevitable

After noting that he is tolerant when it comes to business mistakes but intolerant of any personal misconduct, Mr. Buffett admits that he has made “many mistakes” over the years when it comes to capital allocation. He characterizes only a few of Berkshire’s enterprises as having “truly extraordinary” characteristics with “many” that have “very good” economics. Balanced against this are a “large group” of marginal businesses and those that have died completely due to creative destruction.

“At this point, a report card from me is appropriate: In 58 years of Berkshire management, most of my capital-allocation decisions have been no better than so-so. In some cases, also, bad moves by me have been rescued by very large doses of luck. (Remember our escapes from near-disasters at USAir and Salomon? I certainly do.)”

This discussion brings up an important point: it does not take many exceptional decisions to generate outstanding investment results over a long time horizon. It also highlights the folly of “watering the weeds and cutting flowers.” Common investment practices like averaging down on losers and selling winners with the mentality that “one can never go broke taking profits” usually backfires in a big way over time.

“The lesson for investors: The weeds wither away in significance as the flowers bloom. Over time, it takes just a few winners to work wonders. And, yes, it helps to start early and live into your 90s as well.”

Accounting Distortions

Mr. Buffett states that Berkshire had a “good year in 2022” when measured by operating earnings, but GAAP accounting continues to provide highly misleading headlines when it comes to reported net income.

Normally, when a CEO protests that GAAP accounting is masking good results, shareholders should be wary. When companies provide “adjusted earnings” figures, more often than not management is attempting to obfuscate results by persuading shareholders to disregard real operating costs such as stock-based compensation.

In Berkshire’s case, the distortions are due to mark-to-market accounting that requires changes in the value of equity securities to be reflected in net income on a quarterly basis. Last year, I wrote an article explaining this distortion, and Mr. Buffett has clearly explained the situation in past letters. He provides a table illustrating the “acrobatic behavior” caused by mark-to-market accounting:

You would think that this longstanding distortion would cause major newspapers like the Wall Street Journal to focus on operating earnings, but dramatic headlines are what attract clicks. Although the WSJ’s coverage does discuss operating earnings, the headline writer (or editor) couldn’t resist this eye catching formulation:

Mr. Buffett has never suggested that changes in the market value of equity securities do not matter in the long run, only that short term market gyrations have no analytical value. The company provides information on operating earnings to allow shareholders to focus on business performance, and I typically look at trailing twelve month figures to analyze how the business is trending at a high level, as shown in the exhibit below (click on the image for a larger view of the data).

From this perspective, we can see why Mr. Buffett feels like 2022 was a solid year for Berkshire despite the “big loss” caused by market fluctuations in the equity portfolio.

Alleghany and Joe Brandon

Mr. Buffett briefly mentions the Alleghany acquisition which closed in October 2022, noting that Joe Brandon understands Berkshire Hathaway and the insurance industry. I wrote about Alleghany in March 2022 when the acquisition was announced and I suspect that Mr. Brandon could potentially run Berkshire’s insurance operations in the future or help troubled operations like GEICO get back on track.

The annual report explains how Alleghany’s insurance and reinsurance groups have been placed within Berkshire’s insurance operations. Alleghany’s non-insurance operations have been retained with some of the smaller units incorporated into Marmon, which itself is a conglomerate comprised of over a hundred subsidiaries.

Primarily as a result of the Alleghany acquisition, Berkshire’s float increased from $147 billion to $164 billion during 2022. Berkshire’s small underwriting loss in 2022 meant that float was not cost free but Berkshire has consistently delivered cost free float in the past. Mr. Buffett refers to float as an “extraordinary asset” for Berkshire.

Repurchases

Mr. Buffett notes that Berkshire’s share count dropped by 1.2% in 2022 as a result of share repurchases. As I discussed recently, shareholders may logically view this repurchase as an “optional” dividend. A shareholder could sell 1.2% of his or her shares of Berkshire and still retain the same proportional ownership of the company.

Repurchases only create value if they are made at “value-accretive prices”, and if management overpays, continuing shareholders will lose. Mr. Buffett has some uncharacteristically blunt words for politicians who choose to mischaracterize repurchases for their own cynical reasons:

“When you are told that all repurchases are harmful to shareholders or to the country, or particularly beneficial to CEOs, you are listening to either an economic illiterate or a silver-tongued demagogue (characters that are not mutually exclusive).”

Perhaps this comment was prompted by the 1% tax on net repurchases that took effect on January 1, 2023 or by President Biden’s proposal to quadruple the repurchase tax to 4% in the future. More likely, Mr. Buffett is just annoyed by the economic illiteracy that leads otherwise intelligent people to believe that all repurchases are somehow evil.

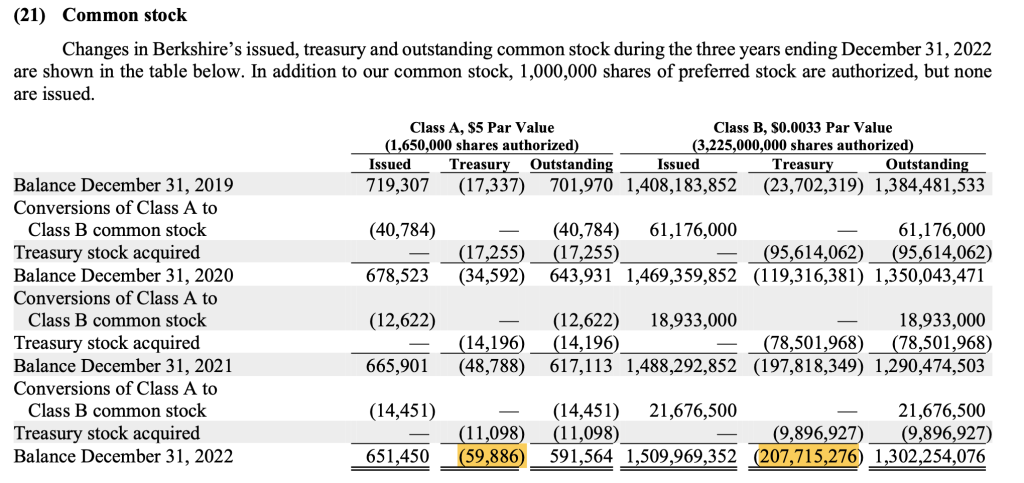

Speaking of repurchases, I updated my spreadsheet containing Berkshire’s entire repurchase history. In 2022, Berkshire retired 17,696 Class A equivalent shares for just over $8 billion, at an average cost of $453,906 per share.

As a validation of my spreadsheet, I refer to Note 21 of the 10-K which confirms the total number of Class A and Class B shares classified as treasury stock.

Berkshire has continued to repurchase shares in 2023. The 10-K reveals that there were 1,458,235 Class A equivalents outstanding on February 13, 2023, a reduction of 1,498 Class A equivalents so far this year. We will not know precisely how much was paid for these shares until the first quarter report comes out in late April or early May.

No Finish Line

Mr. Buffett notes that there is no “finish line” at Berkshire and highlights the broad alignment between Berkshire’s future and the economic future of the United States, stating that Berkshire is the largest owner of eight members of the S&P 500 that earned over $3 billion in 2021:

“In addition to those eight investees, Berkshire owns 100% of BNSF and 92% of BH Energy, each with earnings that exceed the $3 billion mark noted above ($5.9 billion at BNSF and $4.3 billion at BHE). Were these companies publicly-owned, they would replace two present members of the 500. All told, our ten controlled and non-controlled behemoths leave Berkshire more broadly aligned with the country’s economic future than is the case at any other U.S. company. (This calculation leaves aside “fiduciary” operations such as pension funds and investment companies.) In addition, Berkshire’s insurance operation, though conducted through many individually-managed subsidiaries, has a value comparable to BNSF or BHE.”

In the past, both Warren Buffett and Charlie Munger have recommended index funds for most investors as a means of obtaining broad diversification and avoiding excessive management fees. However, it is worth noting that Berkshire Hathaway itself is a broadly diversified conglomerate with very low corporate overhead. Of course, only the future will reveal whether Berkshire’s collection of publicly traded investments and controlled subsidiaries will outperform the S&P 500.

Inflation and Taxes

I don’t think it is an accident that the letter mentions inflation in a section ostensibly about federal taxes because inflation is actually a tax. Mr. Buffett clearly sees the risk of continuing inflation and links this trend to fiscal policy:

“Berkshire also offers some modest protection from runaway inflation, but this attribute is far from perfect. Huge and entrenched fiscal deficits have consequences.”

On taxes, perhaps I am reading too much into this section, but it seems like Mr. Buffett might be annoyed by the populist rhetoric that is increasingly common in Washington these days. He makes an effort to illustrate how Berkshire is a major U.S. taxpayer, contributing $32 billion in corporate income taxes over the past decade which accounts for almost exactly a tenth of 1% of all money collected by the Treasury.

A mental image can be worth a thousand (trillion?) words. Mr. Buffett notes that a million dollars in newly printed $100 bills will make up a stack reaching to your chest. A stack of a billion dollars will reach 3/4 of a mile into the sky. And …

“Finally, imagine piling up $32 billion, the total of Berkshire’s 2012-21 federal income tax payments. Now the stack grows to more than 21 miles in height, about three times the level at which commercial airplanes usually cruise. When it comes to federal taxes, individuals who own Berkshire can unequivocally state ‘I gave at the office.’”

I make it a habit to calculate my “look through” taxes paid via ownership of investments. While many people may scoff at regarding an individual’s proportional burden of corporate income tax in this manner, I view every dollar of “look through” taxes as very real indeed. It’s good to read that Mr. Buffett seems to agree.

Warren Buffett is a lifelong Democrat and is not against paying taxes. It seems like he simply wants there to be some intellectual honesty when it comes to political rhetoric, and is therefore highlighting Berkshire’s contribution to the U.S. Treasury.

“At Berkshire we hope and expect to pay much more in taxes during the next decade. We owe the country no less: America’s dynamism has made a huge contribution to whatever success Berkshire has achieved – a contribution Berkshire will always need. We count on the American Tailwind and, though it has been becalmed from time to time, its propelling force has always returned.”

A Tribute to Charlie

The letter concludes with a tribute to Charlie Munger comprised of a list of fifteen “Mungerisms”, many of which longtime shareholders are already familiar with.

It is great to read that both Warren Buffett and Charlie Munger will be at the annual meeting taking questions for the customary five hours. Let’s hope that this will continue for many more years!

Copyright and Disclaimer

Nothing in this article constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC. This website is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

Individuals associated with The Rational Walk own shares of Berkshire Hathaway.