Accounting changes introduced in 2018 cause wild swings in net income

Accounting rules are supposed to help investors better understand a company’s reported results, not to create confusion. However, sometimes ill-advised rule changes act to muddy the waters and confuse investors, analysts, and reporters.

In 2018, the Financial Accounting Standards Board (FASB) rule known as ASU 2016-01 went into effect. This rule requires that changes in the value of equity securities during an accounting period must be recognized in net earnings. Prior to 2018, only realized gains and losses were recognized in net earnings while unrealized gains and losses were recognized in other comprehensive income. This seemingly technical change has had widespread effects on companies that have large equity securities portfolios.

If the goal of the rule change was to highlight quoted changes in the value of a company’s equity portfolio, it has been a resounding success. However, there are at least two serious problems with the rule change. First, short-term fluctuations in stock prices serve as a poor measure of underlying changes in the business value of an investment. Second, if a company has a large portfolio of equities in addition to operating businesses, changes in the quoted value of the portfolio that are incorporated into net income can obscure the results of the company’s operations.

Berkshire Hathaway’s reported results have long required more in-depth analysis than the average company due to the vast array of operating businesses with different underlying economic characteristics. The effect of ASU 2016-01 has been to make Berkshire’s results very confusing for investors and reporters. Berkshire’s equity portfolio was valued at $327.7 billion on June 30, 2022. Even relatively modest fluctuations in the portfolio can easily overwhelm operating results and render net income useless for analytical purposes.

In his 2017 letter to shareholders, Warren Buffett predicted that the rule change would significantly muddy the waters:

“The new rule says that the net change in unrealized investment gains and losses in stocks we hold must be included in all net income figures we report to you. That requirement will produce some truly wild and capricious swings in our GAAP bottom-line. Berkshire owns $170 billion of marketable stocks (not including our shares of Kraft Heinz), and the value of these holdings can easily swing by $10 billion or more within a quarterly reporting period. Including gyrations of that magnitude in reported net income will swamp the truly important numbers that describe our operating performance. For analytical purposes, Berkshire’s “bottom-line” will be useless.”

Indeed, Berkshire’s “bottom line” net income figure has become totally useless for analytical purposes since 2018. This is true on an annual basis and even more true on a quarterly basis. For this reason, Berkshire has highlighted operating earnings in its press releases, but the majority of media headlines on the company’s earnings continue to focus on net income.

It is very dramatic to write a headline stating that Warren Buffett’s company lost $43.8 billion in the second quarter of 2022. A combination of curiosity and schadenfreude about the “fall” of a well-known billionaire investor can be an irresistible incentive to click on an article. However, a headline highlighting the company’s $9.3 billion of net operating earnings during the quarter would better serve to inform readers about the economic reality of what actually took place.

Berkshire Hathaway announced second quarter results in a press release yesterday and also posted the corresponding 10-Q report which has much more detail. I have spent most of the weekend reading the report and updating Excel spreadsheets.

For this post, I will not attempt to replicate the coverage that is easily found in the news media. Instead, I will focus on the question of how to bring some meaning to Berkshire’s results at a high level, with a focus on quarterly results since 2018. This period spans a time of normalcy prior to the pandemic, the deep downturn of 2020, and the recovery that has taken place since then.1

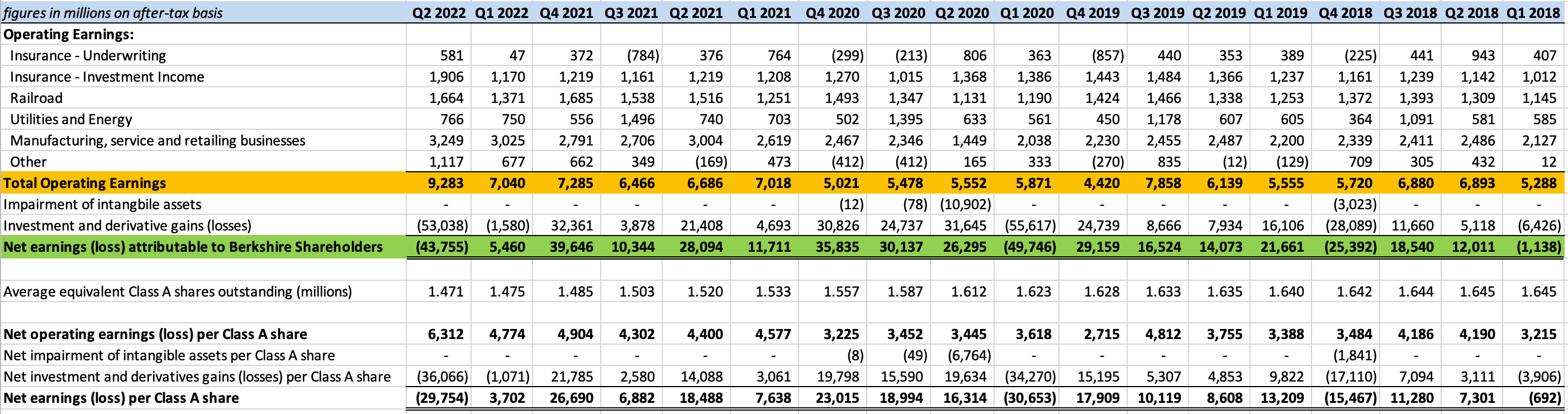

The exhibit below shows quarterly results for Berkshire since 2018. The figures are provided on an after-tax basis (click on the image for a larger view):

The highlighted green row shows the net earnings figure that is widely reported in the news media. The highlighted orange row shows net operating income which serves as a better indicator of how Berkshire’s underlying businesses are performing.

In aggregate, over the eighteen quarters in this exhibit, Berkshire has reported $179.5 billion of net income. This was comprised of $114.5 billion of operating income and $79 billion of investment and derivative gains, offset by $14 billion of non-cash losses attributed to impairment of intangible assets primarily related to KraftHeinz in 2018 and Precision Castparts in 2020.

When you sum up the rows and report the figures as I have in the last paragraph, you have a statement that is not too far from economic reality over the past four-and-a-half years. However, just scanning the figures on a quarterly basis makes it clear that operating earnings are far less variable than net earnings because of the extreme volatility of investment and derivative gains and losses.

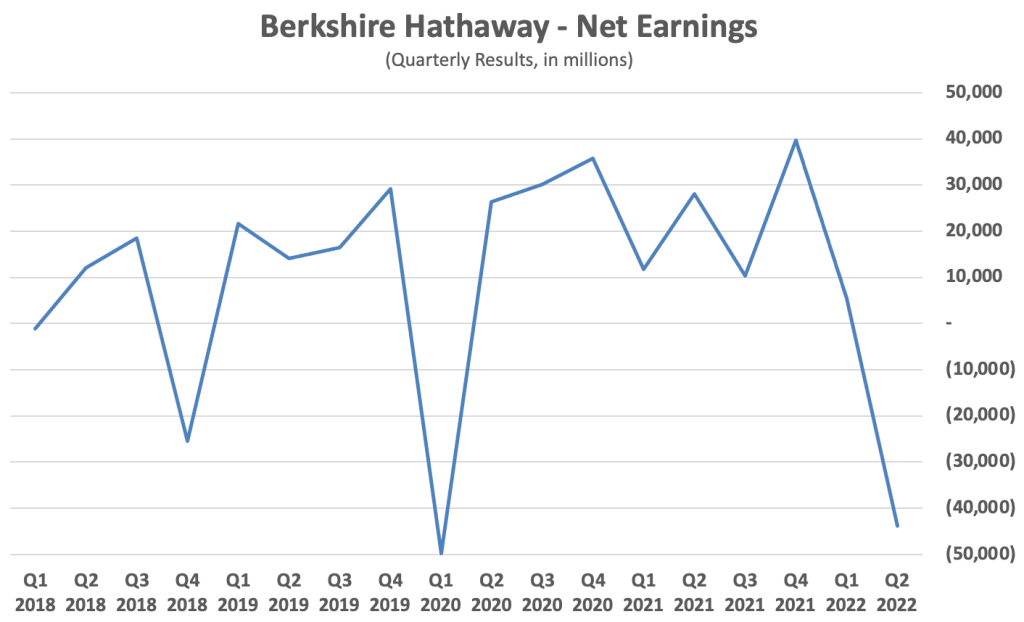

The situation might be better illustrated with a couple of graphs. Let’s take a look at net earnings reported on a quarterly basis:

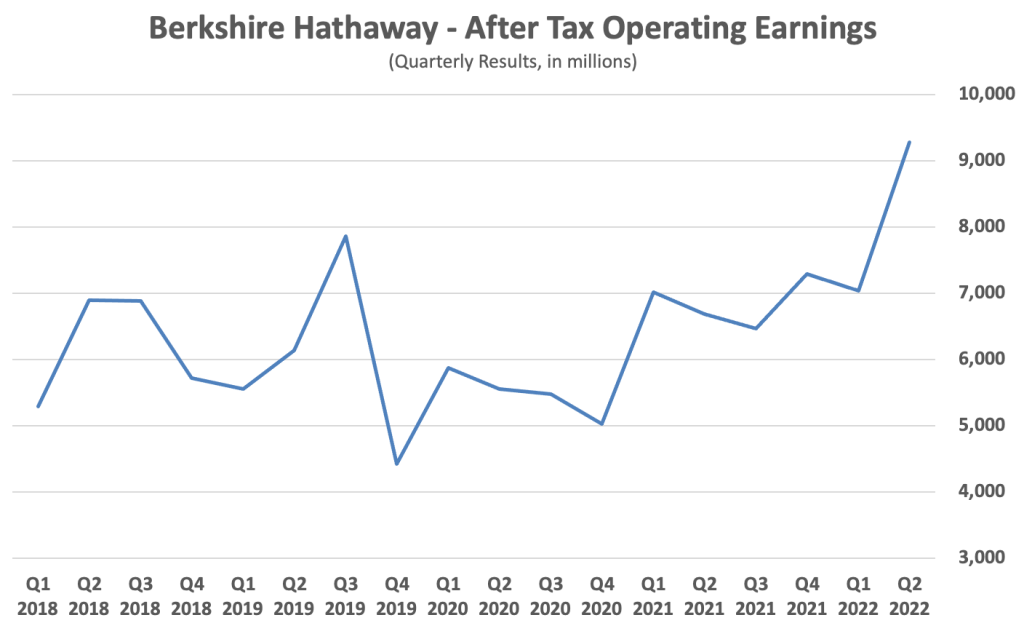

Now let’s take a look at after-tax operating earnings over the same period:

Berkshire’s quarterly operating results can be volatile, but the volatility is caused by the underlying business fundamentals of the operating businesses, not the volatility that is inherent in market quotations of the equity portfolio. Insurance underwriting results are known to swing significantly from quarter-to-quarter. Berkshire Hathaway Energy has higher earnings during the summer months of the third quarter. The manufacturing, service and retailing group was significantly impacted by the pandemic and many also have seasonal variations. But from an analytical perspective, quarterly operating results are still very useful whereas net income drowns in the noise created by the effect of market quotes on the equity portfolio.

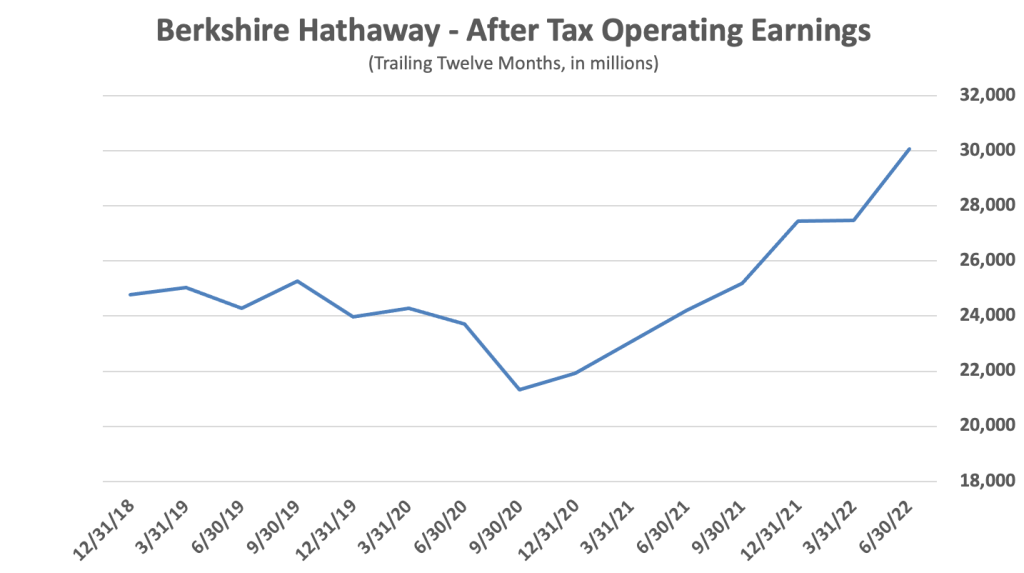

To get a better sense of Berkshire’s operating results, we can look at after-tax operating earnings on a trailing twelve month basis. To arrive at these figures, I have summed the quarterly after-tax operating earnings for the four quarters prior to the date on the x-axis of the chart. For example, the trailing twelve months of after-tax operating earnings for the June 30, 2022 data point adds up the figures for the third and fourth quarters of 2021 and the first and second quarters of 2022.

From an analytical perspective, looking at the trailing twelve month figure for after-tax operating earnings gives us a better sense of how Berkshire’s operating subsidiaries have fared through the pandemic. We can see that the trailing twelve month results hit a trough in the third quarter of 2020 and began a steady recovery and now surpasses pre-pandemic levels.

The point of this article is not to suggest that we should ignore the performance of Berkshire’s large portfolio of equity securities.

The performance of the businesses represented by these equity securities is extremely important for Berkshire in the long run and we should examine the equity portfolio’s quoted value, but over a number of years, not every quarter.

The issue is that quarterly swings in stock prices convey almost no useful information. The fact that these huge swings impact Berkshire’s net income on a quarterly basis mislead many investors and reporters and encourage dramatic “click-bait” headlines.

It would make far more sense for headlines to discuss Berkshire’s after-tax operating results followed by a longer term assessment of the equity portfolio. Berkshire provides the data needed to do a better job of reporting on the company’s results, but for some reason confusion still reigns. Barring a reversal of the FASB rule, investors will just have to look past the headlines to understand Berkshire’s performance.2

I might write another article on certain aspects of Berkshire’s results over the next few days. My overall assessment is that the company’s operating subsidiaries are generally performing well, although I do have some concerns in a few areas. For example, GEICO appears to be struggling relative to Progressive’s recent results. If I write another article, the majority of it will be restricted to paid subscribers.

As an aside, Berkshire Hathaway Energy (BHE) purchased Greg Abel’s 1% interest in BHE for $870 million in June. In April, I wrote How Berkshire Could Deploy $6 Billion which discussed the possibility of Berkshire acquiring Mr. Abel’s 1% interest in BHE. The 8% BHE interest held by the estate of Walter Scott Jr. might also be repurchased at some point although the company has not announced any plans to do so. The article was originally paywalled, but I have now made it available for everyone to read.

Copyright, Disclosures, and Privacy Information

Nothing in this newsletter constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.

Your privacy is taken very seriously. No email addresses or any other subscriber information is ever sold or provided to third parties. If you choose to unsubscribe at any time, you will no longer receive any further communications of any kind.

The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

Individuals associated with The Rational Walk own shares of Berkshire Hathaway and Markel Corporation.

- In March 2020, I wrote Berkshire Hathaway and the Coronavirus Crash in which I attempted to assess how Berkshire’s subsidiaries would fare during the pandemic. Readers might find that article interesting in conjunction with results that have been reported since then. [↩]

- Berkshire is not the only company facing the distortions caused by the rule change. For example, Markel Corporation’s second quarter results were also impacted by unrealized losses in its equity portfolio. Markel’s net income is just as useless as Berkshire’s for analytical purposes. [↩]