Introduction

Berkshire Hathaway shareholders are eagerly awaiting Warren Buffett’s annual letter which will be released on Saturday, February 25. One of the perennial questions many shareholders ask is when Berkshire will begin paying dividends. Other than a ten cent per share dividend that Berkshire paid in 1967, the company has never paid a dividend to shareholders since Warren Buffett took control in 1965.

I have written about return of capital at Berkshire Hathaway several times over the years. Warren Buffett has made it clear that he regards retaining earnings to be his preferred strategy. On occasions when Berkshire has had excess cash, Mr. Buffett has returned cash to shareholders through stock repurchases rather than dividends.1 As of the end of the third quarter of 2022, Berkshire has distributed a cumulative total of nearly $65 billion through repurchases, with over 97% of that sum allocated since August 2018 when Berkshire eased its self-imposed rules for repurchases.2

It is not likely that Berkshire Hathaway will initiate a regular dividend while Warren Buffett is involved in managing the company. There are reasons to believe that a large majority of shareholders do not support a dividend, at least as long as Mr. Buffett in charge. In 2014, a vote was taken on a proposal to establish a dividend and 98% of shareholders rejected the idea. While the vote against a dividend was larger among Class A shareholders, Class B shareholders were also overwhelmingly opposed.3 There is no reason to believe that a vote taken today would have a different outcome.

Should Income Investors Look Elsewhere?

Should income oriented investors avoid Berkshire Hathaway due to the lack of a regular quarterly dividend? While it is true that owning Berkshire Hathaway will not result in cash landing in your brokerage account every three months, that does not necessarily mean that it is impossible to generate income from owning the stock.

Investor psychology can be a major impediment to rational behavior. Most people engage in various forms of “mental accounting” which involves attaching meaning to specific buckets of money. In the case of common stocks, it is typical for investors to view the amount they invest in a stock as principal and dividends received as income. Such an investor will happily spend dividend checks but recoils at the prospect of selling shares to raise cash because doing so would be an “invasion of principal.”

The instinct behind this attitude is not wrong in the sense that encroaching on one’s base of capital is generally undesirable through most of an individual’s investment lifecycle. Invading principal can lead to a downward spiral and deplete a portfolio prematurely before an individual’s goals are fully met. This is obviously a bad outcome.

But it is a mental error to assume that distributions from a company represent income that can be freely spent and that selling shares is always irresponsible. Plenty of failing companies cannot cover a longstanding dividend with cash flow and have been known to borrow to maintain a dividend for as long as possible. Dividends funded from borrowing are surely just as much of an invasion of principal as selling shares.

The policy of a corporation when it comes to retention or distribution of capital depends on reinvestment opportunities. Capital should be retained if sufficient opportunities for reinvestment exist at attractive rates of return. Distributions should be made if there is no attractive place to allocate the capital.

Rather than demand a suboptimal capital allocation policy from the corporation, shareholders who need to periodically draw funds from their investment in Berkshire should instead reframe their thinking. Of course, this is easier said than done. Fortunately, we have a guidepost for how to structure a drawdown strategy based on how Warren Buffett has chosen to distribute his stock to charitable foundations.

Buffett’s 5% Approach to Charitable Gifts

Warren Buffett’s plans to distribute his Berkshire Hathaway shares to charity were formalized in a series of letters that he wrote to charitable foundations in June 2006. I covered Mr. Buffett’s philanthropic record in great detail in an article last year so I will not reiterate all of the terms of his gifts here. The feature of his giving program that could shed light on an income producing drawdown strategy has to do with the mechanics of his share distributions.

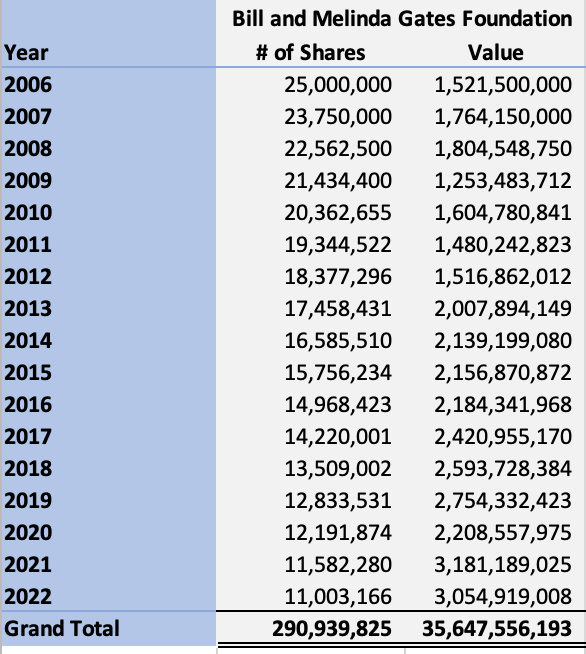

Let’s take Mr. Buffett’s gifts to the Gates Foundation as an example since it represents the largest pledge. In his letter to the Gates Foundation, Mr. Buffett explained that 500 million Class B shares had been earmarked for contributions (all figures are adjusted for the 50-for-1 split of the Class B shares in 2010). Every year, 5% of the balance of the earmarked shares would be contributed to the foundation.

For example, in 2006, 5% of the initial 500 million share pool, or 25 million shares, were donated. In 2007, 5% of the remaining 475 million shares in the pool, or 23,750,000 shares, were donated. We can see how this continued over the years in the exhibit below.4

Even though the number of shares donated to the Gates Foundation dwindled over the years, the market value of those shares has increased substantially, albeit with significant variation on a year-to-year basis. This outcome is exactly what Mr. Buffett expected when he made the following statement in his 2006 letter to the foundation:

“The value of Berkshire shares will, of course, vary from year to year. And, as noted, the number of shares distributed will diminish by 5% per year. Nevertheless, I believe that you can reasonably expect the value of Berkshire shares to increase, in an irregular manner, by an amount that more than compensates for the decline in the number of shares that will be distributed.”

The value of the donation of 11,003,166 shares in 2022 was almost exactly double of the value of the initial donation of 25,000,000 shares in 2006. This is because the market value of Berkshire Hathaway’s shares has increased at a rate far in excess of the 5% annual depletion. Over a very long period of time, Mr. Buffett’s prediction was exactly on target although sharp-eyed readers will note that there were four years when the value of the donation declined, most precipitously between 2008 and 2009.

We are dealing with nominal dollars in the exhibit and we should be concerned with real dollars. The nominal value of the 2022 donation was $3,055 million which translates to $2,092 million 2006 dollars based on the BLS CPI Calculator. This is comfortably ahead of the $1,522 million value of the actual donation made in 2006. On both a nominal and real basis, the value of Mr. Buffett’s gifts to the Gates Foundation has increased over sixteen years despite the number of shares donated declining every year as the total pool of shares declined.

Of course, this happy outcome was not preordained. It happened because Berkshire compounded its intrinsic value at a rate far in excess of 5% and the market price reflected this increase in value, albeit on an irregular basis. Over time, the Gates Foundation has been able to rely on an annual influx of cash with increasing purchasing power even as the number of shares donated declined every year.

Creating a Dividend

Assuming that Berkshire Hathaway continues to grow its intrinsic value over long periods of time, shareholders should be able to replicate Mr. Buffett’s approach to charitable giving by creating their own personal “dividend” every year. From an individual perspective, the “pool” of shares could be the total number of shares one owns or a subset of shares if there is a desire to keep a certain number in reserve.

For example, consider a shareholder who owns 6,000 Class B shares and would like to create a “dividend” by liquidating a portion of shares every year. This individual’s “pool” starts out with 6,000 shares and the first year’s liquidation will be 300 shares (5% of the 6,000 share pool). In the second year, there will only be 5,700 shares remaining in the pool so the liquidation will fall to 285 shares (5% of the 5,700 share pool). As time goes on, the pool of shares will dwindle, but because the percentage drawdown of the pool is fixed at 5%, the pool will never be totally depleted.

Of course, this plan depends on Berkshire Hathaway’s intrinsic value increasing at a satisfactory rate, and the future could very well bring results that are more modest than what we have experienced in the past. For this reason, a conservative shareholder may elect to use a lower percentage such as 3%. In this scenario, the first year’s liquidation would be only 180 shares (3% of the 6,000 share pool), the second year’s liquidation would be ~175 shares (~3% of the remaining 5,820 share pool), and so on.

Let’s take a hypothetical example of what this strategy would look like assuming a starting pool of 6,000 shares of Berkshire Hathaway Class B. Each year, 3% of the remaining pool of shares will be sold. Assume that the shares are sold for $300 in 2023 and that shares appreciate by 6%, on average, over the next twenty years.

Note that I am not suggesting that today’s intrinsic value is $300/BRKB or that one can expect 6% average appreciation in the future — these are just hypothetical examples benefiting from round numbers.

The exhibit below shows how this self-made 3% dividend would look like over the next twenty years given this set of assumptions. (I have left fractional shares in the exhibit for the sake of transparency but one would round to the nearest full share in practice.)

We can see that the value of the “dividend” increases over time, although its value in real terms would depend on the rate of inflation over this two decade period. The value of the dwindling number of shares remaining in the pool also increases over time. Obviously, in practice, this would not work out as neatly as this hypothetical example. The shareholder would need to accept a lower “dividend” if the share price declines in a given year or be willing to liquidate more shares from the pool.

One objection to this plan is that the “dividend” will fluctuate in an unpredictable manner. However, this only highlights in concrete terms what is true beneath the surface in most businesses, even those that maintain a stable or rising dividend come hell or high water. Except for the most stable of businesses, underlying economic results will vary over time whether management declares a stable dividend or not.

We should not ignore the important tax benefits that a “self-made dividend” generates compared to a traditional dividend. In our example, the shareholder will only pay taxes on capital gains, not on the entire amount of the annual liquidation. For example, if the cost basis on the 6,000 shares is $150, only half of the first year’s liquidation will be subject to taxes, not the entire amount. This advantage will continue in future years, although as the share price appreciates, more of the liquidation will be taxable every year since the realized capital gain will be larger.

Psychological Impediments

Many investors might consider the logic of this strategy to be sound but still find it psychologically difficult to actually sell shares. It feels like “invading principal” to do so, and there is no arguing with the fact that the number of shares owned will decline.

A confession: I am subject to this psychological impediment just as much as anyone else, especially near round numbers of shares! However, part of being a rational person is understanding when a psychological impediment makes no sense and to make efforts to overcome emotions rather than to be ruled by them. At least when I am being irrational, I usually know that I am being irrational and try to correct for it.

A partial cure for the psychological block associated with a declining number of shares is to consider the effect of share buybacks on Berkshire’s total share count. When Berkshire Hathaway, or any company, is a net repurchaser of stock, total shares outstanding will decline. For example, Berkshire’s share count declined by 5% in 2020 and 4.3% in 2021 due to significant repurchases.

A shareholder who is creating a dividend based on the example above could deal with the psychological impact of owning a smaller number of shares by knowing that his or her percentage interest in Berkshire Hathaway actually increased during 2020 and 2021. The shareholder owned 3% fewer shares at the end of each year, but the total number of shares outstanding declined at an even faster rate.

This brings up an ancillary point that is worth noting: Whenever Berkshire Hathaway makes share repurchases, a shareholder can sell an equivalent number of shares on a percentage basis without reducing his or her percentage ownership in the company. This is a way of turning a share repurchase into a personal “special dividend” as opposed to a personal “regular dividend” as outlined in this article.

Conclusion

Shareholders are unlikely to wake up on February 25 to read that Warren Buffett has decided to declare a dividend. While not impossible, I would put the odds of such an action in the low single digit percentage range (some would say that the odds are a fraction of one percent!). Nevertheless, any shareholder can create their own dividend. Better yet, we have a roadmap of how to structure such a “dividend” based on how Warren Buffett has been distributing shares to charity over the past sixteen years.

While it is true that many shareholders will have psychological issues with taking any action to “invade principal” and might recoil with horror at seeing a smaller number of shares on a brokerage statement, sound and rational corporate policy cannot be based on irrational feelings and emotion. Warren Buffett does his best to provide clear communications in his shareholder letters and cannot cater to irrational emotions.

A day will eventually come when Berkshire Hathaway will justifiably declare a cash dividend. The company could be flooded with cash and the share price might be trading at a level that is far above intrinsic value. Lacking opportunities to usefully deploy the cash, management could decide to distribute it to shareholders. There is nothing inherently wrong with cash dividends, but so far at least, shareholders of Berkshire Hathaway have been well served by a policy of retention of most earnings with return of capital done through stock repurchases rather than dividends.

Copyright and Disclaimer

Nothing in this article constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC. This website is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

Individuals associated with The Rational Walk own shares of Berkshire Hathaway.

- Until this year, repurchases could be made free of any corporate tax consequences. Starting in 2023, a 1% excise tax is imposed on net corporate share repurchases. While a 1% excise tax is unlikely to impact boardroom decisions, new taxes rarely stay at “low” rates for very long. President Biden recently proposed quadrupling the rate to 4%. [↩]

- I have periodically published a table showing Berkshire’s historical repurchase activity. The most recent table is included in my post on Berkshire’s Q2 2022 Results in the “Share Repurchase Activity” section. [↩]

- Warren Buffett wrote about the vote at the end of his 2014 letter to shareholders. The shareholder who made the proposal did not show up at the meeting so it was not officially voted on. However, the votes were tallied anyway and reported in the shareholder letter. [↩]

- The data in the exhibit is from Buffett’s Philanthropic Record, published on June 15, 2022. That article contains a link to an excel file which, in turn, contains links to the underlying SEC source files which forms the underlying data for the consolidation in the exhibit. [↩]