The basic format of Berkshire Hathaway’s annual meeting has remained unchanged for decades. CNBC’s Warren Buffett Archive has annual meeting videos dating back to 1994 and it is interesting to see how the principles expressed by Warren Buffett and Charlie Munger have hardly changed. In 2020, Mr. Buffett sat alone in an empty convention center and was more subdued than usual. He clearly gets his energy from an audience which was denied to him due to the pandemic.

In 2021, Mr. Buffett was joined by Charlie Munger, Greg Abel, and Ajit Jain, but again did not have a live audience. The 2022 meeting brought all four men back to Omaha where shareholder questions were asked for about five hours in front of a live audience.

To a greater extent than in prior years, Mr. Buffett spoke on various topic for extended periods of time which limited the number of questions that could be asked. I counted a total of twenty-two questions which is less than half of the number of questions typically asked at a Berkshire meeting. But we should keep things in perspective. Few companies provide even a small fraction of the time for Q&A, and Mr. Buffett’s extended monologues were generally informative.

I posted a number of thoughts about the Q&A session on Twitter in the form of a long thread that you can read in its entirety as a formatted PDF file.

The first eighteen tweets are related to Berkshire’s first quarter 10-Q. After that, the tweets are related to the Q&A session.

In this article, I will expand on ten highlights of the annual meeting that I first noted in tweets. The first eight of the highlights will be available to all readers. The final two highlights will be limited to paid subscribers and will include a more extended discussion related to succession and share repurchases.

Bonus content for paid subscribers also includes a spreadsheet with Berkshire’s full history of repurchases since 2011 along with related data and calculations.

#1: No Master Plans

Warren Buffett’s latest shareholder letter indicated that he saw few opportunities to deploy Berkshire’s large pile of cash other than continuing the share repurchase program. However, shortly after the letter was released, Mr. Buffett started deploying Berkshire’s cash in earnest.

Mr. Buffett noted that his annual letter is usually written long before it is released to shareholders. His attitude toward deploying cash has always been opportunistic in nature. It is interesting to see how fast he is willing to act when opportunities arise.

On the day before the annual letter was released, Mr. Buffett received Alleghany’s annual report and a letter from CEO Joe Brandon. This started the process for Berkshire to deploy $11.6 billion by agreeing to purchase Alleghany. Mr. Buffett’s decision to begin purchasing Occidental Petroleum common stock originated from reading an investor presentation over the weekend of February 26-27.

A lesson we can learn from Berkshire’s deployment of cash in March is that there are no master plans. Cash is deployed in negotiated transactions or in financial markets when opportunities arise. Mr. Buffett’s ability to act quickly on his own authority is an advantage. Later in the day, Mr. Buffett acknowledged that there will be somewhat more structure in terms of board involvement after he is no longer CEO.

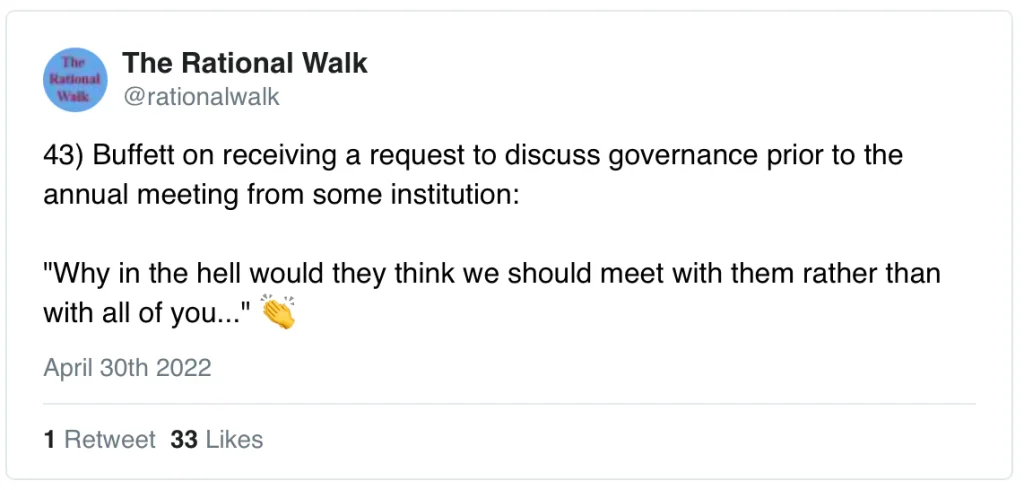

#2: No Preferential Access

There were several shareholder proposals presented at the formal annual meeting which took place after the Q&A session. Mr. Buffett was clearly irritated by several of the proposals, but most likely was particularly perturbed by the proposal to split the Chairman and CEO positions. He indicated that certain institutional shareholders approached him prior to the annual meeting seeking private discussions:

One of the best aspects of owning Berkshire Hathaway is that individual investors can be confident that management is not favoring powerful shareholders over ordinary individuals. One could say that Mr. Buffett refused to meet with these institutions because he didn’t like what they were proposing, but the reality is that he will not meet with any institution. All shareholder communication occurs openly and in public. This is no small advantage for individuals with limited power.

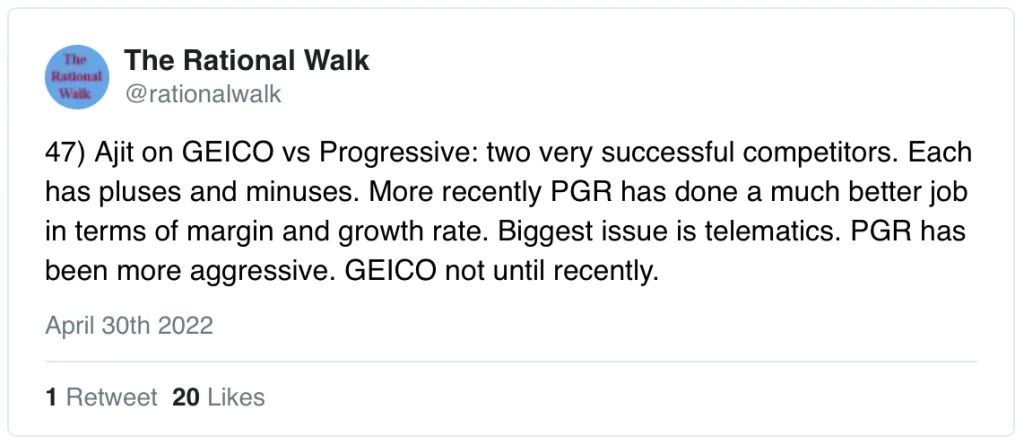

#3: Is GEICO Losing Ground to Progressive?

One of the questions had to do with whether BNSF and GEICO are losing ground relative to their main competitors. These questions were directed to Greg Abel, Vice Chairman of non-insurance operations, and Ajit Jain, Vice Chairman of insurance operations. I found Mr. Jain’s comments on GEICO very candid:

Recently, I wrote an article about competition in the auto insurance industry with a focus on Progressive and GEICO. One of the advantages Progressive appears to have is that its loss ratio is consistency lower than GEICO, perhaps because their introduction of what Mr. Jain refers to as “telematics”. Many years ago, Progressive introduced its snapshot program which allows policyholders to voluntarily opt into driver monitoring in exchange for potentially lower rates. GEICO was initially slow to adopt a similar approach.

GEICO has long had an advantage in its low expense ratio relative to Progressive, but a reluctance to embrace technology has hurt GEICO overall. I liked the fact that Mr. Jain did not, in any way, attempt to minimize the mistake. What I would have liked to hear more about is the long term leadership strategy at GEICO. Todd Combs, whose main job is to run part of Berkshire’s investment portfolio, has been CEO of GEICO for over two years. It seems like Mr. Combs is holding two very demanding jobs and, in the long run, I am curious to know which one he will focus on exclusively.

Mr. Buffett ended this discussion by acknowledging Ajit Jain’s contributions to Berkshire over many decades. It’s hard to imagine a stronger vote of confidence:

#4: Learning from Experience

I do not recall whether Charlie Munger’s comment was in response to an actual question or one of the many digressions that took place during the meeting:

This is one of those lines that gets some laughter and applause and then everyone moves on. But the meaning is quite profound. Warren Buffett made a similar comment about how you should aim to be a better person in the second half of your life than in the first half based on accumulated life experience.

Although they did not exactly say so, I think that this idea has to do with compounding and exponential growth. Not in terms of compounding monetary wealth but compounding wisdom through experience. As we get older, we accumulate more and more information due to direct experience in the world.

The impact of this additional knowledge on our level of worldly wisdom should not be merely additive. It should be exponential. If we have developed enough mental models in multiple disciplines, gaining exposure in a new area exposes interconnections with other disciplines and unlocks even greater wisdom.

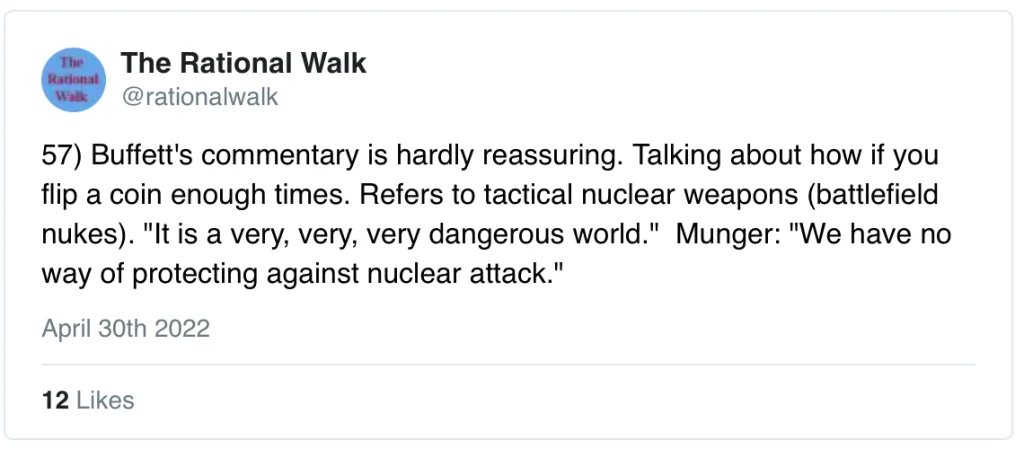

#5: Nuclear War Risks

For some reason, few people seem to want to face up to the reality of nuclear war risks much less discuss them in public. So it was interesting to listen to both Warren Buffett and Charlie Munger directly talk about Berkshire’s inability to deal with the risk of nuclear incidents:

Ajit Jain also made several comments regarding nuclear risks including the reality that governments are likely to force insurance companies to cover losses even if nuclear risks are excluded from policy terms. But that may be the least of our concerns.

As usual, Charlie Munger gets to the heart of the issue in just a few words:

Although the war between Russia and Ukraine was not addressed during the meeting, the references to nuclear risks were clearly directly related to the war.

I personally do not believe that financial markets can “price in” nuclear war risks in any coherent way. Preventing nuclear war is within the realm of our political process and outside the scope of what business leaders can plan for. In the event of nuclear war, survivors will have to rely on whatever governments remain to serve as insurers of last resort.

#6: Best Inflation Hedge is Human Capital

A shareholder asked a question about how to best deal with the risk of inflation. This was a timely question given recent inflationary trends in the United States. I am not sure whether Warren Buffett’s response was what the shareholder was looking for, but I think he made a very good point:

For most people, their most important “asset” when it comes to dealing with inflation are the skills they bring to the table. An individual with high competency in skills that are always in demand will have pricing power that allows their pay to rise along with the cost of living. So, the advice makes a great deal of sense, especially for people who have limited financial assets because they are young.

What Mr. Buffett said about human capital really extends to companies as well. The key thing is to have a unique value proposition that can be offered to customers. The pricing power of an individual is the wage he or she can command in the market. The pricing power of a company is the price that can be charged for goods and services.

#7: Avoiding Politics

A shareholder asked Warren Buffett about the appropriate role for companies and executives when it comes to controversial political issues. Mr. Buffett acknowledged the timeliness of the question and said that he was stepping back from politics to avoid hurting employees and shareholders:

As I listened to Mr. Buffett’s answer, I was nodding in agreement and pleased with the fact that he was no longer planning to weigh in on political issues. In the past, Mr. Buffett would always say that his role as a citizen doesn’t get placed into a blind trust simply because he is CEO of Berkshire. From time to time, he would weigh in on contentious political topics, even lending his name to a tax proposal during the Obama administration called “The Buffett Tax”.

However, as I further reflect on what he said, I cannot help but feel some disappointment that society has reached the point where a man as intelligent as Warren Buffett cannot engage in the political process without fear of harming employees and shareholders.

This morning, I thought of Mr. Buffett’s 2015 Wall Street Journal op-ed, Better Than Raising the Minimum Wage, which was an exceptionally well thought-out proposal for an expanded earned income tax credit.

As a shareholder of Berkshire Hathaway, I am pleased with Mr. Buffett’s decision to step back from politics under today’s conditions. But as a United States citizen, I feel a sense of loss that we will no longer benefit from the ideas he brought to the political process.

#8: Why Berkshire Hathaway Energy Uses Debt

A shareholder asked a question regarding Berkshire Hathaway Energy’s use of debt and was concerned that the debt level was too high. Mr. Buffett’s response was surprising to me:

Although I have followed Berkshire Hathaway Energy since Berkshire bought it, I have never delved into the regulatory issues in much detail. Utilities are very highly regulated and must satisfy rate setting boards in a complicated process. Apparently, the cost of equity capital and debt capital are factors that directly control the rates that customers must pay. Because the cost of debt has been so low in recent years, regulators want utilities to use debt in order to keep rates low for consumers.

Running BHE on an all-equity capital structure probably does not make much sense on its merits. But even if Berkshire wanted to do so, they would not be allowed to.

#9: Succession Planning

For the second year, Vice Chairmen Ajit Jain and Greg Abel appeared on stage with Warren Buffett and Charlie Munger. However, the Q&A was really dominated by Warren Buffett this year and there were few opportunities for Mr. Jain and Mr. Abel to chime in. Mr. Abel was asked questions about the performance of BNSF compared to Union Pacific and Mr. Jain was asked about GEICO, as I noted earlier. Mr. Abel also spoke about cyber-security risks and Mr. Jain commented on nuclear risks.

There were a couple of key points that I found interesting related to management succession. First, a shareholder asked a question very similar to the point that I raised last week in a subscriber-only article about the possibility of Berkshire Hathaway buying out the minority interests of BHE, which includes Greg Abel’s 1% stake and the Scott estate’s 7.9% interest.

Mr. Munger was first to respond to the question of Mr. Abel’s ownership of BHE and the incentive issues this might cause:

This confirms the impression that I have had ever since Mr. Abel was named as Mr. Buffett’s successor. But it is worth noting that Mr. Munger has also been very vocal about always looking at incentive structures when it comes to setting up organizations. Is it a good idea to have a sub-optimal incentive structure even if it happens to work in this case? Or should Berkshire seek to align Mr. Abel’s interests with the overall company rather than just with BHE?

Mr. Buffett seemed to leave the door open to acquiring the minority interests of BHE, but he said that he would not make the first move:

As I mentioned last week, Berkshire Hathaway actually has the power to compel Mr. Abel to sell his interest, but Mr. Buffett would never actually exercise that power, for obvious reasons. However, if Mr. Abel approaches Mr. Buffett, it is possible that they will come to an agreement. The door has clearly been left open for this to happen, but it is going to be up to Greg Abel to step through the door.

My editorial comment after this question still sums up my point of view:

There was one other question related to succession that I think is worth noting. It had to do with how quickly Mr. Abel will be able to move on acquisition opportunities:

It seems likely that the days of Berkshire’s CEO coming up with an idea over a weekend and being able to act on it with minimal board oversight will come to an end. This is not necessarily a bad thing. Mr. Buffett is a unique individual, and it would not be a great precedent for Berkshire’s board to take a totally hands-off approach when it comes to Mr. Buffett’s successor. Nevertheless, the reduced agility of Berkshire’s next CEO could be viewed as a potential risk when it comes to acting on deals quickly.

#10: Repurchase Update

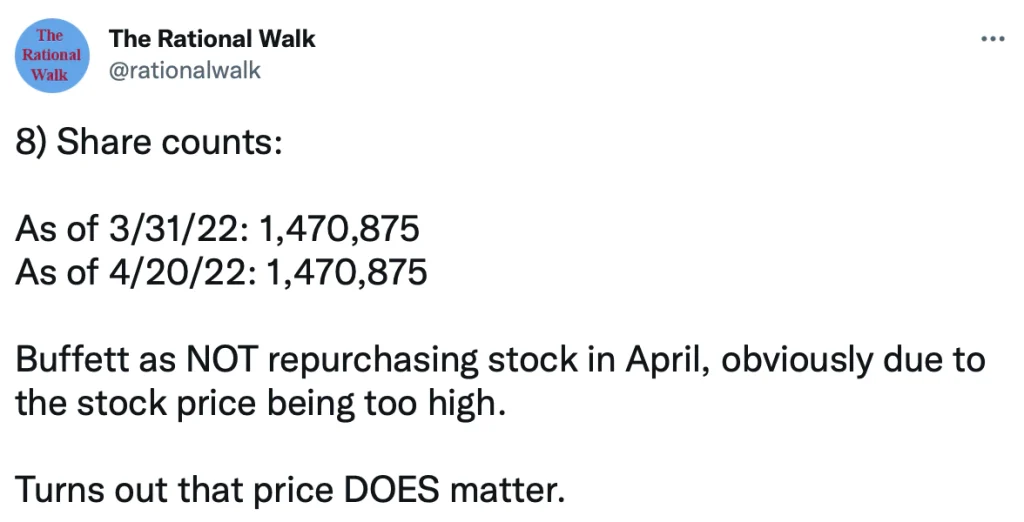

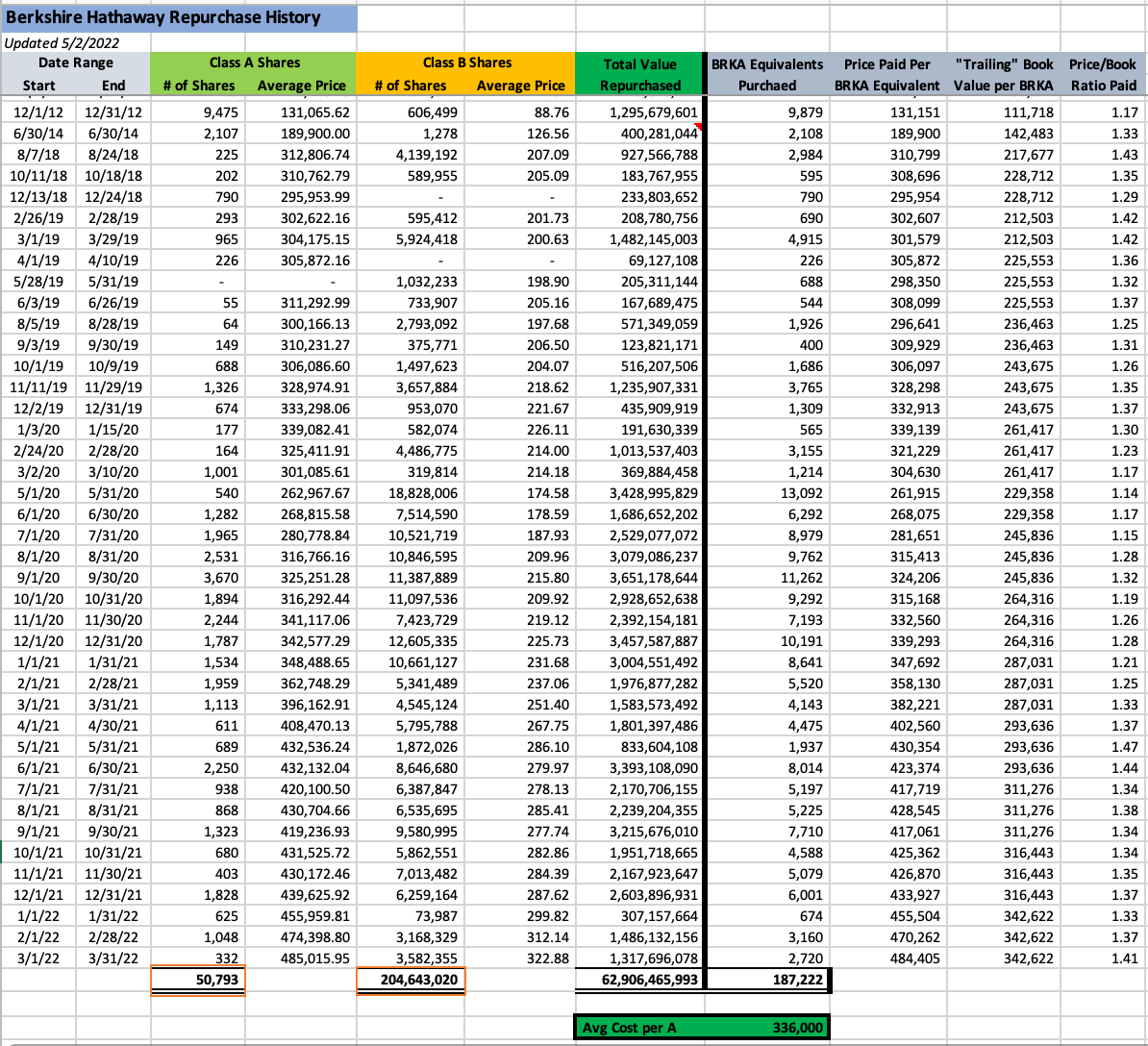

The quarterly report came out just an hour before the Q&A session began, but I did have time to look at it briefly. The first thing I looked at was the share count as of March 31 and compared it to the share count reported on the first page of the 10-Q which was as of April 20.

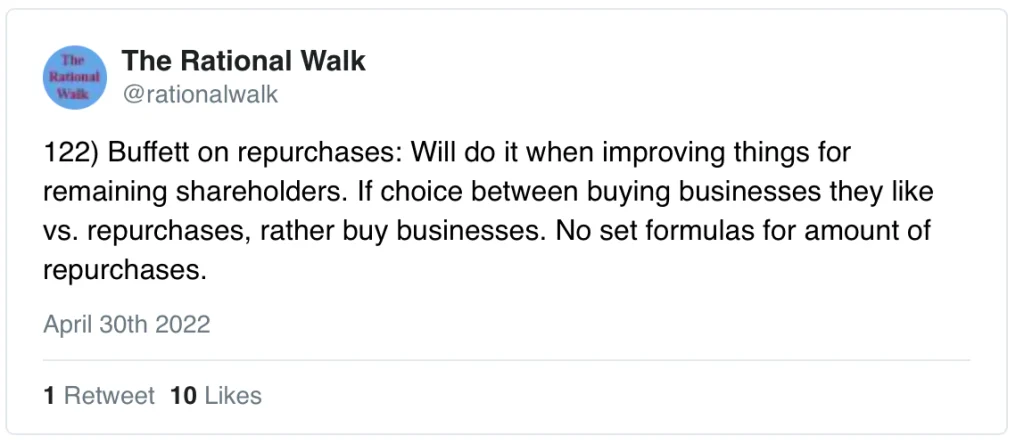

In Mr. Buffett’s opening remarks prior to the Q&A session, he indicated that he had stopped repurchase activity during the month of April. Toward the end of the Q&A session, he made a few more comments regarding repurchase activity:

This is a reiteration of what he has said many times in the past, so it should come as no surprise. Prior to July 2018, Berkshire’s repurchase policy was linked to a fixed price-to-book level multiple or 1.2x. That policy was altered to allow for repurchases at any price-to-book level as long as Mr. Buffett and Mr. Munger agree that the shares are trading below a conservatively calculated estimate of intrinsic value.

Only $6.4 billion worth of shares were repurchased from July 2018 until the end of 2019, but then the repurchase program accelerated dramatically. During 2020 and 2021 a total of $51.7 billion was used to repurchase stock. As Mr. Buffett noted in his recent annual letter, these repurchases left continuing shareholders owning approximately 10% more of all Berkshire businesses compared to what they owned on December 31, 2019.

During the first quarter of 2022, Berkshire used $3.1 billion to repurchase shares, a notable deceleration from the pace of 2020 and 2021. And then repurchases halted entirely during April.

The exhibit below shows Berkshire’s complete repurchase history. To download an Excel spreadsheet containing this data, please click the following link (please do not share this link with others — it is for subscribers only):

Download Berkshire Hathaway Repurchase History Spreadsheet

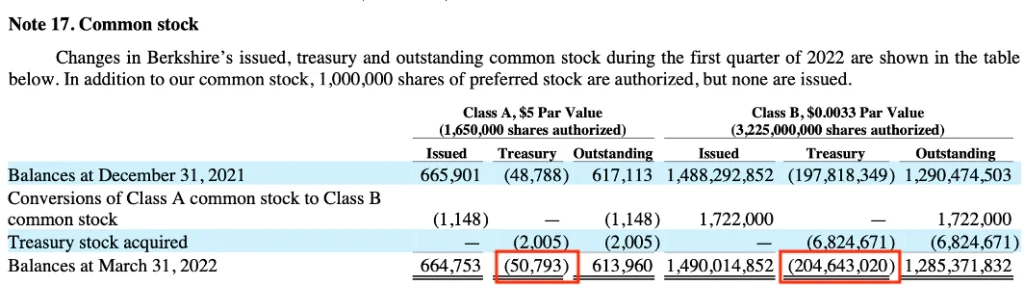

The total number of Class A and Class B shares in the spreadsheet ties back to the treasury share counts fond in Note 17 of the latest 10-Q report:

What can we infer from the cessation of repurchase activity in April?

It appears to me that Mr. Buffett is less likely to repurchase stock when the price-to-book ratio approaches and exceeds 1.5x. During April, Berkshire’s stock price rallied significantly spending most of the month around 1.5x March 31 book value before falling during the final few days of the month.

In addition to Berkshire’s rising price during April, Mr. Buffett has been finding other places to invest Berkshire’s cash and that probably also came into play. Is he repurchasing shares today? As I type this sentence around 2:30 pm eastern time, Berkshire’s A shares are trading around $474,000 which is 1.37x March 31 book value. I can say that Mr. Buffett is more likely to be buying today than he was last week, but no one knows for sure.

For shareholders hoping for more repurchases, the best thing that can happen is for Berkshire shares to trader lower. The lower the price, the better the value for repurchases and the more likely Mr. Buffett is to repurchase stock.

Copyright, Disclosures, and Privacy Information

Nothing in this newsletter constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.

Your privacy is taken very seriously. No email addresses or any other subscriber information is ever sold or provided to third parties. If you choose to unsubscribe at any time, you will no longer receive any further communications of any kind.

The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

Individuals associated with The Rational Walk LLC own shares of Berkshire Hathaway.