Berkshire Hathaway released 2021 financial results today along with Warren Buffett’s annual letter to shareholders. As usual, the company released these materials on a Saturday morning to give shareholders time to digest the results while the stock market is closed. I recommend reviewing financial results for any company you own before reading any media coverage so you can come to your own conclusions. In that spirit, here are the materials released this morning in case you would like to read them before reading my thoughts on the letter:

Press Release

Warren Buffett’s 2021 letter to shareholders

Berkshire Hathaway 2021 annual report

This year’s letter is very brief at just eleven pages but, as Mr. Buffett says, there’s well over a hundred pages of dense financial information in the annual report which some shareholders will find “engrossing”.

I’ve read the entire annual report and found perhaps half of it “engrossing”. But unfortunately, even after more than two decades of owning Berkshire shares, I am not at the point where I can read about subjects such as the Bornhuetter-Ferguson actuarial claims estimation model without my eyes glazing over, despite my coffee machine being extremely overworked throughout the day.

I will restrict my comments in this post to a list of interesting highlights from the letter. The highlights will be followed by a look at Berkshire’s repurchase history updated through 2021. However, I am not providing a comprehensive review of Berkshire’s 2021 results in this post.1

Annual Letter Highlights

Infrastructure Assets. Although Berkshire is perceived as a collection of financial assets, the company also owns and operates more infrastructure assets in the United States (carried at $158 billion on the balance sheet) than any other American corporation. Achieving this status was not an explicit goal but Berkshire will continue investing in infrastructure assets over the long haul. With recent capital expenditures at Berkshire Hathaway Energy far exceeding depreciation, this prediction seems likely to come true in the years ahead.

Taxes. Perhaps Mr. Buffett felt a need to highlight Berkshire’s status as a major U.S. taxpayer given recent populist rhetoric among politicians. While noting that Berkshire’s presence in the United States is an enormous advantage, he also points out that Berkshire paid $3.3 billion in federal income taxes in 2021 compared to total corporate income tax receipts of $402 billion. I would note that shareholders can easily calculate their own “look-through” taxes made on their behalf by Berkshire. As Mr. Buffett says, shareholders can credibly assert that “I gave at the office.”

The Four Giants. From time to time, shareholders question whether Berkshire might sell part of its enormous stake in Apple. Anything is possible, but Mr. Buffett clearly regards Berkshire’s 5.55% stake in Apple as a quasi-permanent holding. Apple is included in his discussion of the “four giants” along with Insurance, Burlington Northern Santa Fe, and Berkshire Hathaway Energy. Tim Cook is described as “brilliant” and Mr. Buffett provides a ringing endorsement of Apple’s repurchase program, presumably even at current prices.

Berkshire Hathaway Energy. In recent years, the “Environmental, Social, and Governance” (ESG) movement has gained momentum and Berkshire has been under pressure to focus more on climate issues. Mr. Buffett’s letter highlights Berkshire Hathaway Energy’s important societal role in reducing carbon emissions. He points out that the BHE website shows that “the company has long been making climate-conscious moves that soak up all of its earnings.” The annual report also includes a letter written by Greg Abel which focuses on BHE’s commitment to carbon emission reductions over the next three decades.2

Combs and Weschler Manage $34 Billion. The traditional table showing Berkshire’s top fifteen equity investment appears in the letter along with a statement that Todd Combs and Ted Weschler currently manage a combined $34 billion. The February 15 issue of Rational Reflections included some information regarding Berkshire’s latest 13-F report.

Mountains of Cash. Berkshire had $144 billion of cash and treasury bills on the balance sheet at the end of 2021 (excluding cash in the railroad and utility businesses). Berkshire has pledged to always maintain a minimum of $30 billion of cash on the balance sheet. Mr. Buffett attributes the large cash position to his failure to find attractive opportunities to acquire businesses or purchase stocks at attractive prices. He adds that this state of affairs is not pleasant but also will not be permanent.

Repurchases are characterized as a “mildly attractive” use of excess cash. At the right price, repurchases can add value, but buying back shares at excessive prices can also destroy value. “When the price/value equation is right, this path is the easiest and most certain way for us to increase your wealth.” Over the past two years, Berkshire repurchased 9% of shares outstanding at yearend 2019 for a total cost of $51.7 billion. Between January 1 and February 23, 2022, Berkshire repurchased an additional $1.2 billion. Mr. Buffett notes that Berkshire’s high quality shareholder base makes repurchases more difficult, but he still prefers to have a predominantly buy-and-hold shareholder constituency.

Paul Andrews, the founder and CEO of TTI, passed away last year. Mr. Buffett writes a lengthy account of Mr. Andrews, the history of his business, and why he decided to sell the business to Berkshire in 2006. I am always amazed to read these stories of how Berkshire’s reputation has made it almost the only choice for founders who wish to sell but care about what will happen to their business in the long run. Since Berkshire’s purchase of TTI, the number of employees has increased from 2,387 to 8,043 and earnings have increased by 673%.

Serendipity. In 2009, Mr. Buffett scheduled a board meeting in Fort Worth so directors could meet Mr. Andrews and learn more about TTI’s activities. During the same trip, Mr. Buffett met with Matt Rose, CEO of BNSF, on a day that happened to coincide with a poor earnings report which caused a decline in BNSF’s stock price. This meeting ended up being the impetus for Berkshire’s acquisition of BNSF. “The BNSF acquisition would never have happened if Paul Andrews hadn’t sized up Berkshire as the right home for TTI.”

How to clarify your thoughts. “Teaching, like writing, has helped me develop and clarify my own thoughts. Charlie calls this phenomenon the orangutan effect: If you sit down with an orangutan and carefully explain to it one of your cherished ideas, you may leave behind a puzzled primate, but will yourself exit thinking more clearly.” 3

Annual Meeting. The annual letter contains information regarding the in-person annual meeting scheduled for Saturday, April 30. There is also a separate page on Berkshire’s website providing the details. It looks like Berkshire will require proof of COVID vaccination to attend the meeting in-person. However, the meeting will also be webcast by Yahoo! Finance.

Repurchases

Warren Buffett has not found large acquisitions over the past few years, but he has allocated tens of billions of dollars to repurchase Berkshire Hathaway stock. He regards this use of capital as a “mildly” attractive way to enrich shareholders and notes that he will not make repurchases at any price. This is in stark contrast to the repurchase policies of most large corporations that seem to be price insensitive when it comes to repurchases.

The message is clear: Shareholders should expect to see repurchases from Berkshire when prices are attractive, but those repurchases could slow down or even stop entirely as the stock price rises. Mr. Buffett notes that $1.2 billion has been used for repurchases from January 1 to February 23, 2022. This pace is somewhat slower than in recent quarters, and that’s likely due to the price of Berkshire stock rising.

I maintain a spreadsheet listing Berkshire’s repurchase activity since the first repurchase program was announced in September 2011. I have updated this spreadsheet through the end of 2021, and it appears below:

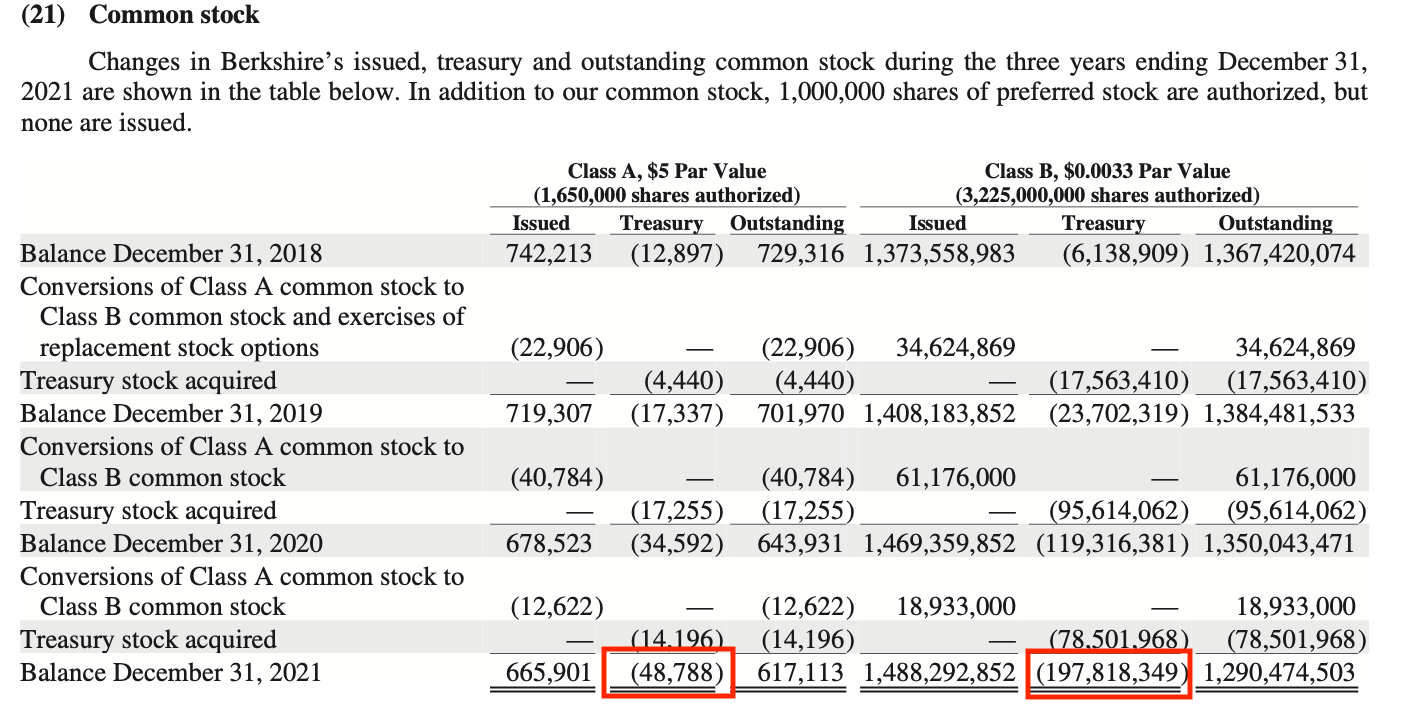

This spreadsheet lists the number of repurchased Class A and Class B shares that have been reported in Berkshire’s financial statements over the years. A total of 48,788 Class A shares and 197,818,349 Class B shares have been repurchased since September 26, 2011.4 In total, the cost of these shares was $59.795 billion, of which $51.7 billion is accounted for by repurchases since the beginning of 2020.

To reconcile my spreadsheet with Berkshire’s financial statements, refer to Note 21 of the 2021 annual report on form 10-K which shows that 48,788 Class A shares and 197,818,349 Class B shares are accounted for as treasury stock. Berkshire’s balance sheet confirms the Treasury Stock account is $59.795 billion at cost.

The first page of the 2021 10-K indicates that there were 615,333 Class A shares and 1,291,212,661 Class B shares outstanding as of February 14, 2022. With each Class B share having 1/1500 of the economic rights of a Class A share, this works out to 1,476,141 Class A equivalents outstanding as of February 14, 2022, compared to 1,477,429 Class A equivalents outstanding as of December 31, 2021.

From Mr. Buffett’s statement in the letter that $1.2 billion of stock has been repurchased between January 1 and February 23, it appears that he ramped up repurchase activity between February 14 and February 23. Of course, all of the details regarding this quarter’s repurchase activity will be released in the first quarter 10-Q which normally coincides with the annual meeting.

Disclosure: Individuals associated with The Rational Walk LLC own shares of Berkshire Hathaway.

- The last time I attempted to provide a comprehensive review of Berkshire was in March 2020 after the initial pandemic crash. I wrote it more for my own sanity than for the benefit of readers as an attempt to see how exposed Berkshire’s underlying businesses would be to the unprecedented economic conditions at the time. Although the post is a couple of years old, readers may find it interesting for the background information. [↩]

- At the 2021 annual meeting, Charlie Munger, perhaps inadvertently, spoke about Greg Abel as Mr. Buffett’s successor. Page K-24 of the 2021 annual report has made Mr. Abel’s status explicit: “Should a replacement for Mr. Buffett be needed currently, Berkshire’s Board of Directors has agreed that Mr. Abel should replace Mr. Buffett.” [↩]

- Mr. Buffett’s comments on writing and teaching are spot-on. For example, I will admit that I wrote this post more for my own benefit than for yours. Writing absolutely helps the writer clarify his thoughts, and I have no doubt absorbed more from today’s letter and annual report because I wrote about it. Clicking on the “publish” button that will send my thoughts to thousands of inboxes focuses my mind. [↩]

- Note the following for the 6/30/14 repurchase from the 2014 10-K: “On June 30, 2014, we exchanged approximately 1.62 million shares of GHC common stock for WPLG, whose assets included 2,107 shares of Berkshire Hathaway Class A Common Stock and 1,278 shares of Class B Common Stock. The Berkshire shares are reflected as treasury stock in our Consolidated Financial Statements.” [↩]