“With the price advantage GEICO’s low costs allow, it’s not surprising that several years ago the company seized the number two spot in auto insurance from Allstate. GEICO is also gaining ground on State Farm, though it is still far ahead of us in volume. On August 30, 2030 – my 100th birthday – I plan to announce that GEICO has taken over the top spot. Mark your calendar.”

— Warren Buffett, 2015 Letter to Berkshire Hathaway Shareholders

Progressive and GEICO gain market share at State Farm’s expense

It is safe to say that no one enjoys purchasing auto insurance. Annual premiums vary widely based on characteristics of the driver, the vehicle, and location, but the expense represents a significant budget line item for most people, with one study estimating the average annual cost at $1,655 in 2021. Rapid inflation in the cost of used automobiles, which increases claim costs, coupled with higher frequency of claims as people begin to return to offices will push annual premiums even higher in 2022.

Although inertia can keep customers with an insurance agent for many years, people are rarely sentimental or brand loyal when it comes to auto insurance. They tend to shop based on premium cost. GEICO and Progressive have both been regular advertisers on television for decades, with recognizable brand equity represented by Progressive’s Flo character and GEICO’s gecko. The message is that you can save money on auto insurance by purchasing it directly online.

Both GEICO and Progressive have made significant market share gains in recent years and it appears that State Farm could very well lose its top position in the private passenger auto insurance market several years before Warren Buffett’s goal of 2030. It would not surprise me to see State Farm displaced by 2025. However, it is an open question whether GEICO or Progressive will take the top spot.

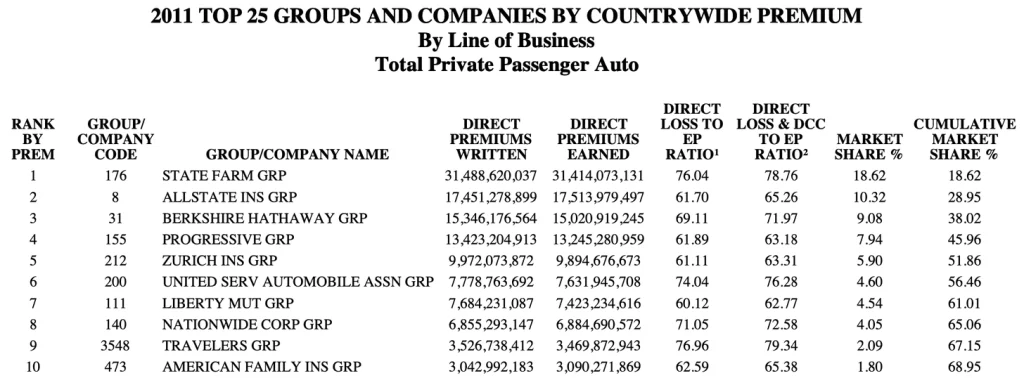

Let’s start by taking a look at the market share statistics published by the National Association of Insurance Commissioners (NAIC). Rewinding back to 2011, here is what the private passenger auto market looked like for the top ten players:

A decade ago, State Farm was clearly the dominant player in the private passenger auto insurance market with market share of 18.6%, far surpassing Allstate’s 10.3% share. Berkshire Hathaway’s GEICO subsidiary had less than half of State Farm’s volume at the time. We can also see that the industry was quite concentrated with cumulative market share of the top ten competitors at nearly 69%.

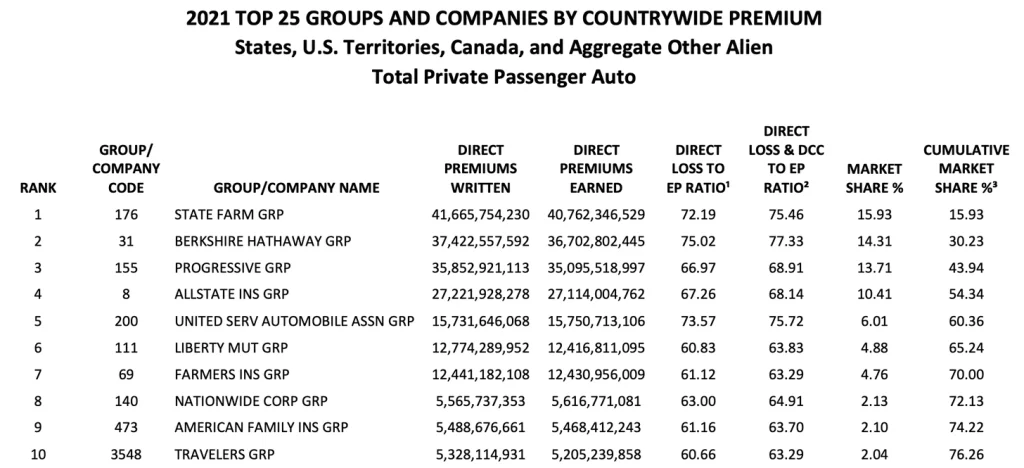

Let’s fast forward a decade to 2021 and see how the situation has changed:

For overall context, direct premiums earned for the entire industry increased from $167.8 billion in 2011 to $258.4 billion in 2021, a 54% increase over a decade. Over the same timeframe, State Farm’s earned premiums increased by 29.8%, trailing the growth of the overall industry. On the other hand, earned premiums at GEICO and Progressive increased by 144% and 165%, respectively. Industry consolidation increased with the market share of the top ten companies at 76.3%.

Taking an even longer view, the following exhibit shows key data for GEICO and Progressive over the past twenty-one years:

The growth of both companies has been phenomenal, and this growth has been profitable with Progressive posting underwriting profits in every year and GEICO posting underwriting profits in all years except for 2017.

We can see from the table above that earned premiums, presented in annual reports on a GAAP basis, differ somewhat from the NAIC data which I believe is based on statutory accounting. For GEICO, the difference is not large, but in Progressive’s case, earned premiums include a commercial auto insurance business as well as a non-auto property business since 2015. We can see that when we look at total personal lines, the figures are pretty close to the NAIC data for private passenger auto. The GAAP financials appear to validate the market share data presented by NAIC.

It is difficult to forecast whether Progressive or GEICO stand a better chance of surpassing State Farm, but there are a few interesting points worth considering:

- GEICO consistently runs at a lower expense ratio compared to Progressive. In 2021, GEICO’s expense ratio was 14.5% vs. Progressive’s 19.6%.

- Progressive consistently runs at lower loss ratio compared to GEICO. In 2021, GEICO’s loss ratio was 82.2% vs. Progressive’s 75.8%.

- GEICO is more likely to accept a higher combined ratio, possibly indicating a more aggressive posture with respect to expansion. Over the past decade, GEICO’s combined ratio has averaged 95.7% vs. 92.7% for Progressive.

- In aggregate, GEICO has recorded underwriting profits of $12.2 billion over the past decade while Progressive has recorded underwriting profits of $20.6 billion.

One interesting twist is that Progressive has a goal of writing business at a 96% combined ratio, so the company’s results have surpassed management’s expectations, which could mean that expansion efforts have not been aggressive enough.

Berkshire Hathaway’s frugal culture is alive and well at GEICO. They run a very tight ship with respect to expenses, although Warren Buffett has always said that he’s happy to spend a great deal on advertising. The issue is that GEICO needs to be ultra-efficient when it comes to expenses given that their loss ratio seems to run high.

I’m not the first analyst to notice the performance difference between GEICO and Progressive. At the 2021 Berkshire Hathaway annual meeting, Warren Buffett was asked about Progressive and replied at length:

“Progressive has had the best operation in recent years, in terms of matching rate to risk, and I mean, that’s what insurance is all about among other things. But I mean, you have to have the right rate. If you think that 90 year olds and 20 year olds have an equal chance of dying, I mean, you’re going to be out of business very quickly, the life insurance business. And you will get all the 90-year-old risks and the other guy will get the 20-year-old risks.

And the same thing applies in auto insurance. I mean, there’s a huge difference between 16-year-old males, and how they drive, and 40-year-old, married, employed people. So companies that do the best job of actually having the appropriate rate for everyone of their policy holders, is going to do very well, and Progressive has done a very good job on that.

And we’re doing a much better job on that already, but Todd Combs has gone there. And it’s a very interesting business, both Progressive and GEICO were started in the ’30s. I believe I’m right about Progressive on that, and we were started in ’36. We have had the better product for a long, long time, I mean, in terms of cost. And here we are 80, 85 years later, in our case, and we have about 13% or so of the market, whatever it may be, and Progressive as just a slight bit less. So the two of us have 25% of the market, roughly, in this huge market, after 80 something years of having a better product. So it’s a very slow changing, competitive situation, but Progressive has done a very, very good job recently. We’ve done a very, very good job over the years, and we’re doing a good job now, but we have made some very significant improvements.”

Ajit Jain, Berkshire’s Vice Chairman in charge of insurance operations, had some comments as well:

“There’s no question, Progressive is a machine. They’re very good at what they do, whether it’s underwriting, which Warren talked about, in terms of matching rate to risk, whether it’s handling claims. Having said that, I think GEICO is catching up with Progressive. More than a year ago, about a year ago, Progressive had margins that were almost twice as much as GEICOs, and growth rates that were almost twice as much as GEICOs. If you look at the results, as of now, Progressive is still crushing it, in terms of growth, relative to GEICO, but GEICO has certainly caught up with Progressive in terms of margins, and, hopefully, that gap will be non-existent in the future.

The second point I want to make on the issue of matching rate to risk, GEICO had clearly missed the business, and were late in terms of appreciating the value of telematics. They have woken up to the fact that telematics plays a big role in matching rate to risk. They have a number of initiatives, and, hopefully, they will see the light of day before, not too long, and that’ll allow them to catch up with their competitors, in terms of the issue of matching rate to risk.”

It appears that GEICO has a lot of work to do to catch up with Progressive in a number of areas, but the low cost structure embedded in the company’s culture represents a durable advantage.

In December 2019, Todd Combs was named Chief Executive Officer of GEICO in a move that surprised many Berkshire shareholders. Todd Combs has been managing a significant chunk of Berkshire’s investment portfolio since joining the company in 2010. He has continued to manage his portfolio while also serving as CEO of GEICO for over two years. GEICO’s website seems to imply that Mr. Combs will continue in both roles indefinitely.

In December 2021, GEICO’s Executive Chairman Tony Nicely retired. Mr. Nicely started at GEICO in 1961 and served as Chairman and CEO for 25 years prior to assuming the Executive Chairman role in 2018. Mr. Buffett has praised Mr. Nicely’s management and leadership skills on numerous occasions, crediting him for engineering GEICO’s exceptional growth over the past few decades.

Although Mr. Combs is no doubt a capable executive, he seems to have a lot on his plate running a complex company like GEICO in the midst of a competitive battle with Progressive while also running a multi-billion dollar investment portfolio. It will be interesting to see if Mr. Combs will end up focusing entirely on GEICO in the future. There is no obvious successor for Ajit Jain, who is 70 years old. Perhaps Mr. Combs, at age 51, could be an eventual successor.

As a Berkshire shareholder, I have followed Progressive closely for years. GEICO provides relatively little information in Berkshire’s annual reports and by following Progressive, one can stay abreast of trends in the auto insurance market that are likely impacting GEICO as well. Progressive has extensive and transparent reporting and posts summary results on a monthly basis. I also like their report on loss reserving practices which has a great introduction to reserving along with a useful glossary.

It is interesting to examine Progressive’s valuation in the stock market since GEICO is a very comparable company. I have done this as well over the years, although I won’t go into valuation questions in this post to keep it at a reasonable length. However, it is worth briefly noting that Progressive, at a market capitalization of nearly $68 billion, currently trades at a price-to-book multiple of approximately 3.8, which represents a level rarely seen over the past two decades.

If GEICO was a publicly traded company, it would probably be richly valued as well in today’s market. A decade ago, I wrote an article that examined some comments Mr. Buffett made regarding what he paid for GEICO in 1996 to guess what he would think of Progressive’s valuation. That approach could be used to look at the situation today … perhaps the subject of a future article.

Copyright, Disclosures, and Privacy Information

Nothing in this newsletter constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.

Your privacy is taken very seriously. No email addresses or any other subscriber information is ever sold or provided to third parties. If you choose to unsubscribe at any time, you will no longer receive any further communications of any kind.

The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

Individuals associated with The Rational Walk LLC own shares of Berkshire Hathaway.