“Our new Constitution is now established, everything seems to promise it will be durable; but, in this world, nothing is certain except death and taxes.”

If we could ask Benjamin Franklin about life in modern-day America, he would most likely say that death, taxes, and inflation are all certain and inevitable realities.

Inflation was hardly unknown to Franklin and his contemporaries, but he would not have considered a perennially rising price level to be inevitable during peacetime, much less a desirable goal for politicians and bureaucrats to purposely engineer decade after decade, in perpetuity.

Today, we are far removed from Ben Franklin’s world. We have a Federal Reserve that has pledged to generate annual inflation of 2% despite having no statutory authority to do so. To the extent Congress has expressed its will on inflation, it is that America should have stable prices over time, not a steady erosion of purchasing power.1

Two percent annual inflation seems like a small figure until you realize that it implies destruction of half of the purchasing power of the dollar over thirty-five years. It is even worse because the Federal Reserve will never seek to offset a period of high inflation, as we are presently experiencing, with inflation below the 2% target for a period of time. Quite the contrary. There are many powerful people openly advocating for a higher inflation target and they are even saying the quiet part out loud:

“A bit of inflation also acts as a labor-market lubricant. Over time, higher inflation tends to translate, one for one, into higher wages. In bad times, though, inflation allows an employer to cut labor expenses by freezing pay so inflation gradually reduces real wages. That isn’t possible with zero inflation: The employer would have to cut jobs or pay, which is demoralizing and deeply unpopular.”

As I wrote in September 2021, one purpose of the 2% target is to generate what is known as money illusion. While sophisticated investors will observe low inflation and still account for it, ordinary Americans are busy living their lives and might be fooled into accepting cuts in real wages if inflation is low enough to not be immediately noticed. To say that this is a dishonorable way to conduct national affairs is an understatement particularly because inflation has a severe impact on poor people.

Included among the voices supporting a higher inflation target, at least in theory, is former Federal Reserve Chairman Ben Bernanke. When Bernanke codified a 2% inflation target as official policy in 2012, he did so without authority from Congress. Remarkably, Bernanke admitted as much this in a recent appearance where he agreed “in theory” that the inflation target should be increased to a level higher than 2%:

“Well, I agree in theory. But I think the actual reality doesn’t really support it. One thing nobody talks about is politics. The Congress let us put in an inflation target without being part of the process and I had to consult widely with that. I remember we were here and Janet Yellen put up a video of the head of the House Financial Services Committee saying, ‘under no circumstances will you raise the inflation target.’ I think if you did it you would have to consult with Congress, and you might find out at the end that your inflation target is one (percent). [laugher among panelists and audience members]

The quote above starts at approximately 3:08:17:

There is a difference between Congress silently acquiescing to the Fed implementing an inflation target and authorizing such a target. Bernanke admits that if the Fed had to approach Congress to seek formal authority to increase the target, politicians might very well demand a lower target. Of course, that would be the prerogative of elected representatives of the American people. The Federal Reserve was created by the United States Congress in 1913 and is, at least theoretically, subject to its oversight. The fact that a former Chairman of the Fed views Congress as an annoyance to be overcome is an example of the institutional epistemic arrogance of our central bank.

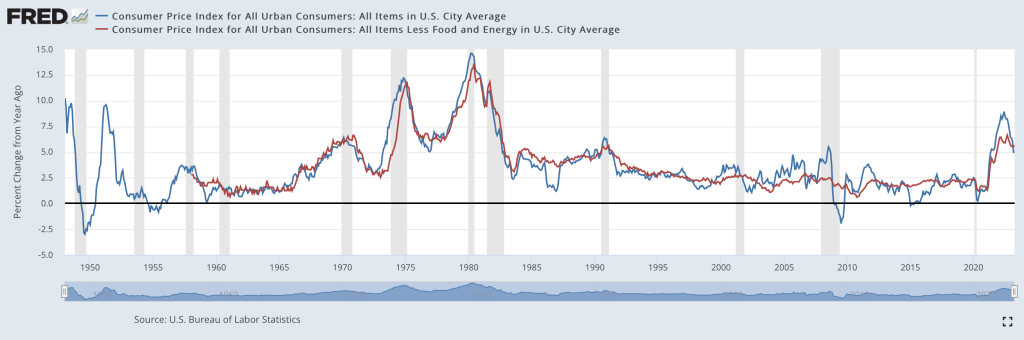

I could take up much more space on the Federal Reserve, but regardless of what you think about Fed policy, it is an established fact that inflation has been a nearly constant reality since the Second World War. For all the ink spilled by economists over the risk of “deflation”, there have been hardly any flirtations with this dreaded condition in postwar history. The bias has been toward inflation, and lots of it:

If the chart above doesn’t bring home the point strongly enough, consider that the price level has increased by an order of magnitude over the past sixty years, as measured by the consumer price index:

Of course, this represents more than 2% annual inflation. But would it surprise you to know that average annualized inflation over this sixty year period was “only” 3.9%?

Another way to look at this situation is to realize that if we define a “millionaire” today as someone who has at least $1 million of net worth, that is the same as someone who had a $100,000 net worth in 1963. Conversely, what a person in the early 1960s thought of as a millionaire is someone who is worth at least $10 million today.

Low single digit annual inflation, if sustained over a long enough period of time, is absolutely ruinous when it comes to the purchasing power of the dollar. Even if the Federal Reserve hits its 2% inflation target, a million dollars in today’s money will lose nearly 70% of its purchasing power over the next sixty years.

To make matters worse, the CPI is constantly being adjusted by the Bureau of Labor Statistics in ways that many observers believe understates the actual change in the cost of living. However, even if you believe that the adjustments made by the BLS are justified, it is impossible to deny the fact that inflation is a major tax on the American people. When inflation is high, this condition is noticed like metastatic cancer. When inflation is low enough, it is more like a silent tapeworm that policymakers hope will fool people into thinking that they are better off than they really are.

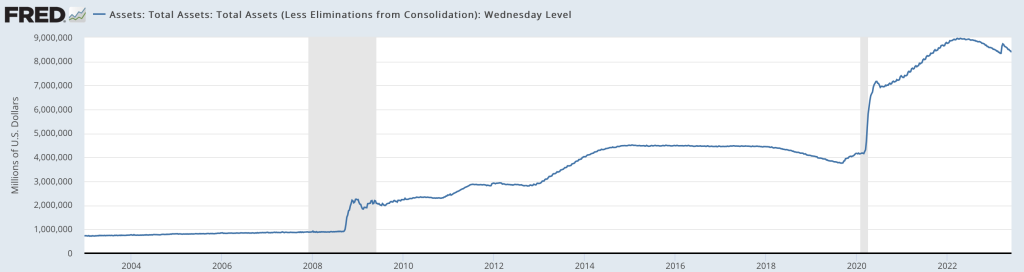

Although the recent debt ceiling drama is now in the rear view mirror, the fiscal situation remains terrible with rising debt as far as the eyes can see. Since the financial crisis, the Fed has been acquiring trillions of dollars of the debt through quantitative easing. These purchases of treasury securities amount to monetizing the national debt based on the Fed’s own definition, as documented in a 2013 article by economists at the St. Louis Fed:

“If the recent rapid accumulation of Treasury debt on the Fed’s balance sheet constitutes a permanent acquisition, then the corresponding supply of new money would be expected to remain in the economy (as either cash in circulation or bank reserves) permanently as well. As the interest earned on securities held by the Fed is remitted to the Treasury, the government essentially can borrow and spend this money for free. If, on the other hand, the recent increase in Fed Treasury debt holdings is only temporary (an unusually large acquisition in response to an unusually large recession), then the public must expect that the monetary base at some point will return to a more normal level (through sales of securities or by letting the securities mature without replacing them).”

Whatever “quantitative tightening” the Fed has done has barely put a dent in returning its balance sheet to levels prior to the start of QE. Is there any reason to believe that the Fed will not continue to monetize the oceans of debt that the Treasury will issue over the next several decades?

Can the systemic bias toward inflation in the United States be tamed by the Federal Reserve or Congress? I have no crystal ball, but I am highly skeptical that inflation will be lower over the next sixty years than it has been over the past sixty. In other words, inflation could very easily end up being twice the Fed’s current inflation target.

For investors, the prospect of continued high inflation is very challenging. A business that has proven pricing power and a demonstrable moat could be in a position to survive periods of inflation in good shape. In contrast, owners of most fixed income securities will face the prospect of diminished purchasing power if actual inflation is higher than inflation expectations. The exception is that owners of inflation protected fixed income securities could retain more of their purchasing power provided that the CPI is reasonably close to estimating the change in the cost of living.

In the second part of this two-part series, I will discuss the market for Treasury Inflation Protected Securities (TIPS) and I Series U.S. Savings Bonds, both of which provide conservative investors with some inflation protection, albeit imperfect. I have written about these securities in the past in different contexts but I have not compared them side-by-side which will be the goal of the next article.

Copyright, Disclosures, and Privacy Information

Nothing in this article constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC. The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

- The text of the 1978 Humphrey-Hawkins Act includes the following text indicating a goal of achieving zero percent inflation (stable prices) by 1988, provided that this could be done consistent with the reduction of unemployment: “Upon achievement of the 3 per centum goal specified in subsection (b) (2), each succeeding Economic Report shall have the goal of achieving by 1988 a rate of inflation of zero per centum: Provided, That policies and programs for reducing the rate of inflation shall be designed so as not to impede achievement of the goals and timetables specified in clause (1) of this subsection for the reduction of unemployment.” [Emphasis added] [↩]