“You know, if baseball umpires were on the front page of the sports section every week, you’d know something was desperately wrong with the game.”

— Jim Grant referring to central bankers

Scandals that dominate headlines typically involve obvious ethical or legal lapses that casual observers can easily understand. So it should come as no surprise that Robert Kaplan’s trading activities in 2020 generated significant outrage. As President of the Dallas Federal Reserve Bank, Mr. Kaplan was an active trader of individual stocks, as The Wall Street Journal reported on September 7:

According to the disclosure form provided by the Dallas Fed, Mr. Kaplan had a total of 27 individual stock, fund or alternative asset holdings each valued at over $1 million. Mr. Kaplan’s stock holdings included Apple Inc., Amazon.com Inc., Boeing Co., Alphabet Inc., Facebook Inc. and Marathon Petroleum Corp.

The form also shows Mr. Kaplan made some combination of sales or purchases of over $1 million in 22 individual company shares or investment funds. These transactions included Apple, Alibaba Group Holding Ltd., Amazon, General Electric Co. and Chevron Corp.

Eric Rosengren, President of the Boston Federal Reserve Bank, also traded stocks actively in 2020. In the wake of blowback from these reports, both men announced that they would sell individual stocks in their portfolios and cease active trading, although they defended the propriety of their actions in 2020.

In recent decades, the Federal Reserve has, as an institution, become much more communicative regarding policy decisions and individual Fed officials are now fixtures on financial television and in the pages of newspapers, both as named sources and as “unnamed officials”. Their utterances can and do move markets, and obviously Federal Reserve decisions on monetary policy have a substantial impact on the valuation of all financial assets given that interest rates act as “financial gravity”.

It doesn’t take an expert in ethics (or economics) to understand the ethical issues associated with Fed officials trading actively in the stock market while also speaking publicly on monetary policy.

While my reaction to these disclosures was predictably one of disgust, I was not at all surprised, nor do I think that this episode compares to much larger problems at the Federal Reserve. In fact, trading by Fed officials, even multi-million dollar trades, pale in comparison to policy issues that are blandly reported in the mainstream media but reveal major ethical issues.

On September 1, The Wall Street Journal published an article entitled How to Deal With Above-Target Inflation: Raise the Target which raised my blood pressure far more than revelations of Mr. Kaplan’s multi-million dollar trading.

The Federal Reserve operates under a dual mandate of maintaining price stability while supporting maximum sustained employment. This mandate was codified as law in the Humphrey–Hawkins Full Employment Act of 1978, a time of significant inflation.

Price stability, to an ordinary person one would meet at a barber shop or the grocery store, is likely to be interpreted as … stable prices, meaning that the purchasing power of the dollar would be roughly the same over long periods of time for a representative basket of goods purchased by ordinary consumers. However, in 2012, Federal Reserve Chairman Ben Bernanke codified a 2% inflation objective as official Fed policy and declared that 2% inflation was consistent with price stability.

It should be emphasized that the Federal Reserve itself is an institution created by the Congress of the United States, not a fourth branch of government created by the Constitution. While it is supposed to be “independent”, the Fed is ultimately accountable to the enabling legislation that created it and governs its conduct.

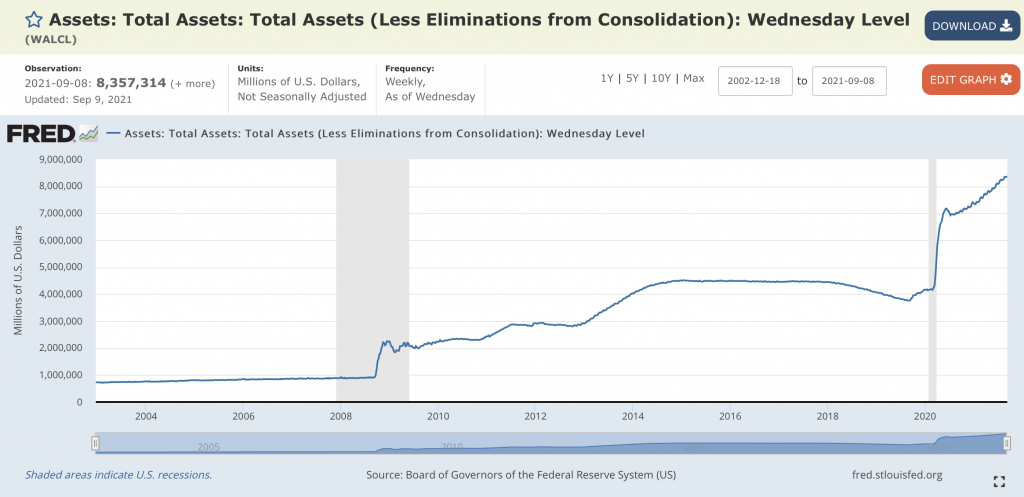

With inflation running significantly higher than 2% over the past year, as the country bounces back from the COVID recession, the Fed has continued expansive monetary policies with the Federal Funds rate anchored near zero and monthly purchases of $120 billion of Treasuries and mortgage backed securities.

It should be noted that unless the Federal Reserve eventually reverses these purchases and returns its balance sheet to its former levels, purchasing Treasury securities amounts to monetizing the national debt based on the Fed’s own definition, as documented in a 2013 article referring to a prior episode of asset purchases:

If the recent rapid accumulation of Treasury debt on the Fed’s balance sheet constitutes a permanent acquisition, then the corresponding supply of new money would be expected to remain in the economy (as either cash in circulation or bank reserves) permanently as well. As the interest earned on securities held by the Fed is remitted to the Treasury, the government essentially can borrow and spend this money for free. If, on the other hand, the recent increase in Fed Treasury debt holdings is only temporary (an unusually large acquisition in response to an unusually large recession), then the public must expect that the monetary base at some point will return to a more normal level (through sales of securities or by letting the securities mature without replacing them).

Talk of “tapering” asset purchases has typically led to selloffs in the stock market and the erroneous impression that tapering involves shrinking the Fed’s balance sheet. In fact, tapering the $120 billion of monthly purchases only means that the Fed’s rate of monetization is decreasing.

There is absolutely no talk of the Fed selling the assets it has acquired during the pandemic (not to mention prior episodes of asset purchases in the early ‘10s). Monetization of the debt has become an accepted policy objective, one that is not authorized by the Fed’s mandate from Congress and therefore is not authorized by the consent of the citizens of the United States.

While monetizing the national debt is rightly viewed as a scandal, one that is orders of magnitude more serious than Mr. Kaplan’s frenetic trading habit, the even bigger scandal lies in the motivation of those who not only support the goal of 2% inflation but want to increase that objective. As reported in The Wall Street Journal article, an important motivation is to enable the stealthy erosion of real wages of American workers:

A bit of inflation also acts as a labor-market lubricant. Over time, higher inflation tends to translate, one for one, into higher wages. In bad times, though, inflation allows an employer to cut labor expenses by freezing pay so inflation gradually reduces real wages. That isn’t possible with zero inflation: The employer would have to cut jobs or pay, which is demoralizing and deeply unpopular.

Cutting through the economics jargon, what Fed officials are trying to do is to help American businesses cut the real wages of workers in a stealthy manner by freezing pay and having that pay slowly eroded by inflation that they hope will be low enough to not be perceived.

This is a textbook case of money illusion. If inflation is running at 3% per year and you get a raise of 2%, you are worse off than you were before, but human psychology is such that when you see the nominal amount of take-home pay go up, you might feel temporarily better off. In fact, you are no better off than if your employer cut your pay by 1% and prices remained stable with a 0% inflation rate. But, as the Federal Reserve and other government officials know well, it is far harder for an employer to pursue nominal wage cuts than it is for real wages to be cut via inflation.

There are important nuances to this equation that I will not go into here. In particular, there are serious questions regarding whether the consumer price index is an accurate measure of the cost of living for typical consumers. Also, every individual’s cost of living is somewhat unique. However, the general point certainly holds: if your nominal wages are not rising at least as fast as your cost of living, you are falling behind.

In a market economy, it is not the government’s job to ensure that workers enjoy real gains in wages, nor is it even the government’s job to prevent real declines in wages. The question here is not one of stability or the “right” of any individual worker to maintain his or her purchasing power. The issue is whether it is right for the Federal Reserve in particular or the government in general to set, as a policy goal, a rate of inflation that is seen as beneficial specifically because it offers the opportunity to erode real wages without seeming to do so.

Sometimes a big scandal can be obscured by revelation of a smaller scandal that is easier for most people to understand. Mr. Kaplan’s trading activity is easy to understand while the intricacies of money illusion are significantly more complex.

One scandal involves millions of dollars and the other involves trillions. Yet the easy-to-understand scandal is the one that was supposedly “fixed” by Mr. Kaplan’s planned divestment of individual stock holdings.

Meanwhile, the Fed’s radically easy monetary policy, driven by epistemic arrogance that they will not allow the situation to get out of control, continues apace with unknown risks to the economy and individual workers.

Copyright, Disclosures, and Privacy Information

Nothing in this newsletter constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.

Your privacy is taken very seriously. No email addresses or any other subscriber information is ever sold or provided to third parties. If you choose to unsubscribe at any time, you will no longer receive any further communications of any kind.

The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.