“Progressive has been on the telematics bandwagon for, I don’t know, more than 10 years, probably closer to 20 years. GEICO, until recently, wasn’t involved in telematics. And it’s been only the last two years that they’ve made a very serious effort, in terms of using telematics for segmentation and for trying to match rate and risk. It’s a long journey. But the journey has started, and the initial results are promising. It’ll take a while, but my hope and expectation is that hopefully in the next year or two, GEICO will be in a position to catch up with Progressive, in terms of telematics. And hopefully that’ll then translate into both growth rate and margins.”

— Ajit Jain, Berkshire Hathaway Annual Meeting, May 2, 2022

Automobile insurance is a major expense for the typical American family. Bankrate estimates that the average cost of a full coverage automobile policy is now $2,014 per year. As a point of reference, the Bureau of Labor Statistics recently reported that median weekly earnings of full-time wage and salaried workers was $1,100 during the first quarter, the equivalent of $57,200 on an annualized basis.

When I wrote Auto Insurance Competitive Dynamics in April 2022, Bankrate indicated that the average cost of a full coverage automobile policy was $1,655 during 2021. When the cost of a non-discretionary big ticket item increases by over 20% in a short period of time, the typical consumer is going to comparison shop. As much as someone might like Progressive’s Flo or the famous GEICO Gecko, there are limits to brand loyalty in this business. The internet makes comparison shopping easy.

GEICO and Progressive have long been fierce competitors and I have written about this rivalry many times over the years. As a Berkshire Hathaway shareholder, I have followed Progressive for well over a decade. I wrote a detailed profile of Progressive in December 2022 that is now free to read. It contains information about the auto insurance industry as well as a section on the rivalry between GEICO and Progressive.

In the 1990s, GEICO and Progressive were relatively small players in auto insurance with market shares of 2.5% and 2.2% respectively in 1995. By 2021, GEICO had taken the number two position behind State Farm with 14.3% of the market while Progressive was close behind at 13.7%. However, Progressive passed GEICO to take second place in 2022, as measured by direct premiums written. GEICO still had a slight edge in direct premiums earned. The following exhibit shows market share data for 2022 provided by the National Association of Insurance Commissioners:

For all practical purposes, Progressive and GEICO are nearly tied in the competition for second place, with State Farm maintaining a tenuous grasp on first place.

In the Progressive profile, I provided a snapshot of key data for Progressive and GEICO since 2001. The exhibit below updates that snapshot for 2022 results. Note that premiums earned in this table includes Progressive’s commercial and property lines in addition to private passenger auto lines.

GEICO has consistently run at a lower expense ratio compared to Progressive, and this was particularly pronounced in 2022 as GEICO reduced its expense ratio from 14.5% to 11.7%. Progressive reduced its expense ratio from 19.6% to 18.5%. However, GEICO’s loss ratio skyrocketed to 93.1% while Progressive kept its loss ratio to 77.3%. As a result, GEICO’s combined ratio was 104.8% while Progressive’s combined ratio was 95.8%. For the second time since 2001, GEICO posted an underwriting loss for a full year. In contrast, Progressive has no annual underwriting losses since 2001.

The pandemic resulted in unprecedented shifts in driver behavior that insurers had no way to model ahead of time. Initially, industry loss ratios were far lower than normal as the pandemic began in the first quarter of 2020. Fewer drivers were on the roads due to lockdowns and mileage driven plummeted. However, Progressive, GEICO, and other insurers provided rebates to customers in 2020 in recognition of lower automobile usage. These rebates inflated expense ratios in 2020.

As drivers returned to the roads in 2021 and 2022, accidents and claims predictably increased. Inflation began to take a toll on insurers as the cost of repairs increased and used car prices skyrocketed, as I discussed in an article on the automobile industry in August 2022. It has been a rough few years for all auto insurers.

Conventional wisdom seems to be that GEICO’s late implementation of telematics is to blame for many, if not most, of the company’s underperformance relative to Progressive. In my profile on Progressive, I include a number of quotes from Warren Buffett and Ajit Jain regarding telematics. They both concede that Progressive’s superior use of technology has provided an edge with respect to setting the right premium based on the risk of the driver.

I am writing this article on the eve of the 2023 Berkshire Hathaway annual meeting on May 6, 2023. Tomorrow morning, Berkshire will release first quarter 2023 results including the 10-Q which will contain details on how GEICO has fared so far this year. Unfortunately, most Berkshire shareholders will not have time to review this material prior to the annual meeting.

Progressive’s Q1 2023 Results

In addition to providing quarterly results, Progressive releases a significant amount of information on a monthly basis on its investor relations site. As a result, following Progressive’s results during the quarter is possible with an unusually high degree of granularity. Berkshire shareholders can look at Progressive’s results as a sort of leading indicator of how industry conditions are shaping up during a quarter.

The rest of this article is a brief overview of Progressive’s results for the first quarter with a focus on policies in force and underwriting results. I covered the company’s business model, investment portfolio and overall results in much more detail in the profile published in December so readers who are particularly interested in the company can refer to that report in addition to what follows in this article.

The Excel file that accompanies the profile contains a spreadsheet with monthly data on policies in force and underwriting results for 2019 through November 2022. The exhibit below shows trends in policies in force for March 2022 through March 2023:

Progressive has been very successful adding policies in force with a 8.9% gain in policies in force over the past year. In personal auto, policies in force increased by 10.8% with the direct channel posting a gain of 15.2% while the agency channel posted a 5.3% gain. We can see from the sequential change in policies in force that the company’s success in adding policies has accelerated over the past three months.

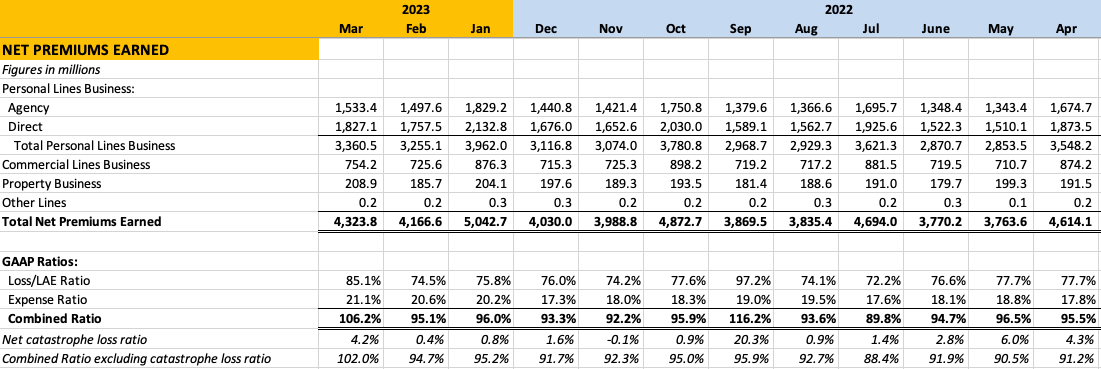

Unfortunately, underwriting results have been poorer than management expected during the first quarter. The following exhibit shows monthly underwriting results from March 2022 to March 2023:

For the first quarter as a whole, Progressive posted a loss ratio of 78.4% and an expense ratio of 20.6% for a combined ratio of 99%. Progressive recorded unfavorable reserve development of $621.2 million during the first quarter of 2023. Unfavorable development related to prior accident years (mostly attributable to 2022) inflated Progressive’s loss ratio for the quarter by 4.6%. CEO Tricia Griffith explained the situation as follows in her quarterly letter to shareholders:

“During the first quarter, we experienced continued elevated loss costs due, in part, to our inflationary environment, reserving development, additional weather-related losses, and recent law changes in Florida that impacted loss estimates and prompted increases to our reserves. Loss costs emerged higher than we anticipated and prior accident year reserves developed unfavorably 4.6 points on the companywide CR. The majority of the unfavorable development related to fixing cars (property damage, collision, and comprehensive coverages) as the cost to fix vehicles continued to increase.”

In light of these developments, Progressive is re-evaluating its rate plans and will be more aggressive with raising rates in the future. It seems apparent that Progressive was not aggressive enough with pricing during the first quarter. This resulted in strong growth in policies in force but at the cost of exceeding management’s targeted combined ratio of 96%.

Advertising spending in the first quarter of 2023 was 23% higher than in the first quarter of 2022, and this likely played a major role in attracting more customers to Progressive. During the first quarter earnings call, Ms. Griffith indicated that the company would curtail advertising expenses in order to lower the expense ratio:

“Our largest controllable variable expense is advertising spend, and we are taking action to reduce these costs, which we expect could both slow growth and help to reduce our expense ratio. Once we are confident that we can deliver our target calendar year profitability, we will consider resuming our spend. While we won’t provide details on which segments of media we are reducing or how this may affect growth going forward, I will tell you that we’ve invested in bringing the same industry-leading science from the pricing side of our business to the acquisition side, and we’ll continue to spend in the places that we believe have the greatest benefit to the business.”

Advertising costs can be viewed as an investment of sorts because there is a timing difference between advertising spending and revenue recognition. As Ms. Griffith points out in her letter, advertising costs are expensed as incurred while premiums are earned over the policy term, which is normally six months for personal auto policies.

The problem facing all auto insurers is that if you put the pedal to the metal on advertising spending but do not have rates set appropriately, you may attract customers who end up being unprofitable in the long run. This is where Progressive’s vaunted telematics program is supposed to shine. By targeting rates based on risk, informed by the company’s technology, Progressive should be in a position to attract business that will be profitable — that is, result in loss ratios that are acceptable.

Ms. Griffith appears to be proud of the growth in the first quarter and believes that aggressive rate actions should deliver Progressive’s targeted combined ratio of 96 for the full year:

“We plan to take aggressive rate increases where needed across all lines through the balance of 2023 to ensure we’re pricing to deliver our target profit margin. The next question, given the actions we will take to meet our profit target is, what will this do to growth?

First and foremost, keep in mind that growth in the first quarter of 2023 was an all-time high for the company, and we are very proud of that. Secondly, we are still in a very hard market with lots of consumers quoting their insurance.

We also continue to see ambient shopping. While policy growth may be slowed by our actions, we still anticipate there will continue to be robust demand for our products. Of course, the actions of our competitors also play a role in what growth will be. So I won’t speculate on specific growth predictions. However, you can rest assured that we are focused on growing policies that we believe will meet or exceed our target margins.”

When I read “our competitors”, I obviously think of GEICO. Berkshire’s results tomorrow will reveal how GEICO has fared so far in 2023, although we will not get the level of granularity that Progressive provides. Still, we should get an indication of how GEICO has performed in terms of growth and profitability during Q1. In addition, Ajit Jain and Warren Buffett are certain to get questions about GEICO’s position relative to Progressive during the Q&A session of the annual meeting.

Ms. Griffith concluded her prepared remarks during the call by commenting on Progressive’s reserve adequacy in light of $621.2 of adverse development during the first quarter. She noted that Progressive’s coverages are short-tail and they reacted quickly when claims data came in that were not in line with expectations. She pointed to the company’s history as a sign of confidence in the overall reserving methodology, a claim that seems justified based on the long term record:

Market participants initially reacted negatively to Progressive’s quarterly results with the stock declining on May 2 when the quarterly report was released. However, the stock has partially recovered over the past two days.

Hopefully this brief review of Progressive’s recent results has been useful for Berkshire shareholders who are awaiting information on GEICO in tomorrow’s first quarter report. I suspect that there will be several questions on GEICO during the Q&A session of the annual meeting.

GEICO’s CEO Todd Combs was recently interviewed on the “I Am Home” podcast hosted by Nebraska Furniture Mart. The conversation was mostly related to how Mr. Combs initiated a conversation with Charlie Munger in 2010 which eventually led to being hired as an investment manager by Warren Buffett.

Although the discussion did not center on GEICO, it is definitely worth listening to. It will be interesting to see if Mr. Combs remains as CEO of GEICO while also managing investments. His workload sounds extremely heavy which is to be expected since he has two demanding full time jobs!

Copyright, Disclosures, and Privacy Information

Nothing in this article constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC. The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Individuals associated with The Rational Walk own shares of Berkshire Hathaway.