Are you merely average?

If you are reading this article, chances are that you will instinctively recoil when asked this question. People do not like to think of themselves as merely average and this is even more true for individuals who have selected careers in business. We live in a hyper-competitive world where professional identity and self esteem depends on having above average insights and achieving superior results. The cognitive bias known as illusory superiority is behind the tendency of individuals to overestimate their ranking relative to peers. This phenomenon has been shown to be true in ordinary activities like driving and it certainly seems to extend to investing.

Active investing requires the recognition of certain fundamental realities. The world is full of intelligent people who have access to the same information at the same time, and this has only been accentuated by the internet. Additionally, there are plenty of people who might have special insights due to longtime involvement in an industry or familiarity with key decision makers at a company. This doesn’t necessarily imply illegal inside information although it would be naive to think that one isn’t competing against people with access to such information and willingness to act on it. If we are going to rationally choose to be active investors, we must believe that we have some type of edge over other market participants. Merely reading SEC filings and newspapers is not enough to provide such an edge.

The Rise of Passive Investing

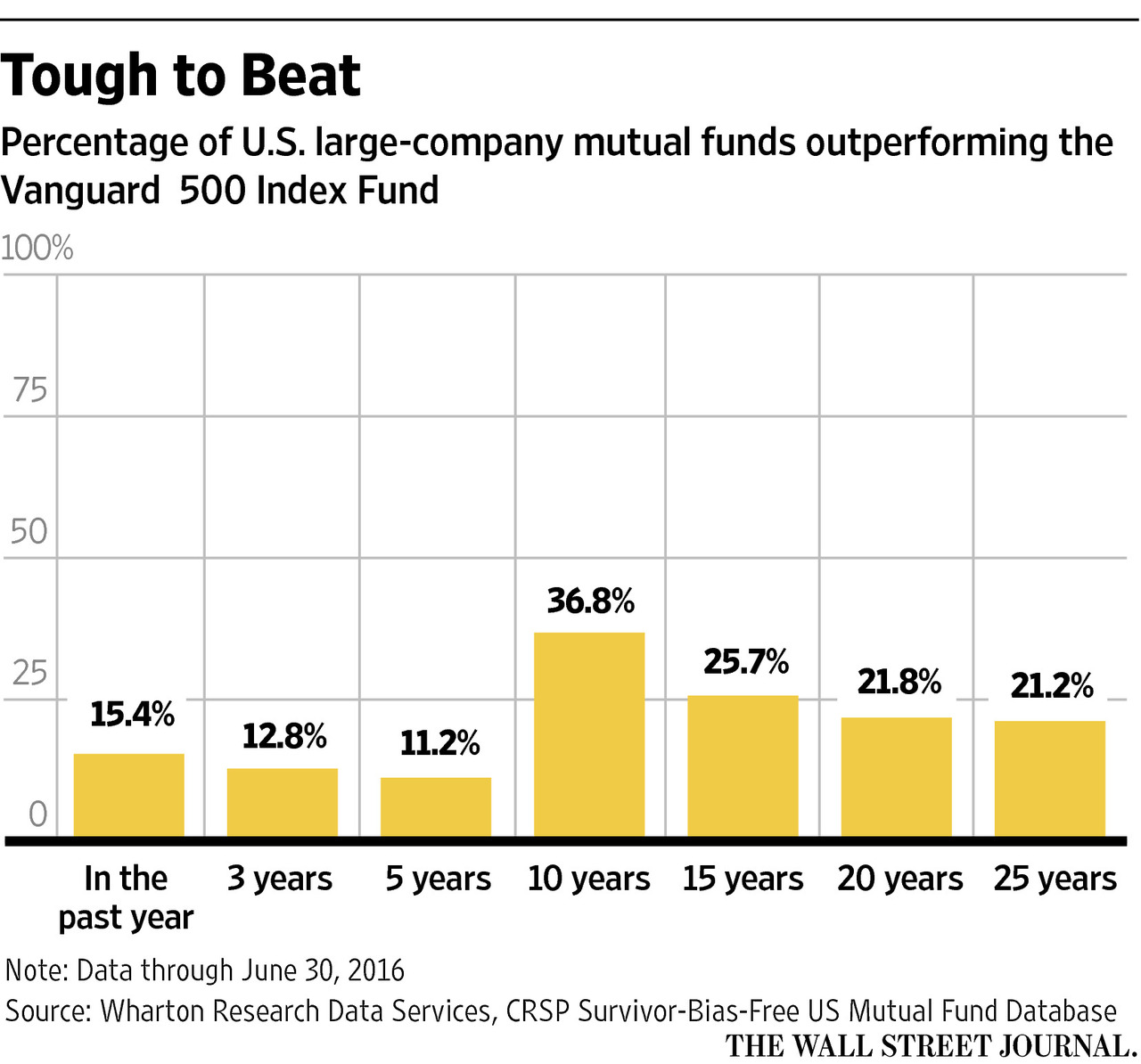

The Wall Street Journal is running a series this week exploring the rise of passive investing. Passive investing has been a viable option for the past four decades ever since Jack Bogle created the first index fund accessible to ordinary investors. The idea of indexing is to match the performance of the broad stock market (or whatever sector is being indexed) rather than to make any attempt whatsoever to pick winners and avoid losers. This could be done at much lower cost even in the 1970s and the advantage of passive indexing has only grown more pronounced over the years as assets under management increased dramatically allowing for progressively lower management fees. The Vanguard Group, which became the dominant player in indexing under Mr. Bogle’s leadership, has been joined by many other firms eager to capitalize on this trend. Indexing has become the default choice in many company retirement plans. As the following graph from The Wall Street Journal illustrates, indexing has outperformed the vast majority of active fund managers.

Index funds incur low fees and index fund managers have no psychological impulses to deal with. They simply own all stocks in a given index in an effort to be average. Obviously, some actively managed funds have demonstrated that they can outperform but outperformance during a period in the past does not necessarily allow us to predict whether such returns will continue into the future.

But none of this applies to most of us, right? As value investors following the principles of Benjamin Graham, Warren Buffett, and Charlie Munger, aren’t we immune to the folly that makes the majority of active managers fail? Unfortunately, this is not necessarily the case. For one thing, the number of “value investors” competing for ideas is hardly small. Mr. Buffett’s record and the simplicity that seems to underpin his success leads many people to seek to emulate the approach. Few will come anywhere close to succeeding both because the actual process is not simple and because the temperament required to succeed is rare.

As we argued last year, individual investors have many important advantages over professional investors. In particular, with no outside constituency to manage, individuals can exploit timeframe arbitrage to their advantage provided that they themselves have the temperament required to do so. However, it is worth questioning whether the typical individual investor should attempt to outperform even if he or she has the skills and temperament required to do so.

Settle For Average?

From a purely mathematical standpoint, it takes a relatively large portfolio and/or a significant degree of outperformance to logically induce an individual investor to seek to outperform an index fund. Let’s consider a simple example. A 50 year old marketing executive has a $1 million 401(k) account accumulated through diligent payroll deductions and compounded investment returns over a period of 20 years. The money has been invested in a selection of the mutual funds offered by his employer and individual security selections were not permitted. Let’s say that this investor leaves his company for a better opportunity within the field of marketing and rolls the 401(k) into a self directed IRA. He will not need to draw any funds from this account until reaching the age of 70. Should he actively manage that $1 million portfolio or index it?

Obviously the answer to this question is not simple. Does this individual have a special circle of competence in one or more areas that could provide a discernible edge over other market participants? Does he have adequate time to devote to research and the inclination to spend his time on research outside of his normal day job? Does he have the appropriate psychological temperament to view his investments as long term commitments or will he start to actively trade at precisely the wrong time? If all goes well, what is the margin of outperformance that he expects to achieve?

For one thing, it is probably not possible to answer many of these questions unless the individual has an existing track record outside his $1 million self directed IRA. If he does not, he almost certainly should index. However, let’s assume that the investor has managed a smaller account successfully over the past decade and has achieved returns 1.5 percent greater than the S&P 500 index. Let’s further assume that he read Poor Charlie’s Almanack in 2006, started attending Berkshire Hathaway annual meetings, and has ever since made an effort to expand his circle of competence through a multi-disciplinary framework. He enjoys reading and is eager to spend around 500 hours per year on intellectual pursuits including the selection of investments for his portfolio.

The Temptation

Our investor appears to be a candidate for active investing but is it worthwhile? Let us assume that the S&P 500 will average 6 percent total returns over the next two decades given the fact that valuations are hardly at bargain levels today. If an investor expects a 1.5 percent outperformance, then that would imply returns of 7.5 percent. Keep in mind that this small margin is actually a very significant difference that few professionals can hope to achieve even working on a full time basis. However, our investor feels confident that he can achieve this margin by devoting 500 hours per year to the endeavor.

Based on these assumptions, and with the obviously incorrect assumption that returns will be smooth, the expected result would look something like this:

If you look at the expected account value in the early years, the difference is fairly small but eventually compounding does its magic and the end result of active management, given our oversimplified assumptions, will be about $1 million over what is delivered by the index fund. Looking at the difference in early years shows that the effort expended in achieving the outperformance might be questionable: In year one, for example, the 1.5 percent margin of outperformance results in a dollar difference of only $15,000 in exchange for 500 hours of effort which works out to $30 per hour, far below the value our investor attaches to his time, both in his day job and for leisure. However, a sustained effort will eventually lead to a material difference in the final account value.

Simple Assumptions Are NOT Reality

The rather naive assumptions and smooth curve of outperformance shown above is far from reality. Instead of a smooth curve, the natural volatility of the stock market will result in a much more variable picture from year to year. The chart below shows exactly the same endpoint for the active and passive strategies but with a more plausible variation of annual returns:

So our hypothetical investor begins by falling short of the index for four years before pulling ahead until year fourteen when his investments are suddenly viewed unfavorably by Mr. Market. Diligence and a steady temperament pays off in the subsequent years, however, and we end up with the same $1 million margin over the index at the end of the twenty year period.

How many investors, in reality, would stick with this more realistic scenario for the first four years? How many would still stick with it after posting cumulative underperformance after fourteen years? Would most people begin to question whether their circle of competence is real when faced with a brutal verdict from Mr. Market so many years into the process?

Ultimately, investors need to assess their ability to outperform, the level of effort required if one chooses to make the attempt, and the very real psychological pressures that could cause the effort to be abandoned during difficult times. Anyone who cannot confidently claim to have the ability based on an actual track record should index. Anyone who does not want to put in the level of effort required should index. And unless one has been through difficult times in the past and acted with a steady hand, it is probably best to index.

We end up with something of a chicken vs. egg conundrum: How can anyone know whether they have the ability to succeed without trying? And how can we know how we will truly react to adversity without putting ourselves in situations that test our resolve? The answer is that we cannot know the answers to these questions without putting ourselves out there in some way and making the attempt. If there is a desire to engage in the process, which many investors truly enjoy, it seems prudent to enter the competition with a meaningful enough amount of money to test one’s ability and psychological tendencies, but to start out by indexing the rest. It isn’t possible to test ourselves using a “paper account”. We have to have actual “skin in the game” to see how we will react to the many psychological pressures that conspire to make even those with above average aptitude achieve only average results.

Ultimately, there is no shame in being merely “average” when it comes to investing but there would be cause for regret if one posts consistently inferior returns due to an overly optimistic self-assessment of skill or psychological makeup.