“True knowledge exists in knowing that you know nothing.”

— Socrates

The twentieth century was one of the most momentous in human history. Technology altered every sphere of politics, business, and day-to-day life to the point where the lifestyle of people at the turn of the twenty-first century bore almost no resemblance to those living at the turn of the twentieth. Yet one hundred years is only a minuscule fraction of the two hundred thousand years that Homo sapiens have inhabited the earth. To put this in perspective, 99 percent of human existence took place before the lifetime of Jesus Christ and 99.75 percent took place before the discovery of the New World.

The pace of visible change in our world, driven by amazing advances in human knowledge, can trick us into thinking that the psychological pitfalls that afflicted prior generations no longer apply to us. But nothing could be further from the truth. The reality is that, at an evolutionary level, a few hundred years means very little and human misjudgment of the realities of our modern environment is widespread. We can study aspects of our psychological makeup which lead to misjudgment but we cannot trick ourselves into thinking that knowledge of these pitfalls makes us fully immune.

Financial markets have certainly changed a great deal since 1940 when Fred Schwed published Where Are the Customers’ Yachts. Schwed wrote at a time when investors were skeptical regarding the stock market. The 1929 crash took place a decade earlier and stock prices were still far from the record highs. The Second World War was underway with Nazi Germany on the rise. Surely, a book regarding Wall Street written at that time would be a relic of a bygone age, one that has little relevance to us today? Yet, that is not the case at all. Anyone who spends a few hours reading this book today will, between bouts of uncontrolled laughter, recognize that very little has changed in terms of human behavior. As Michael Lewis writes in the introduction to the book, “What Schwed has done is capture fully — in deceptively simple language — the lunacy at the heart of the investment business: the widely held belief that there is someone out there who can tell you how to turn a little money into a lot, quickly.”

Passion for Prophesy

The spring of 2020 is one of the most uncertain times in recent memory with the COVID-19 pandemic underway and financial markets unsure of how to interpret the tsunami of incoming information. The demand for forecasts might be at an all-time high, but as Howard Marks pointed out recently, the future is determined by thousands of factors that must be accurately weighed and very few, if any, people are capable of balancing all of the relevant factors and assessing future risks and returns. One might say that there is a “passion for prophesy” today.

As Schwed pointed out eight decades ago, that passion for prophesy has always existed when it comes to financial markets. Investors are not content to make their own decisions and merely seek efficient execution of their trades.

For one thing, customers have an unfortunate habit of asking about the financial future. Now if you do someone the signal honor of asking him a difficult question, you may be assured that you will get a detailed answer. Rarely will it be the most difficult of all answers — “I don’t know.” …

But I doubt if there are many, or any, Wall Streeters who sit down and say to themselves coolly, “Now let’s see. What cock-and-bull story shall I invent and tell them today?” I don’t think you can supply any guarantee of accuracy when looking into the heart and mind of someone else. But I feel, from years of personal observation, that the usual thought process is far more innocent. The broker influences the customer with his knowledge of the future, but only after he has convinced himself. The worst that should be said of him is that he wants to convince himself badly and that he therefore succeeds in convincing himself — generally badly.

Where Are the Customers’ Yachts?, p. 16-17

Schwed wisely applies the concept of Hanlon’s Razor in this case, choosing to give the benefit of the doubt to those who meet the perennial demand for market forecasts. He could not have imagined the modern financial landscape with networks like CNBC providing nonstop market commentary along with interviews of dozens of prophets who appear every day to furnish the interpretation of events that viewers so desperately seek. The vast majority of these commentators are not trying to deceive anyone. As in Schwed’s day, they have either personally studied massive amounts of data or relied on economists at their firms who have done so. And they believe that these studies provide an edge when it comes to divining the course of future events. Schwed dryly observed that “the notion that the financial future is not predictable is just too unpleasant to be given any room at all in the Wall Streeter’s consciousness.”

Cash is Trash

Following the financial crisis and recession of 2008-09, interest rates in the United States have remained at very low levels which has made it very difficult for investors to realize meaningful income from risk-free assets such as U.S. treasury securities. Interest rates were also at very low levels in 1940 when Schwed published his book. Investors may have been scared of investing in the stock market, but “doing nothing” and staying in cash was painful as well. Schwed refers to customers who dread having any cash as suffering from a psychiatric disturbance called “rhinophobia”.

Customers who suffer from rhinophobia always have as many securities as possible. When they sell out stocks at a profit they hasten to fill the void in their accounts with other stocks. The odd part is that they are frequently economical souls who do not believe in frittering away their money on food and drink and momentary pleasure … To them, having a sizable cash balance in an account for any length of time is unbearable. Suppose stocks should go way up? They would be left high and dry with nothing but some dirty old money.

Where Are the Customers’ Yachts?, p. 62

Sounds familiar, doesn’t it?

Rhinophobia affects small and large investors alike, as we saw in January when Ray Dalio referred to cash as trash:

Ray Dalio, founder of investment firm Bridgewater Associates, said Tuesday that he thinks investors shouldn’t miss out on the strength of the current market and that they should dump cash for a diversified portfolio.

“Everybody is missing out, so everybody wants to get in,” Dalio said on CNBC’s “Squawk Box” at the World Economic Forum in Davos, Switzerland.

Dalio advised having a global and well-diversified portfolio in this market and said the thing people can’t “jump into” is cash.

“Cash is trash,” Dalio said. “Get out of cash. There’s still a lot of money in cash.”

Source: CNBC article dated 1/21/2020, retrieved on 5/19/2020

Ray Dalio was not alone in January. Few investors, large or small, wanted to be sitting in cash at a time when stock markets were posting record highs. Although investors knew about the emergence of a strange new disease in Asia, very few thought that it would have a massive impact on the U.S. economy. Prophesy was difficult in 1940 and it remains difficult in 2020.

Leverage

If cash is trash, and it certainly seems to be in bull markets, the next seemingly logical step for an investor to take is to not only be fully invested in stocks but to borrow some money at an attractive interest rate to buy even more stocks. During the 1920s stock market boom, margin requirements were not yet regulated and customers could shop around at different brokerages which competed for business based on low margin policies. By 1940, margin requirements were fixed, but Schwed notes that the practice still tempted investors:

Americans find margin trading a particularly attractive little invention. It parallels the American principle that the first thing a man should do with his home, even before moving in, is to put it in hock. The idea is that he only has to pay six per cent or so on the mortgage and if he can’t wangle something better than a measly six per cent out of a round lot of money, he ought not to be in business. This is another argument I am unable and unwilling to discuss further.

The idea is easily extended to margin trading. We assume that it is a wise and profitable venture to buy 100 shares of United Fido at ten, paying $1,000 for it. Ergo, wouldn’t it be even better to buy 200 shares paying the same $1,000? And even better to make it three or four hundred if we can find a sufficiently kindly broker to do us this favor?

The answer is no. But I only know one way of proving it to you conclusively. Go try it.

Where Are the Customers’ Yachts?, p. 54

Certain lessons can only be learned by actually losing money. Testing your strategies with a “paper portfolio” will not do the trick. It is one thing to lose money on paper and quite another to lose real money, as Schwed dryly notes: “There are certain things that cannot be adequately explained to a virgin either by words or pictures. Nor can any description that I might offer here even approximate what it feels like to lose a real chunk of money that you used to own.”

Leverage can be deadly but has tempted investors throughout history. Intelligent investing in stocks might be a good strategy to get rich. But the compounding effects on small amounts of wealth can seem agonizingly slow for many years before it “snowballs” into real wealth.

As Charlie Munger once said at a Berkshire Hathaway annual meeting, “We get these questions a lot from the enterprising young. It’s a very intelligent question: You look at some old guy who’s rich and you ask, ‘How can I become like you, except faster?’” Well, one way to try to get rich “faster” is to use leverage. As Schwed said eighty years ago, this is a false illusion that every generation of investors seems to have to learn anew.

Buying the “Best Securities”

In 1979, Warren Buffett wrote an article entitled “You Pay a Very High Price In The Stock Market For A Cheery Consensus”. Buffett noted that in 1972, pension fund managers could not buy stocks fast enough, which was reflected in their lofty prices. The early 1970s were the height of the “Nifty Fifty” period when the prices of “stocks of the future” were bid up to dizzying heights. Fast forward to 1979 when, after experiencing a bruising bear market in 1973-74 and subsequent years of economic malaise, fund managers were placing orders for stocks “with an eyedropper.”

Four decades earlier, Schwed warned his readers about the perils of buying the “best” securities, that is, those securities that are merely popular at a given point in time:

The pathetic fallacy is that what are thought to be the best are in truth only the most popular — the most active, the most talked of, the most boosted, and consequently, the highest in price at that time. It is very much a matter of fashion, like Eugenie hats or waxed mustaches. When crinolines were being worn, canal bonds were being bought; when the bustle was thought attractive, so were railroad and traction securities. To say that industrial common stocks were all the rage in the late 1920s would be to understate it, and le denier cri for the last few years has been for government bonds and tax-exempts at prices calculated to yield something near zero per cent. Interspersed with such major fashion trends there appear at various times briefer foibles — sudden passions for “war babies”, auto stocks, radio stocks, bank stocks, real-estate mortgages, convertible debentures.

Where Are the Customers’ Yachts?, p. 78-79

Schwed notes that the basic trouble with all of these trends is that people are buying not necessarily the “best” securities but merely those that are most popular at a given point in time. And that popularity itself accounts for prices that often are out of proportion to business prospects. “Implacably, this universal habit of buying the popular securities works for bad results over a period of time.”

The crucial distinction between future prospects for a business enterprise and prospects for its securities is one that generation after generation of investors fail to make. A business with compelling future prospects can make for a lousy investment if its securities are so popular that its bright future is more than fully reflected in the price one must pay to participate.

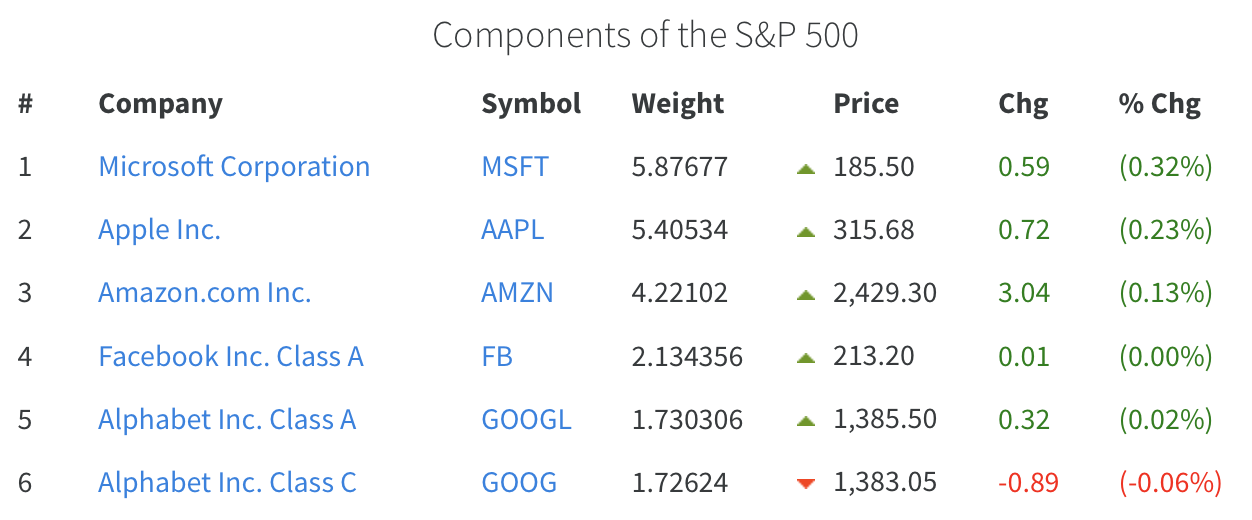

As of May 2020, the top five companies in the Standard & Poor’s 500 comprise over 21 percent of the index:

Microsoft, Apple, Amazon, Facebook, and Alphabet are indisputable leaders of our modern economy. Their stocks are also popular not only with active investors but with index funds that automatically purchase these stocks when they receive new inflows of investor funds. Without commenting on the valuation of these companies, we can note that they are undoubtedly popular stocks in 2020. Their popularity might be justified by the underlying business fundamentals or investors may be repeating the “universal habit” of buying what is popular and suffering poor results over time. At the very least, buying popular stocks should always be done with great caution.

Nothing is Ever Enough

Another perennial truth that Schwed describes is the tendency for people to always seek a level of income from their assets that pushes the envelope of what can be prudently attained. This results in the investor, or his advisor, committing the cardinal sin of “reaching for yield”, either literally through the purchase of higher yielding, but riskier fixed income securities, or through more aggressive investments in equity securities.

As a brief thought experiment, consider why reaching for returns is so common. Take a person who has accumulated a sum of $2 million over a number of years through success in running a business. This level of net worth would put this person at the 94th percentile of wealth in the United States.1 Let’s say that this person wishes to retire and draw income on that $2 million for his or her income. If we assume a 3 percent withdrawal rate, the income that can be safely drawn is about $60,000 per year which approximates the median household income. But will a person who has wealth greater than 94 percent of Americans be satisfied with an income that is merely at the median?

The emphasis in the investment problem is usually placed on the proper selection of securities. I suggest that the emphasis would be better placed on how the investor intends to spend his income. The initial mistakes are made in this latter department; the wrong securities are chosen largely as a result of this initial philosophic error.

Where Are the Customers’ Yachts?, p. 150

Just as in 1940, an investment advisor can “fix” the problem of insufficient income and “arrange the larger yield in a jiffy if the family asks for it…. He simply sells out the conservative bonds and substitutes riskier securities.”

Reaching for returns has tempted investors for generations and will always tempt investors because someone who has a net worth of a few million dollars typically feels “rich” and is dissatisfied with only consuming the median income. And one can extrapolate this for higher levels of wealth as well. How many individuals with a net worth of $10 million would be satisfied only drawing $300,000 per year? Clearly some will, but not most. Social proof and the simple temptation to consume will almost always militate against conservation of wealth and lead to a desire for more income. Sometimes the quest for higher income will work out well over time but more often it will end in tears.

The More Things Change …

Rapid technological change can trick us into thinking that the fundamental nature of human beings has changed commensurately, but nothing could be further from the truth. In terms of biological evolution, we are not very different from human beings who lived thousands of years ago in hunter-gatherer cultures that bear no resemblance to our current world. We have inherited the psychology of our ancestors and must work within the constructs of that psychology.

Our advantage as human beings with a sense of history is that we can choose to be aware of the many sources of psychological misjudgment that can afflict us. Although we can never be immune from misjudgment, we can avoid many mistakes if we make a deliberate effort to check ourselves at points where others have gone badly astray.

Fred Schwed’s tales of Wall Street in another era reinforces that today’s investors are not that different from those who lived nearly a century ago. As Jason Zweig notes in his introduction to the book, “Schwed’s is the only financial book, out of hundreds I’ve read, that will provoke you, teach you, and crack you up all at once.”

- Net worth percentile calculator based on 2017 data, retrieved on 5/19/2020. [↩]