The current banking crisis has led to calls for the government to insure all bank deposits, but doing so has significant long term implications.

A healthy banking system is a prerequisite for a functional modern economy. Individuals and businesses entrust financial institutions with their savings in exchange for banking services and the opportunity to earn interest on their funds. Banks compete for deposits on the basis of the services they provide to customers and the interest rate they are willing to pay to attract funds. The motivation for banks is to obtain a source of funding to make loans that carry an interest rate higher than the cost of funds. A bank expects to earn a net interest margin from its operations.

In a competitive market, certain banks will do a better job than others when it comes to providing banking services to depositors and making sound loans. A bank that provides excellent service to depositors might be able to gain an advantage by paying a lower rate of interest, thereby making it possible to offer loans at attractive rates while limiting loan losses. Over time, well run banks will gain market share and benefit from economies of scale while incompetent players will exit the industry.

What I am describing here is admittedly very basic, but at times over the past week I have felt that much of the coverage of the banking crisis has failed to distill what banking actually represents in a functioning economic system. The basic blocking and tackling of banking is essential for the economy. Chaos in banking has caused numerous financial panics that have led to economic depressions.

It is unrealistic to expect most individuals and smaller businesses to study the financial statements of banks to determine safety and soundness. It is ludicrous to visualize an ordinary American sitting down to compare deposit rates offered by banks and selecting one based on his or her assessment of the bank’s stability. The same is true for small businesses. Even if this was possible, it would be a terrible use of time. For the majority of individuals and businesses, the system just needs to work, and having to worry about bank stability would impede activity in the real economy.

But when it comes to large businesses and wealthy individuals, it is reasonable to expect that banking relationships will be chosen with a greater level of discernment. Large depositors are more likely to view themselves not only as consumers of banking services but as creditors of the bank. In a functional free market-based banking system, such depositors are supposed to act as “cops on the beat” and exert some level of judgment. If a bank is offering unusually high interest rates, the sophisticated depositor should ask whether this high rate comes with greater risk of loss.

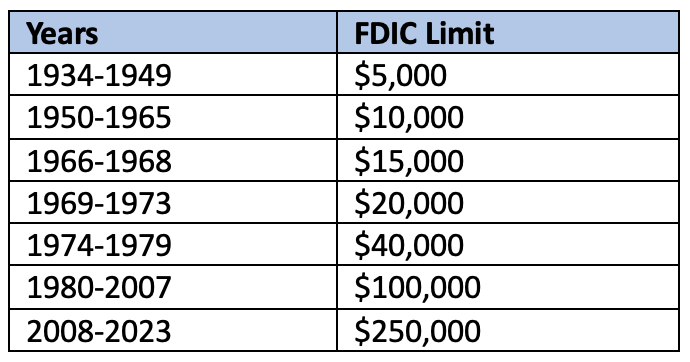

The Federal Deposit Insurance Corporation (FDIC) was created in 1933 to increase confidence in the banking system during the depths of the Great Depression. The cornerstone of the FDIC involved the establishment of deposit insurance intended to provide limited protection in the event of bank failures. The system is funded by assessments on banks to cover payments to depositors of failed institutions. Initial coverage at the beginning of 1934 was $2,500, but was increased to $5,000 later in that year. The exhibit below shows the level of insurance in effect over the years:

It is important to note that these figures are in nominal dollars. According to the BLS, $5,000 in February 1934 had purchasing power equivalent to approximately $113,000 in February 2023. Rather than adjusting the FDIC limit for inflation automatically, the level of protection has remained static in nominal dollars for long periods of time before shifting up in large increments.

The latest increase, from $100,000 to $250,000, took effect in October 2008 in the midst of the financial crisis. Initially, this was supposed to be a temporary increase but the Dodd-Frank reform Act passed in 2010 made the increase permanent.

At $250,000, the current level of FDIC protection is more than twice what was provided when the system was set up in 1934 after adjusting for inflation.

Bill Ackman, among others, has advocated for a “temporary” guarantee on all deposits until the FDIC deposit insurance can be set to an unspecified “larger guarantee” and deposit insurance fees can be “scaled based on the creditworthiness of the bank.” As noted above, the last time the system was in crisis, the deposit insurance limit was more than doubled from $100,000 to $250,000, supposedly on a “temporary” basis before the change was made permanent less than two years later.

If deposit insurance is unlimited for some “temporary” period of time, the FDIC would be expected to protect all depositors in the event of a bank failure making this week’s bailouts of Silicon Valley Bank and Signature Bank the standard operating procedure for all bank failures.

The FDIC insurance system is currently funded based on the assumption that there is a limit to deposit insurance. To the extent that the deposit insurance fund is insufficient, the FDIC will either have to raise assessments on banks, which is the plan to cover losses at Silicon Valley Bank and Signature Bank, or the government will have to provide additional funding to shore up the system. In either case, this will impose costs on the real economy and this must be recognized as part of the debate.

Aside from potential funding shortfalls, unlimited deposit insurance would eliminate any incentive for depositors of any size to care about a bank’s operations and financial stability.

As already noted, it is unrealistic and absurd to think that ordinary individuals and small businesses will ever exert this type of discipline on banks, but when did it become absurd to think that wealthy individuals and large companies should use judgment when it comes to where they invest their funds? It is sad to see fragile capitalists behaving in such a helpless way. Wealth and privilege comes with serious responsibilities and consequences, or at least it used to.

The absence of any market discipline from depositors to police the activities of banks will require the government to step up regulatory oversight of all banks in order to limit exposure of the government to losses. In the absence of market discipline from depositors and sufficient regulatory oversight, only the shareholders of banks will be left to care about enforcing sound banking practices. In reality, agency problems have become so severe that it is doubtful that effective oversight will occur.

One of the unfortunate consequences of the financial crisis is that the government allowed a small number of financial institutions to grow to truly gargantuan size and clearly become “too big to fail”. As a result, it is assumed that we already have “unlimited” deposit insurance for the largest banks while customers of smaller banks not deemed to be systemically important are limited to $250,000 of coverage. Rather than allowing banks to become too big to fail, government should have taken steps to prohibit concentration in banking that could lead to these types of systemic risks.

In the age of viral social media and instant communication, public discourse has been reduced to vapid sound bites. Rather than engaging in real debate, the typical tweet or message board discussion is full of straw man arguments and highly mendacious rhetoric, usually driven by an individual’s overall political inclinations. When everything in the public discourse is reduced what one is supposed to believe based on “red vs. blue” allegiance, we have lost the plot and will suffer severe consequences.

I am not aware of any serious person who advocates for a return to the days before any level of deposit insurance or some pure libertarian free market system in banking devoid of all government regulation. However, it is fair and essential to debate the proper level of deposit insurance that strikes a balance between protecting ordinary Americans and small businesses while allowing for market discipline, combined with regulation, to act as “cops on the beat” to police the banking system.

I am skeptical that “unlimited” deposit insurance for a “temporary” period of time will solve the serious problems facing the system. History shows that temporary measures often become permanent. That was the case when FDIC insurance was raised from $100,000 to $250,000 in 2008 and history is very likely to repeat.

We are approaching another “crisis weekend” during which policy makers will frantically meet to discuss how to respond before markets open on Monday morning. Policymakers have a responsibility to consider the long term effects of their decisions and those with large social media megaphones have a duty to avoid fomenting panic in an attempt to box policymakers into taking their preferred course of action.

Copyright and Disclaimer

Nothing in this article constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC. This website is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.