In Today’s Issue:

- Alchemy by Rory Sutherland

- Predicting the Future

- Money is the Megaphone of Identity

- Chick-fil-A’s Franchising Model

To read last week’s newsletter regarding Tesla’s recent stock rally, the panic of 1901, staying informed in a noisy world, and taming your cell phone, please click here.

Alchemy by Rory Sutherland

Rory Sutherland’s recent book, Alchemy (reviewed on The Rational Walk this week), is a highly entertaining look at the pitfalls that await those who seek to reduce human behavior to a set of equations. Sutherland’s background as Vice Chairman of Ogilvy has put him in a great position to observe the seemingly irrational aspects of consumer behavior. What might be seen as irrational, however, can often be better understood by thinking about what consumers are actually trying to accomplish rather than what they say they are trying to accomplish.

While this book may appeal most directly to people who are involved in advertising and marketing, it is actually an excellent and very funny look at human psychology. If you find Nassim Taleb’s style of writing compelling, you’ll probably also enjoy Alchemy. Both Taleb and Sutherland seem to enjoy taking on intellectuals who misunderstand human behavior and they specifically target economists. But even economists with a sense of humor will find themselves laughing out loud while reading the book.

If you prefer to learn more about the book in audio format, Sutherland recorded a podcast episode in November on EconTalk with Russ Roberts.

Readers interested in advertising might also enjoy a book review of “The Man Who Sold America”, a compelling biography of Albert D. Lasker (1880-1952), one of the pioneering advertising executives of the twentieth century. Lasker’s notable achievements include inventing the Sunkist and Sun-Maid brands, dramatically improving the performance of products such as Palmolive soap and Pepsodent toothpaste, and much more controversially, expanding the appeal of Lucky Strike cigarettes to women.

Predicting the Future

Intellectual humility is often in short supply among market forecasters, no matter how poorly prior predictions have panned out. The reality is that even the most brilliant observers of the world have often been totally wrong about predicting the course of future events.

In hindsight, we look at a period like the late 1920s and think that people were out of their minds to stay invested after the market crash of October 1929. We know that the carnage was not transitory and that stocks would continue to fall for several more years and not regain the 1929 highs for a quarter century. We know that the Great Depression was coming. We know that Nazi Germany and Imperial Japan were poised to strengthen throughout the 1930s and that the Second World War would break out in 1939.

Of course, we are suffering from hindsight bias. No one surveying the scene in October 1929 saw all of these events coming.

Morgan Housel’s latest essay, “History is Only Interesting Because Nothing is Inevitable”, takes us through a series of newspaper articles and quotes from the late 1920s that appear totally ridiculous in hindsight. How could experts at the time have been so foolish!

But they were not foolish. They just were not omniscient. And neither are we.

And, no, our ability to forecast isn’t any better in the 21st century. Check out this chart of Greece’s ten year government yield since 2012:

Did anyone in 2012 predict that Greece’s ten year government yield would be less than the U.S. ten year yield in 2020? I’m not aware of anyone who predicted that, but I do recall many predictions of the imminent end of the Euro, yet here we are eight years later.

Money is the Megaphone of Identity

Telling someone who is in poverty that “money doesn’t buy happiness” would be seen as insensitive and absurd because basic survival is at stake. If you fear becoming homeless if you cannot make your next month’s rent payment, philosophical musings about money not buying happiness sound ridiculous.

The truth is that a certain amount of money is needed for happiness because happiness cannot be achieved while under constant financial duress.

Yet, money cannot guarantee happiness.

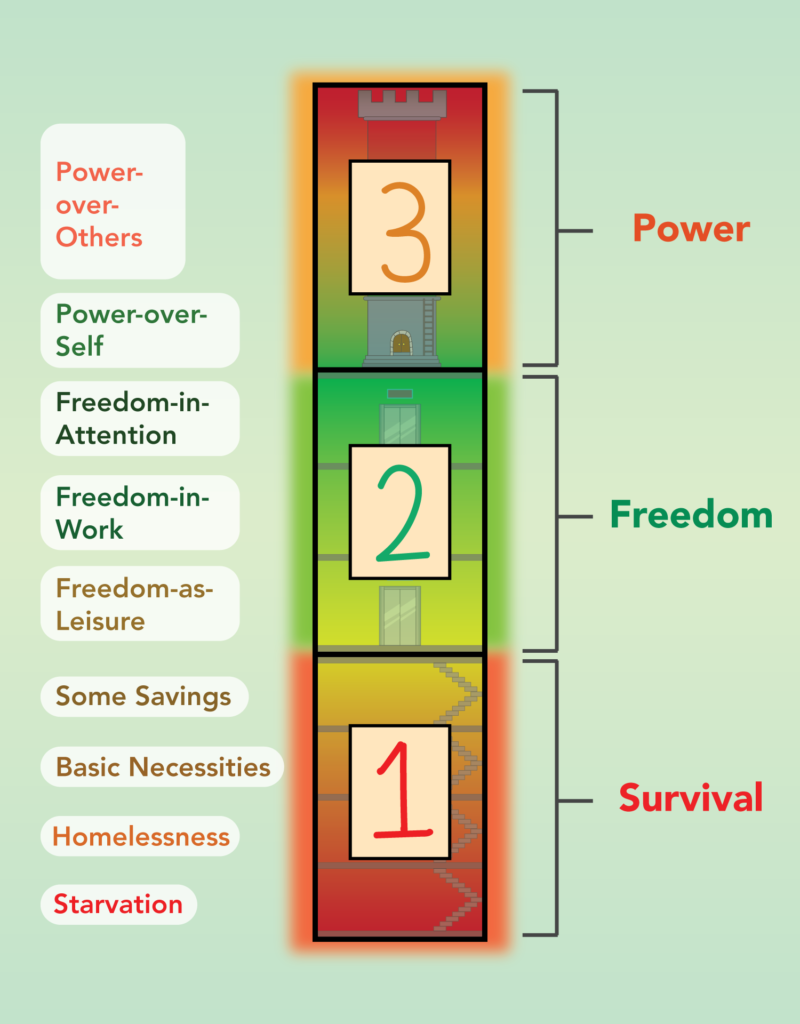

Lawrence Yeo takes on this interesting subject in “Money is the Megaphone of Identity”. He formulates an interesting framework for looking at the question of what utility money provides depending on the stage of life and the mindset of the individual involved:

Looking at the utility of money as a progression through the phases of survival, freedom, and power strikes me as a very useful exercise. Yeo makes excellent points regarding the power of money to buy freedom, but not in the sense of necessarily retiring to the beach. Money can provide freedom to pursue the type of work that you find fulfilling regardless of remuneration.

As Yeo points out, a person who earns $30,000 per year doing work that he loves to do, and would do for free, is “rich” if he only requires $20,000 per year to buy the kind of lifestyle he aspires to. And someone earning $300,000 per year is “poor” if he hates his job, has a huge amount of debt, and is barely scraping by.

There is nothing wrong with wanting a nice lifestyle but I think that people often ratchet up their spending without much thought as their income rises. Financial freedom is attainable for a large number of people but it isn’t possible to get there while consuming your entire income.

Chick-fil-A’s Franchising Model

I mentioned Chick-fil-A briefly in a previous issue of the newsletter as an example of a company that is impossible to replicate due to the intangible qualities of its brand. Naturally, management is very protective of the brand image and, as a result, has put in place a franchising model that is quite different from its competitors in the fast food industry.

In a recent article, Zachary Crockett explains how difficult it is to become a Chick-fil-A franchisee. The company is so careful admitting new franchisees that its acceptance rate is lower than Stanford University’s admission rate. One of the reasons the company gets 60,000 applicants per year is because the franchise fee is only $10,000. Chick-fil-A pays for and owns the land, structure, and equipment in franchised restaurants. The average competing chain requires franchisees to be worth a minimum of $1 million, with at least $500,000 of that liquid.

Of course, there is a catch. Chick-fil-A’s royalty fee is 15 percent of revenue, roughly triple the rate of competing chains. In addition, Chick-fil-A has claim to 50 percent of a franchised restaurant’s earnings whereas competing chains do not take a cut of earnings.

There are other restrictions. Chick-fil-A wants franchisees to be owner-operators active in the business and normally does not want one franchisee to own more than a single restaurant. Obviously, this is intended to ensure that the corporate culture remains intact through personal involvement.

As Crockett’s article notes, some critics say that these franchisees appear to be more like management employees rather than true business owners. And that is true, up to a point. However, the system allows franchisees with limited resources to get in the game and, once established as franchisees, they have significant skin in the game. This seems like a win-win proposition overall.

I am not alone in thinking that Chick-fil-A would be a great acquisition for Berkshire Hathaway since the Cathy family has pledged to never go public and has quirky policies such as remaining closed on Sunday that only an acquirer like Berkshire would be likely to respect. Such an acquisition seems unlikely and would be expensive. We know that Warren Buffett is at least familiar with Chick-fil-A … back in 2006, he exchanged letters with Truett Cathy.

That’s all for this week. The next issue of Rational Reflections will be sent out on Wednesday, February 19. Any feedback is welcome and can be sent to administrator@rationalwalk.com. Thanks for subscribing!

Was this email forwarded to you by a friend or colleague? Sign up here to receive Rational Reflections directly every week.

Copyright and Disclosures

Nothing in this newsletter constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.