“More people should copy us [Berkshire Hathaway]. It’s not difficult, but it looks difficult because it’s unconventional — it isn’t the way things are normally done.”

— Charlie Munger, 2000 Wesco Financial annual meeting

Alleghany Corporation is a holding company founded in 1929 with a long history of success operating in a variety of industries. The company’s objective is to create value through its property and casualty insurance and reinsurance operations as well as through ownership and management of non-insurance operating subsidiaries and investments. Alleghany has been led by President and Chief Executive Office Weston Hicks since 2004. Shareholders’ equity was $7.8 billion and book value per share was $503.43 as of March 31, 2016 compared to a recent market quotation of $515 per share.

The company is managed by a small headquarters staff responsible for capital allocation and overall strategic direction while operational responsibility is delegated to subsidiaries that operate in a “quasi-autonomous” environment. At least at a surface level, Alleghany’s management approach and corporate structure appears to take several pages from the well known Berkshire Hathaway playbook. It is worth taking a look at the company to see whether it represents a “mini Berkshire”, particularly given the modest valuation in terms of price-to-book value.

Overview

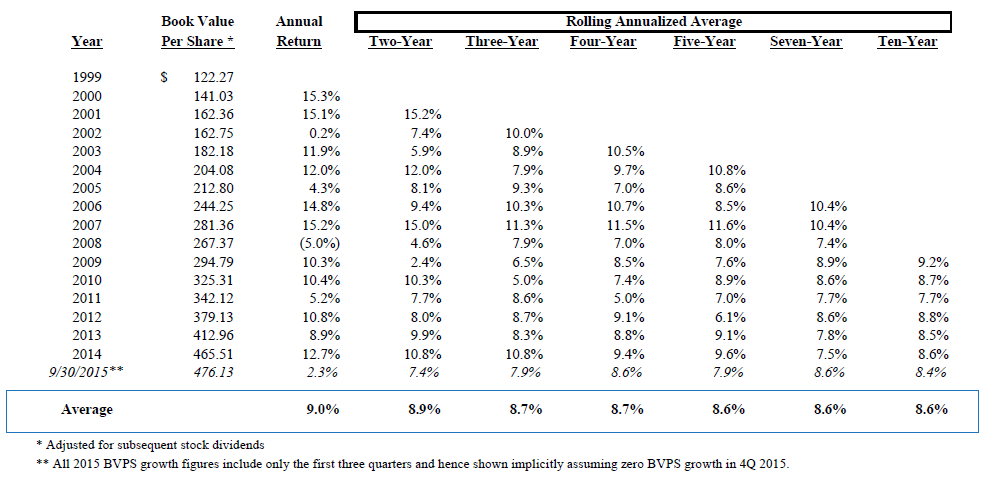

Alleghany’s stated objective is to compound book value per share at seven to ten percent over long periods of time. While this objective seems modest, management believes that it can be achieved at relatively low risk. Over the past decade, book value has indeed progressed at a rate that is roughly in line with management’s current goal. For the ten year period that ended on December 31, 2015, book value per share grew at a compounded annual rate of 8.6 percent which compares favorably to the 7.3 percent annual return of the S&P 500. However, Alleghany’s performance compares unfavorably to Berkshire Hathaway and Markel with ten year growth rates of 10.1 percent and 12.4 percent, respectively.

The following exhibit, taken from a recent company presentation (pdf) shows that long term annualized returns have been quite consistent over the past fifteen years:

In his annual letter to shareholders (pdf), CEO Weston Hicks notes that he is satisfied with Alleghany’s relatively modest 4.4 percent gain in book value per share for 2015 given the low levels of returns available elsewhere in the capital markets. He also notes that over the past decade, Alleghany’s stock price has only compounded at 6.6 percent annually because the price-to-book ratio has compressed over time. Alleghany shareholder letters are very detailed and worth reviewing. It is quite clear that Mr. Hicks is trying to emulate Warren Buffett’s style when it comes to annual communications with shareholders.

The following slide from the investor presentation illustrates that Alleghany stock has typically sold at a discount to book value in the years since the financial crisis. We can see that book value growth has been fairly consistent with only one down year in 2008. However, the stock price, even when observed with only one price point per year, is clearly more volatile.

Although the exhibit shown below from a company presentation is slightly out of date, it is a good high level illustration of how management is allocating capital between the insurance subsidiaries, non-insurance activities, and investments. These specific business lines will be discussed in more detail later in this article. At this point, we would simply note that the vast majority of capital has been allocated toward insurance operations, and specifically toward reinsurance activities at TransRe. In contrast to Berkshire and Markel, Alleghany is clearly much more weighted toward reinsurance.

Insurance and Reinsurance Overview

Alleghany posted $4.2 billion in earned premiums in 2015 which was down slightly over four percent compared to 2014. The company reports results in two segments: Insurance and Reinsurance. Within the insurance segment, results are broken down into three operating units: RSUI, Cap Specialty, and Pacific Comp. Within reinsurance, results are broken down into property and casualty lines. 2015 underwriting profit was $467 million and the combined ratio was 89 percent. The charts below show the composition of earned premiums and underwriting profit for 2015.

Alleghany has posted underwriting profits on a consistent basis in recent years. The exhibit below shows the overall loss, expense, and combined ratio for all of the company’s insurance segments over the past decade. In addition, a breakdown of earned premiums as a percentage of total by segment is provided along with combined ratios on a segment basis.

As we drill into the positive overall record, we can see that the TransRe acquisition in 2012 was transformative in terms of the overall size of Alleghany’s insurance operations. It is also apparent that certain insurance operations have posted less than stellar results, although these units account for a relatively minor percentage of premium volume. Several of these observations warrant further explanation.

Transatlantic Re

Alleghany acquired Transatlantic Re in March 2012 for approximately $3.5 billion consisting of cash consideration of $816 million and 8,360,959 shares of Alleghany common stock. Total consideration was approximately $61.14 per TransRe share. The merger was announced on November 21, 2011. Earlier in 2011, a number of companies, including Berkshire Hathaway, were reportedly interested in acquiring TransRe. Berkshire made an offer of $52 per share for TransRe in August 2011. This is notable given the fact that Warren Buffett and Ajit Jain would have been unlikely to overpay.

Although Alleghany had to offer more than Berkshire in order to close the deal, it was still at a discount to TransRe’s book value and immediately accretive to Alleghany’s book value per share. At the time of the merger, Alleghany hired Joe Brandon, who previously ran Berkshire’s General Re operations in the 2000s, to oversee all of Alleghany’s insurance operations. Readers interested in additional merger details can refer to The Brooklyn Investor website which published a good summary of the merger event.

A summary of TransRe’s results since 2012 are shown in the exhibit below:

It is clear that the TransRe merger transformed Alleghany’s operations and made the company much more focused on reinsurance. Since the merger, TransRe has posted overall underwriting profits in all years with property lines performing at a lower combined ratio than casualty lines. Prior to the acquisition, TransRe had posted several consecutive years of underwriting profits. There are always concerns regarding reserve adequacy when an insurance company is acquired. Based on a review of Alleghany’s loss triangle in the 2015 annual report, it looks like reserving has been conservative so far.

Mr. Hicks makes a number of comments regarding the merger in his annual letter. He notes that TransRe’s book value has grown approximately $1.6 billion since March 2012 which is a compound annual growth rate of 9.5 percent. Considering the gain on bargain purchase (due to TransRe being acquired at less than book value) at the time of the merger, TransRe has contributed almost $2.1 billion to the growth of Alleghany’s book value. Alleghany’s book value per share is about 10 percent higher than it would have been had TransRe not been purchased. Although four years isn’t a very long time, initial results of the merger seem promising. Reinsurance pricing has been soft recently, as Warren Buffett and many others have noted, so it will be interesting to see how TransRe performs over the next several years.

RSUI

RSUI underwrites specialty insurance coverages in the property, umbrella/excess liability, general liability, directors’ and officers’ liability, and professional liability lines of business. Specialty coverage is required for difficult to place risks and is less regulated than standard markets. RSUI has a number of operating subsidiaries and conducts business through 125 independent brokers and 29 managing agents. RSUI was acquired in 2003 and has been focused on underwriting profits over multiple industry cycles. As a result, management has been willing to shrink premium volume when pricing is inadequate.

The exhibit below shows RSUI’s results over the past decade:

We can see that RSUI has been willing to shrink premium volume when necessary but it has been growing again in recent years. The combined ratio has been below 100 percent for each of the past ten years reflecting underwriting profitability.

Mr. Hicks reports that RSUI achieved modest renewal rate increases in all of its product lines except for property in 2015. He also notes that since Alleghany acquired RSUI for $628 million in 2003, RSUI has paid dividends to the holding company of $774 million. RSUI has generated over $1.5 billion of underwriting profits since the acquisition and its stockholders equity has compounded at 11.1 percent adjusted for dividends and capital contributions. RSUI is clearly a very good insurance operation and dominated Alleghany’s overall financial results until TransRe was acquired in 2012.

CapSpecialty

CapSpecialty writes property and casualty insurance and surety products such as commercial and contract surety bonds through 137 agents and 69 general agents primarily serving small and mid-sized businesses in the United States. The company was acquired by Alleghany in 2002 for $242 million.

Representing only 5 percent of Alleghany’s overall earned premiums, CapSpecialty is not very material to overall results. Mr. Hicks notes in the annual letter that management has been taking steps intended to return the company to underwriting profitability. However, we can see from the exhibit below that CapSpecialty has posted underwriting losses for the past five years. On an cumulative basis, the company has posted an underwriting loss over the past decade.

Pacific Comp

Alleghany acquired Pacific Comp’s predecessor company in 2007. Prior to 2009, the company’s main business was workers’ compensation insurance. In 2009, management determined that rates were inadequate due to the state of the California workers’ compensation market and stopped writing new and renewal business. In 2011, the company began writing a modest amount of coverage and the business has increased since that time. Pacific Comp currently does business in California and six additional states.

As one might expect based on its history, the results of Pacific Comp in recent years leaves much to be desired as we can see from the exhibit below:

With premium volume tumbling to very low levels after 2009, the combined ratio predictably shot through the roof. As business has increased again over the past few years, the combined ratio has declined but the overall operation is still unprofitable from an underwriting perspective. In his annual letter to shareholders, Mr. Hicks expresses some optimism regarding Pacific Comp’s prospects for restoring underwriting profitability. Time will tell whether this will be the case. However, at only 2 percent of overall earned premiums, Pacific Comp is not a major factor driving the overall performance of Alleghany’s insurance operations.

Alleghany Capital Corporation

As we noted earlier, Alleghany is seen by many observers as a “mini-Berkshire Hathaway” because it owns interests in a number of non-insurance operations and has a decentralized management philosophy that offers significant autonomy to subsidiaries. Alleghany Capital oversees the company’s private capital investments in non-insurance businesses. The strategy is to invest in closely held businesses where owners and managers are seeking a long term home to support growth.

The following exhibit from a recent investor presentation provides a high level overview of Alleghany Capital:

What is the value proposition that Alleghany Capital provides to potential sellers? Again, we can see the influence of the Berkshire Hathaway model when we take a look at a slide from a company presentation (pdf):

The Berkshire Hathaway comparison is not perfect. Subsequent slides in the presentation illustrate that the acquisition process is more involved and not the kind of “hand shake deal” that Warren Buffett is famous for. However, it is clear that Alleghany is promising many of the same benefits to sellers including preservation of their company’s culture and legacy as well as continued operational control. The entire presentation is worth reviewing since it contains more details regarding the rationale for past acquisitions including the companies listed below:

- Stranded Oil Resources Corporation. The company was formed in June 2011 and Alleghany has invested $243.9 million. Stranded Oil seeks to acquire legacy oil fields and apply innovative enhanced oil recovery techniques. The company commenced drilling operations in 2015 but delays were encountered and production is now expected to begin in 2016. Alleghany owns approximately 80 percent of the company. The company is not yet profitable with negative EBITDA of $19.7 million in 2015 according to Alleghany’s annual letter. It is unclear whether Stranded Oil has a profitable business model in light of current low energy prices and only limited disclosure exists in Alleghany’s financial statements.

- ORX Exploration. ORX is a Louisiana based oil and gas exploration company. Alleghany owns a 40 percent interest. The company has developed a number of regional resource opportunities known collectively as the “Louisiana Heritage Play”. According to Alleghany’s annual letter, the decline in oil and gas prices has had a negative impact and the ORX investment has been written down to zero. According to the 2015 10-K, there was a $25.8 million realized capital loss related to a non-cash impairment charge required to write off the ORX investment. Presumably a recovery in oil and gas prices will be required to realize value from this investment.

- Bourn & Koch. Alleghany acquired an 80 percent interest in Bourn & Koch in 2012 and increased its position to 88 percent at the end of 2015. The company is a manufacturer and retrofitter of precision machine tools and a supplier of replacement parts. According to the Bourn & Koch website, the company specializes in machine tools for gear manufacturing, surface grinding, boring and vertical tuning with all production taking place in Rockford, Illinois. The company was founded in 1975. At the end of 2015, Alleghany had received cumulative cash distributions of $24.8 million in comparison to a gross investment of $55 million. The company produced EBITDA of $5.9 million in 2015 compared to $6.4 million in 2014.

- Kentucky Trailer. Alleghany owns an 80 percent equity interest in Kentucky Trailer as well as a preferred equity interest. The company’s website shows a large variety of custom trailers and truck bodies along with replacement parts. The company has roots going back to the establishment of the Kentucky Wagon Manufacturing Company in 1879. In October 2015, Kentucky Trailer made its third acquisition since Alleghany made its initial investment in Kentucky Trailer in 2013. This indicates that Kentucky Trailer may be a platform that can be used to allocate additional capital in the future. Alleghany has a cumulative gross investment of $42.6 million in Kentucky Trailer. In 2015, Kentucky Trailer generated EBITDA of $12.3 million compared to $8.3 million in 2014.

- Jazwares. Alleghany owns a 30 percent interest in Jazwares which is a Florida based toy company. Alleghany acquired its interest in Jazwares in July 2014 for $60.3 million and has received $13.4 million in cash distributions since the initial investment. Jazwares produced EBITDA of $35.8 million in 2015 compared to $41.3 million in 2014.

- Integrated Project Services (IPS). Alleghany acquired 84 percent of IPS in October 2015 for $89.9 million. IPS is a technical service provider focused on the global pharmaceutical and biotechnology industries. IPS generated EBITDA of $16.5 million in 2015. Alleghany’s share of 2015 EBITDA during its period of ownership was $1.3 million. According to the 2015 annual letter, IPS entered 2016 with a significantly larger backlog than at the start of 2015 which could presumably indicate higher earnings for 2016.

In addition to the businesses listed above, Alleghany owns and manages properties in the Sacramento, California region through Alleghany Properties, a wholly owned subsidiary. Alleghany properties owns improved and unimproved commercial land as well as residential lots. Total land holdings was approximately 317 acres at the end of 2015. According to the 2015 annual letter, Alleghany properties completed its first property sale in late 2015 since the 2008 financial crisis and a small profit was reported for 2015.

Alleghany’s financial supplement (pdf) for the first quarter of 2016 contains new disclosures for Alleghany Capital that do not exist in prior supplements. The results for Alleghany Capital are broken down into “manufacturing and services” and “oil and gas”. Although we do not have granular quarterly results for each of the businesses listed above, it is evident that the manufacturing and services group is profitable while the oil and gas sector is not. This is unsurprising given the current energy pricing environment.

It is difficult to come to any firm conclusions regarding Alleghany’s venture into non-insurance operations. These acquisitions have been relatively recent and the energy related companies skew the overall results negatively. Alleghany Capital represents a very small percentage of the total company’s capital at this point so the results here are not terribly material. Nevertheless, these ventures should be scrutinized over the coming years since much of the “mini Berkshire” narrative is based on diversification into controlled or wholly owned subsidiaries outside insurance.

Roundwood Asset Management

Alleghany’s public equity investments, including assets held by insurance subsidiaries, are managed primarily through Roundwood Asset Management which is a wholly owned subsidiary. These investments are funded both with shareholders’ equity as well as policyholder float. As of March 31, 2016, Alleghany’s investment portfolio was slightly over $17 billion with 17 percent invested in equities, 80 percent invested in fixed income securities, and the remainder invested in short term investments. The exhibit below shows the allocation of the investment portfolio:

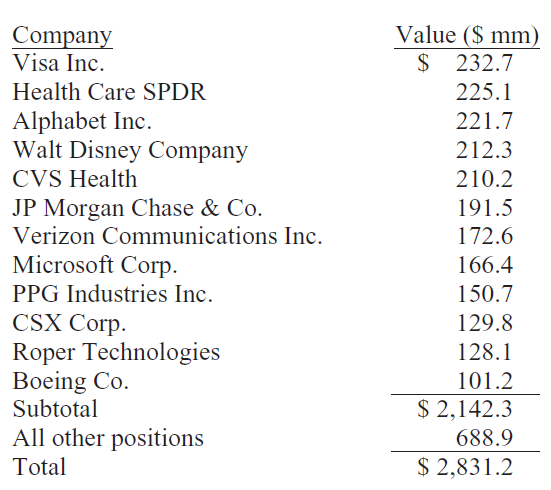

The effective duration of the fixed income portfolio was 4.6 years as of March 31, 2016 with the majority rated AAA or AA. Alleghany’s stated investment strategy is to preserve principal and liquidity while maximizing risk adjusted after-tax rate of return. Although equity investments represent a small percentage of total investments, management characterizes the approach as “research intensive” and focused on finding companies that can reliably grow revenues, earnings, and dividends over time. The following exhibit taken from the 2015 annual letter shows the composition of the equity portfolio as of December 31, 2015.

The approach is quite concentrated with the top seven positions accounting for more than half of the portfolio’s value. At $2.8 billion, the equity portfolio size is small enough to invest meaningful sums in companies with relatively small market caps so it is interesting to note that most of the top positions are very large capitalization companies. According to a recent invest presentation, the equity portfolio provided a 10.6 percent compounded annual return for the three years ended September 30, 2015.

Conclusion

This article has provided a fairly high level overview of Alleghany Corporation primarily intended to examine whether the company might be considered a “mini Berkshire” in terms of its overall operating strategy. Alleghany is a company with a very long track record as well as long serving and experienced management. The company has clearly shifted its strategy numerous times over the years in an opportunistic manner and has posted a compelling track record of book value growth. Book value growth has exceeded the S&P 500 over the past decade while trailing the performance of Berkshire Hathaway itself as well as Markel which is often thought of as a “mini Berkshire”.

Although Alleghany has many positive attributes, it is important to note that reinsurance is currently its dominant business and will be the primary driver of overall results. The insurance business, in aggregate, has been very good for Alleghany with combined ratios under 100 percent over the past decade. As a result, policyholder float in excess of $10 billion has been cost free and available to invest for the benefit of shareholders. However, many industry observers, including Warren Buffett, have noted that reinsurance pricing is currently inadequate. A reinsurance focused insurer like Alleghany will have to decide whether to reduce its premium volume (and float) or accept the risk of underwriting losses. Therefore, we cannot really view the $10 billion of float as a reliable cost-free source of funding for investments going forward.

It is probably too soon to evaluate the success of Alleghany Capital’s venture into non-insurance businesses. The companies that are not involved in oil and gas exploration seem to be profitable based on the limited data provided by Alleghany. But we simply do not have enough of a track record to evaluate the long term returns on capital invested in this area.

Market participants seem to be viewing Alleghany with some caution given the stock’s modest premium to book value. In recent years, shares have typically traded at a discount to book value and, at certain times, the discount has been quite large. Markel trades at a significant premium to book value (about 1.55x) so the market is viewing it as more of a “mini Berkshire” candidate at the moment. However, Markel has a much more diversified insurance business with less emphasis on reinsurance.

Alleghany appears to offer a reasonable value for risk averse investors seeking a conservative management team that is hoping to compound book value per share at a 7 to 10 percent annual rate. Purchasing a business of this quality at book value is probably going to work out reasonably well over time. More opportunistic investors might prefer to stay on the sidelines and wait for a meaningful discount to book value before buying shares.

Disclosure: No position in Alleghany. Individuals associated with The Rational Walk LLC own shares of Berkshire Hathaway and Markel Corporation.