CarMax shook up automotive retailing in the 1990s. Will the company face disruption by online competitors in the 2020s?

Introduction

CarMax was founded in 1993 as a subsidiary of Circuit City Stores. Circuit City was looking for growth and diversification opportunities outside consumer electronics. The automotive sector was identified due to its large size, high level of fragmentation, and reputation for low customer satisfaction. By bringing its experience in big box retailing to the used car market, Circuit City intended to disrupt automotive retailing by providing a wide array of inventory and a no-haggle shopping experience.

The initial rollout of CarMax locations was restricted to the southeast. By 1996, CarMax had five retail locations and $305 million in sales.1 Although the venture was weighing on Circuit City’s financial results at the time, management saw enough positive signs to pursue an aggressive national rollout of the CarMax concept.

In 1997, Circuit City created a tracking stock for CarMax and raised $412 million by selling 22.5% of the economic interest in CarMax to the public. Circuit City retained the remaining 77.5% interest in CarMax.2 Five years later, CarMax operated 41 retail locations and reported $3.2 billion of revenue and $91 million of net income.3

On October 1, 2002, CarMax became an independent, separately traded company. Owners of the CarMax tracking stock received one share of the newly independent company for each share of tracking stock they owned while Circuit City shareholders received 0.314 share of CarMax for each share of Circuit City they owned.4

To say that the next several years would not be kind to Circuit City is a major understatement. A series of management missteps followed by the 2008 financial crisis and economic downturn destroyed the business. Circuit City filed for bankruptcy in late 2008 and, despite efforts to arrange a restructuring, all stores were closed by March 2009 in a liquidation. Circuit City stock ended up being worthless.5

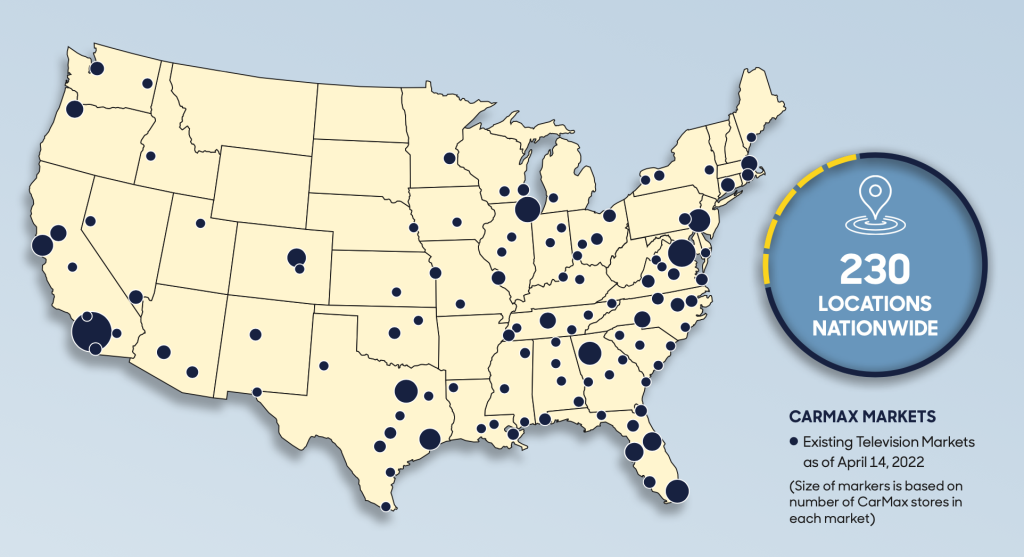

The story of CarMax is considerably happier. The company is now the largest retailer of used vehicles in the United States and operates 237 retail locations in 41 states.6 In the four fiscal quarters that ended on May 31, 2022, CarMax sold 1.6 million vehicles, recorded $33.5 billion of revenue, and brought $967 million to the bottom line.7

As the business has performed well over time, so has CarMax stock. The stock price has increased from a split-adjusted $8.15 on October 1, 2002 to $101.59 as of August 12, 2022. This represents a 13.5% annualized return and has outpaced the S&P 500 total return index, as seen in the chart below. CarMax has never paid a dividend. Total market capitalization stands at $16.2 billion.

While CarMax has done very well over the past three decades, it is always hazardous to grow complacent in a competitive business environment. The history of the company’s former parent presents cautionary lessons. While there were many reasons for the downfall of Circuit City, one important factor involved management’s failure to adapt its sales approach to compete with Best Buy:

… Circuit City didn’t see Best Buy as a threat. “We thought we were smarter than anybody,” says Alan Wurtzel, who remained on the board of directors until 2001. “But the time you get in trouble is when you think you know the answers.”

The Rise and Fall of Circuit City by Jessie Romero.

Alan Wurtzel is the son of the founder of Circuit City and served as the company’s CEO from 1972 to 1986.8 In a 2013 interview, Mr. Wurtzel cited hubris as a significant element in the decline and ultimate fall of Circuit City. In particular, he observed that management did not take the threat of Best Buy seriously because they believed that it was skating on thin ice financially and would likely fail.

It turned out that Best Buy’s retail approach was a better fit for what consumers actually wanted, and Circuit City shareholders paid dearly for the hubris of the company’s management in the long run. Circuit City’s management was simply not paranoid enough to take the threat seriously. This proved to be fatal.

Over the past quarter-century, we have repeatedly seen consumer preferences change in ways that might have initially seemed quite unlikely. Often, new competition comes from industry upstarts that have the funding to sustain operating losses for a considerable period of time while gaining scale and operational experience.

The new kid on the block in automotive retailing is Carvana, an upstart founded in 2013 that sells automobiles entirely online. CarMax has enhanced its online presence significantly in recent years, but the company continues to maintain an extensive network of retail locations. While CarMax management considers this “omni-channel” approach to be a competitive advantage, Carvana has been able to eliminate the significant cost of running a network of dealerships.

CarMax is a highly profitable company with a long history of sound financial results. Carvana, which went public in 2017, is the polar opposite with a history of losses and shaky financials. However, Carvana has been growing rapidly in order to achieve the scale that its management believes will eventually lead to profitability. After years of rapid growth, Carvana became the second largest used car dealer in 2021.9

Andy Grove, the longtime CEO of Intel Corporation, wrote a book entitled Only the Paranoid Survive in which he discussed the importance of management taking aggressive actions to deal with strategic inflection points. Are used car buyers ready to abandon the opportunity to test drive cars at retail dealerships and make purchases entirely online? If so, a network of retail locations might become an albatross for CarMax in the long run, ruining the company’s economics.

This profile of CarMax is divided into the following sections:

- Used Vehicle Economics. Discussion of the industry’s size, fragmentation, recent trends, basic economics, and growth opportunities. The Automobile Industry, published on August 4, provides general industry background.

- Operating History and Business Model. Review of long-term operating results and recent trends. The CarMax business model involves selling to consumers at retail, liquidating inventory unsuitable for retail sale through a wholesale auction process, and financing retail purchases through CarMax Auto Finance.

- Balance Sheet and Capital Allocation. CarMax generates significant free cash flow, much of which has been dedicated to share repurchases, with share count declining by nearly 30% over the past decade. In 2021, CarMax acquired Edmunds, a well-known consumer-oriented vehicle research website.

- Growth Opportunities and Risks. Fragmentation of the used car market provides opportunities for further expansion while online-only competitors such as Carvana pose significant risks.

Used Vehicle Economics

CarMax is the largest retailer of used vehicles in the United States, but the company still has a relatively small share of the overall market due to the highly fragmented nature of the industry. At the end of 2021, there were more than 18,000 franchised dealerships operating in the United States. These dealerships sell the majority of late model used vehicles. The following excerpt is from the fiscal 2022 CarMax 10-K:

“Based on industry data, there were approximately 42 million used cars sold in the U.S. in calendar 2021, of which approximately 23 million were estimated to be age 0- to 10-year old vehicles. While we are the largest retailer of used vehicles in the U.S., in calendar 2021, we estimate we sold approximately 4.0% of the age 0- to 10-year old vehicles sold on a nationwide basis, an increase from 3.5% in calendar 2020. We estimate we sold approximately 4.9% of the age 0- to 10-year old vehicles sold in the current comparable store markets in which we operate in calendar 2021, an increase from 4.3% in 2020.”

CarMax’s management has set a goal to increase its share of the 0-10 year old share of the used car market on a nationwide basis to 5% by 2025.10

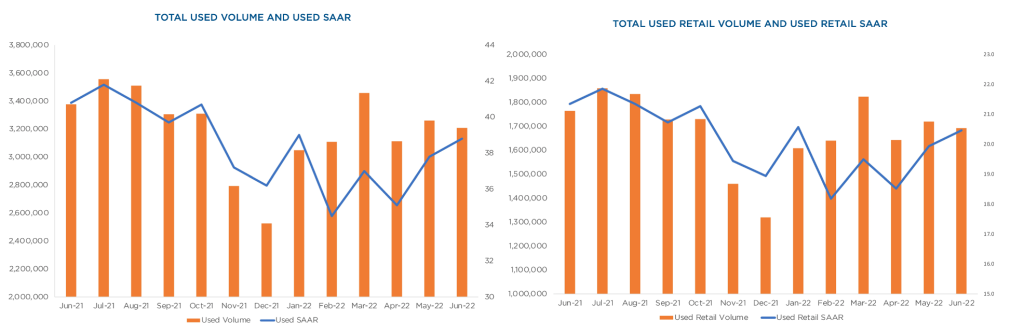

Used car sales volume has decreased recently. There were 38.2 million used vehicles sold between July 2021 and June 30, of which 20.1 million vehicles were sold at retail. On a seasonally-adjusted annualized basis, the pace of sales in June was 38.8 total used vehicle sales and 20.5 million retail used vehicle sales.11

In the exhibit below, the graph on the left shows total used units and the seasonally adjusted annual rate of sales (SAAR) while the graph on the right shows the same data restricted to retail units sold through dealerships. The left axis of each chart corresponds to monthly units while the right axis is the SAAR in millions of units.

Slightly more than half of used vehicles are sold at retail while the remainder represent transactions between private parties. Used car dealerships compete with each other as well as private-party sellers when it comes to acquiring inventory and selling vehicles to customers.

The attraction of a private-party transaction is that the margin captured by a used car dealership is avoided. This savings is typically shared by the seller and the buyer in a proportion that depends on the negotiating ability of each party to the transaction. The downside of transacting privately is that it is more time consuming for both the buyer and the seller, it can be unpleasant for people uncomfortable with haggling, and the level of real and perceived risk is much higher.

As an example of the economics of used cars at a micro-level, let’s take the case of a 2008 Ford Mustang GT, a vehicle I purchased new and drove for six years before selling it in 2014. In “clean” condition with 130,000 miles, Edmunds makes the following appraisal of the car’s current market value:12

- Trade-in value: $6,082

- Private party value: $7,219

- Dealer retail value: $9,083

Obviously, if a buyer and seller can find each other and negotiate a deal, they are both better off than if they transact with a dealership. The seller gets about $1,200 more for the car and the buyer saves about $1,800. However, the two parties have to find each other, negotiate with each other, and ultimately have some level of trust in each other.

Rather than going through the process of listing a car for sale, allowing strangers to test drive the car, negotiating a deal, and trusting that the buyer’s check will clear, the seller could decide to forego the potential $1,200 savings and trade it in.

From the buyer’s perspective, going to a dealership might seem less risky, especially if some kind of warranty is provided, even of very limited duration. Doing business with a dealership like CarMax does not require negotiating over the price and, in normal times, there is likely to be plenty of inventory to choose from. Those advantages could easily be worth $1,800 to the busy and risk averse buyer who needs financing.

The value proposition of using a dealer can be even greater for someone trading in their car for a newer model. The trade-in of the current vehicle, the purchase of a newer vehicle, financing, and warranty protection can all be arranged quickly and easily without the hassle and risk of engaging in two private-party transactions.

From the perspective of a dealership, sourcing vehicles from private parties is a relatively cheap way to obtain inventory for resale. If a vehicle appears to be in good enough shape to sell at retail, the dealership will spend some money to recondition and inspect it prior to selling it. The dealership’s gross margin is the price it is able to sell the vehicle for less the cost of acquisition and reconditioning. Vehicles falling short of retail standards will normally liquidated through an auction.

Earning a gross margin on each vehicle sold is only one part of the economics of used car retailing. For most consumers, buying a car is a large expense that requires financing. While many consumers may arrange for financing with their own bank or credit union, it is common for dealerships to arrange financing for customers. In addition, retailers typically earn commissions or profit sharing revenues from selling extended warranties as well as guaranteed asset protection (GAP) plans that cover the unpaid balance of an auto loan in the event of a total loss.

Since the used car market is so large and fragmented, auto retailers have many plausible strategies for gaining market share. Within existing geographical markets, an auto retailer can attempt to compete more effectively with other retailers as well as gain share at the expense of private-party transactions. Expansion into adjacent geographic markets is also possible for retailers with sufficient capital and a proven business model.

Operating History and Business Model

Before we take a deeper dive into the key drivers of CarMax’s business, let’s briefly examine the company’s overall operating history. The company operates in two segments: CarMax Sales Operations and CarMax Auto Finance.

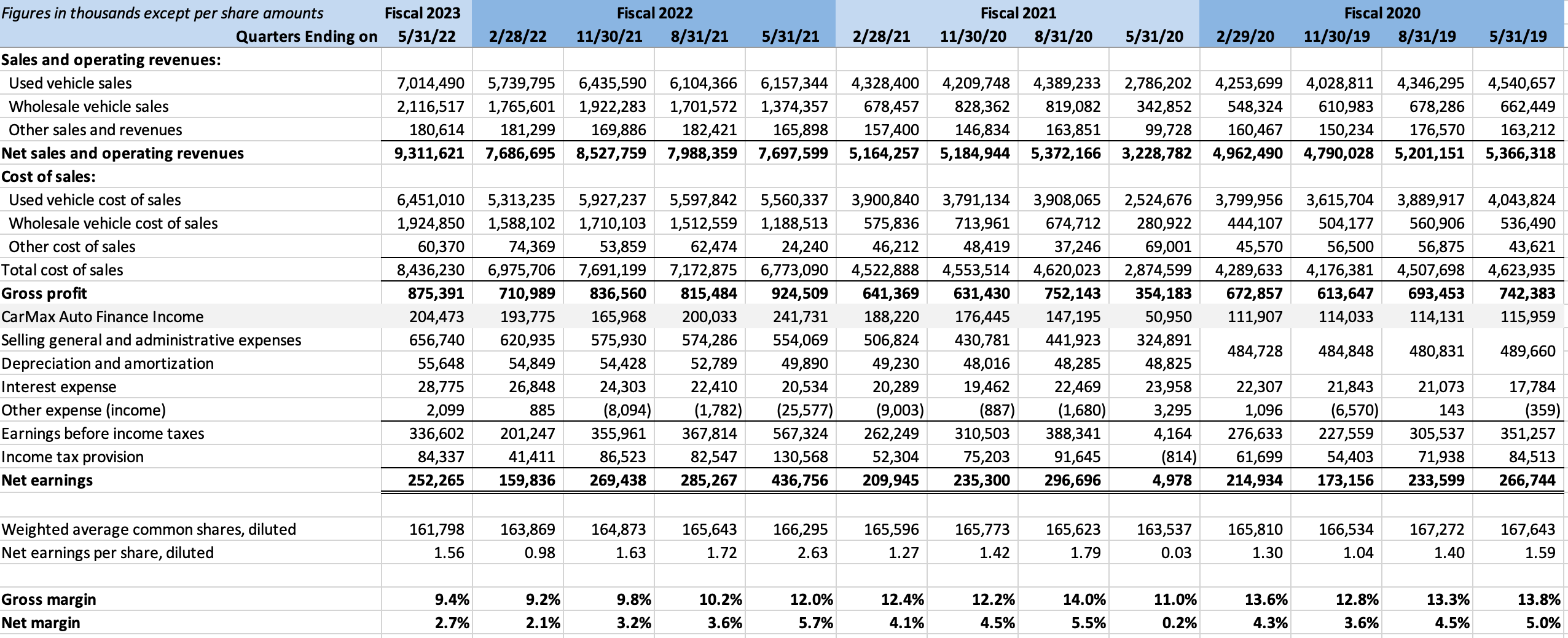

The following exhibit shows the income statement over the past decade:

Due to significant recent changes in the industry due to the pandemic, it is also helpful to look at recent trends on a quarterly basis. Note that the effects of the pandemic were felt starting in fiscal 2021 which began on March 1, 2020. Fiscal 2020 covers March 1, 2019 to February 29, 2020 and was unaffected by the pandemic.

From these high level summaries, I would make the following general observations before we take a closer look at segment results:

- From fiscal 2013 through fiscal 2020, CarMax exhibited steady growth. Sales revenue increased from $11 billion in fiscal 2013 to $20.3 billion in fiscal 2020, net income increased from $434.3 million to $888.4 million, and net income per share increased from $1.87 to $5.33 due to higher net income and a decreasing share count due to stock repurchases.

- Business boomed in fiscal 2022 with revenue increasing by 68.3% and net income increasing by 54.1%. Revenue was boosted by a combination of higher unit volume coupled with dramatically higher prices in the retail and wholesale channels due to rapid inflation in the price of used vehicles.

- Gross and net margins were quite stable from fiscal 2013 to fiscal 2020 and held up in fiscal 2021. However, rapid used vehicle inflation in fiscal 2022 pressured margins significantly and this has continued in the first quarter of fiscal 2023.

- CarMax Auto Finance income increased from $299.3 million in fiscal 2013 to $456 million in fiscal 2020 representing relatively stable growth before increasing to $562.8 million in fiscal 2021 and $801.5 million in fiscal 2022. The segment has experienced tailwinds from growth in the loan portfolio coupled with higher recovery rates when vehicles are repossessed and sold at auction.

CarMax Sales Operations

The majority of CarMax’s sales operations segment revenue (76.6% in FY22) comes from selling used vehicles to consumers through retail channels. In the past, the company had a small amount of revenue from selling new vehicles, but the last new car franchise was sold during fiscal 2022. Wholesale revenue (21.2% in FY22) represents the company’s auction business in which vehicles that do not meet retail standards are liquidated. Other sales revenue (2.2% in FY22) represents sales of extended warranties and GAP protection plans sold to consumers.

The following exhibit displays the number of vehicles sold, average selling prices, gross profit per vehicle, and gross margin percentages over the past decade. We can spot the recent rapid inflation in the retail and wholesale markets which we will drill into shortly. Gross margin has traditionally been greater in the wholesale channel, although wholesale margins have recently compressed:

The primary drivers of the CarMax business model involves sourcing inventory, selling vehicles through retail channels, selling vehicles at wholesale auctions, and arranging financing for customers. Let’s take a brief look at each of these activities.

Sourcing Inventory

The business model of any used automobile retailer must start with a strategy to source inventory at a cost that allows for a sufficient gross margin to be earned from retail sales. The availability of used vehicles depends on a number of factors including the size of the vehicle fleet, the number of new vehicles sold in a given year, and the propensity of consumers to want to upgrade to newer models.

In general, it is advantageous to source inventory directly from customers rather than to rely on wholesale auctions. CarMax refers to the percentage of vehicles sourced from customers as its self-sufficiency rate which stood at 70% in fiscal 2022 and remained at that level in the first quarter of fiscal 2023. Historically, the self-sufficiency rate has been in the 36-41% range. CarMax credits improvements in instant online appraisals for improving self-sufficiency.

Anyone can sell their vehicle to CarMax regardless of whether they are buying a vehicle from CarMax. For many customers, this entire process can be accomplished by answering an online questionnaire which results in an instant online quote.

On June 1, 2021, CarMax acquired Edmunds, a well-known resource for consumer research. Edmunds has long offered users an online appraisal tool. As I verified recently, CarMax has integrated its inventory acquisition process with Edmunds. In fact, the “path of least resistance” when using the Edmunds appraisal tool is to obtain an instant offer from CarMax which could further increase the self-sufficiency rate.13

In addition to sourcing inventory from consumers, CarMax buys vehicles from wholesalers, other dealers, and fleet owners including leasing and rental companies, but this inventory generally comes at a higher cost. To the extent that CarMax can maintain its self-sufficiency rate at the recent level of ~70%, this could represent a tailwind for gross margins going forward.

Retail Sales

In the four fiscal quarters that ended on May 31, 2022, CarMax sold 894,489 vehicles to consumers via its retail sales channel. In recent years, an increasing percentage of CarMax’s sales have originated through its website and mobile app. The company’s omni-channel strategy is intended to provide consumers with a seamless integration between shopping for a vehicle online and at retail locations.

All vehicles sold at retail are “CarMax Qualified Certified” which excludes inventory with salvage titles as well as flood or frame damage. No vehicles are sold to retail customers on an “as is” basis. To reduce the level of risk to customers, CarMax offers a 24 hour test drive with a limit of 150 miles. Additionally, the “Love Your Car Guarantee” allows customers to return any vehicle within thirty days with a limit of 1,500 miles. All vehicles come with a 90 day/4,000 mile limited warranty and extended warranty options are offered at additional cost. In combination, these policies reduce the real and perceived risk of purchasing a vehicle from CarMax.

In the latest fiscal quarter, 11% of CarMax retail sales were entirely online and 54% were omni-channel where consumers utilized online functionality as well as the services provided by retail locations.14

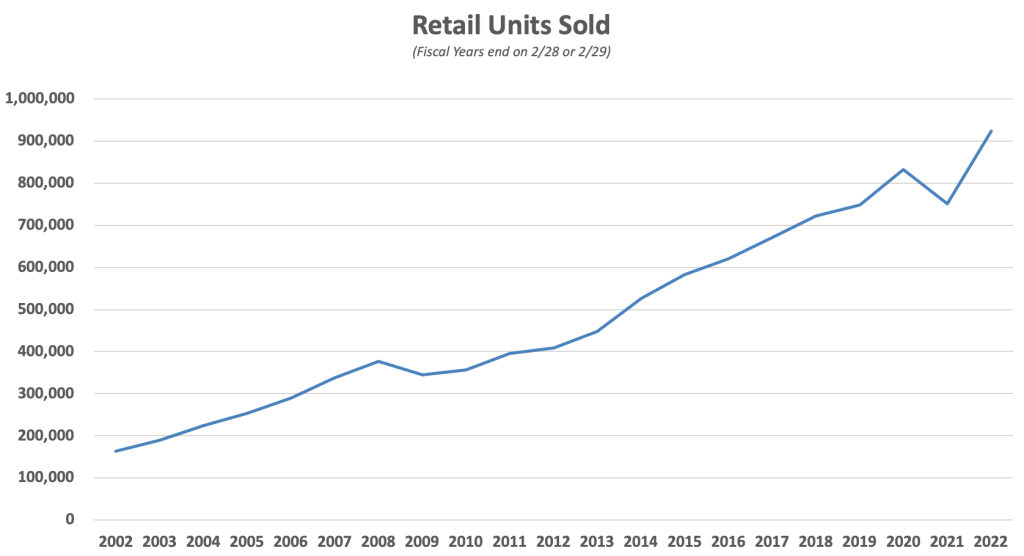

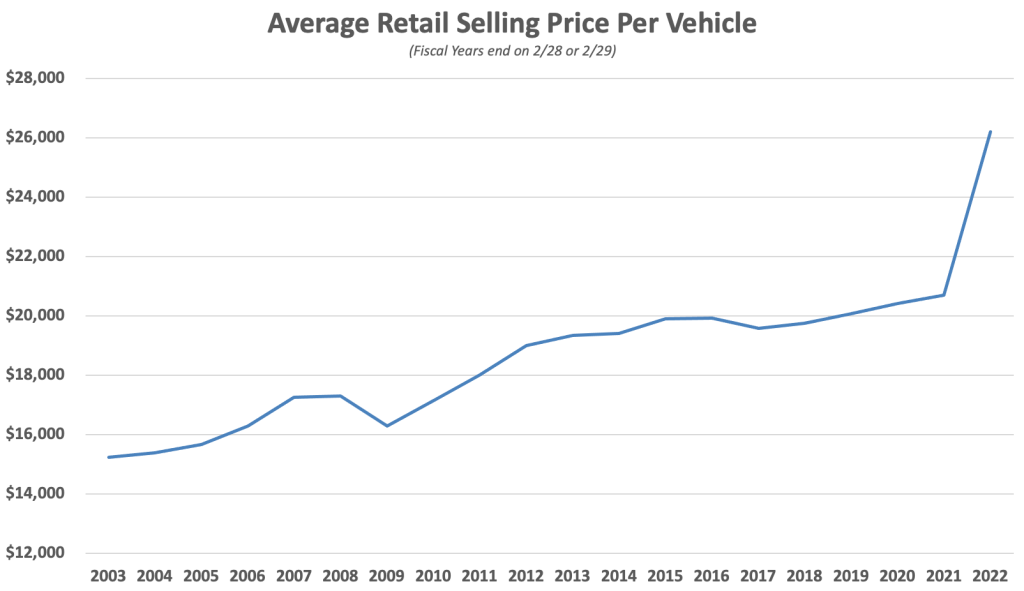

The exhibits below show the number of retail units sold and the average sales price per unit over the past two decades:

Gross margin represents the difference between the price a vehicle sells for and the cost of acquiring and reconditioning prior to sale. Over the past decade, gross margin per vehicle has been in the $2,000 to $2,200 range. During that period, used vehicle prices rose only slowly and gross margin as a percentage of selling price declined gradually from 12% in fiscal 2011 to 10.2% in fiscal 2021. During fiscal 2022, prices increased significantly. Gross margin as a percentage of selling price declined to 8.4% even as gross margin per-unit in dollar terms reached a record high.

The following exhibit shows retail gross margin on a per-unit basis, both in dollar terms and as a percentage of average selling price:

It is not a good idea to draw too many inferences from a single year, particularly during very volatile periods. Gross margin percentage was low in fiscal 2022 and fell further to 8.1% in the first quarter of fiscal 2023 which ended on May 31, 2022. During the latest earnings call, management appeared to focus more on gross margin per unit which was at a record high and stressed the need to keep vehicles as affordable as possible for consumers in an inflationary environment. It remains to be seen if or when CarMax will restore gross margin percentage to the 10-12% range.

Wholesale Auctions

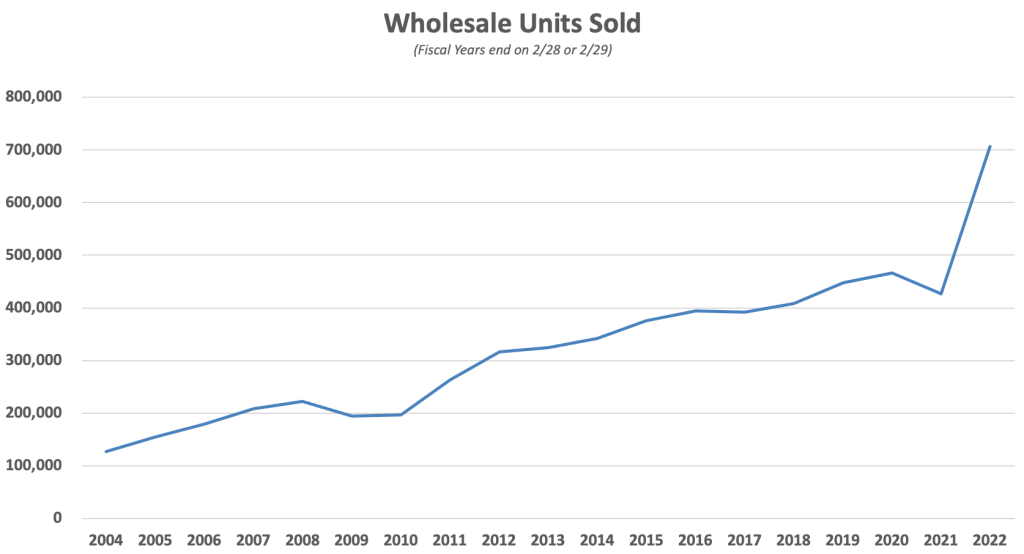

Many vehicles purchased by CarMax are unsuitable for sale to retail customers due to age, high mileage, poor condition, or a history of frame or flood damage. Vehicles that are not candidates to be sold at retail are liquidated at wholesale auctions. In the four fiscal quarters that ended on May 31, 2022, CarMax sold 711,130 vehicles at wholesale.

The typical vehicle sold at a wholesale auction is over ten years old and has more than 100,000 miles. Whether to sell inventory at retail or wholesale can be a judgment call. Recently, management sold some vehicles at retail that might have been liquidated through auctions in the past. This was done to meet demand for lower-priced vehicles as inflation made CarMax’s retail inventory much more expensive.15

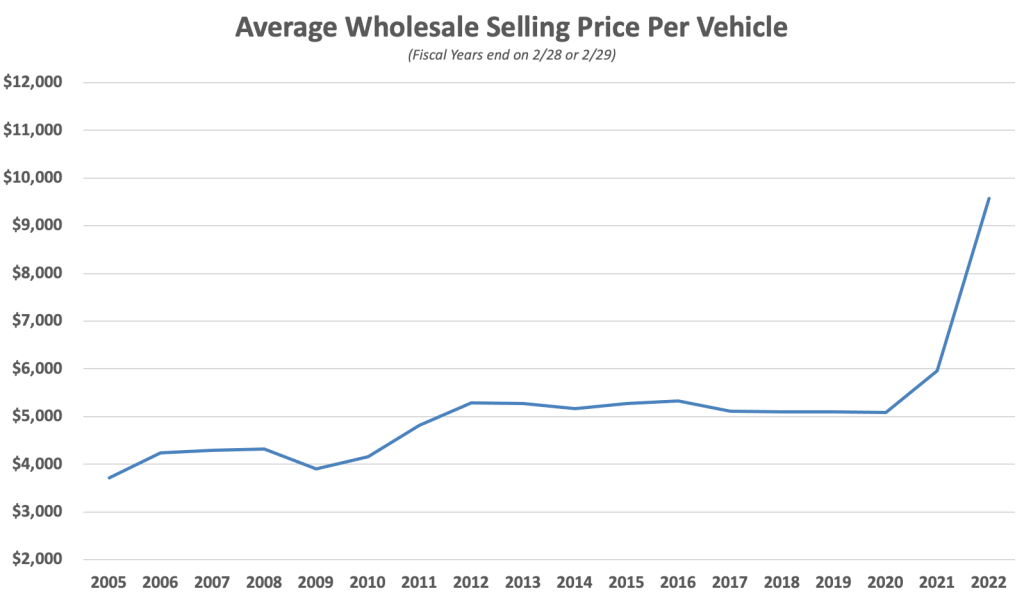

The exhibits below show the number of wholesale units sold and the average sales price per unit since 2005:

The trends we have seen at the retail level are even more extreme in the wholesale channel. In Fiscal 2022, wholesale units sold increased by 65.7% while the average selling price per vehicle rose by 60.8%. At the beginning of the pandemic, CarMax switched all of its auctions to an online-only format. At this point, all auctions are still being held in a virtual online format.

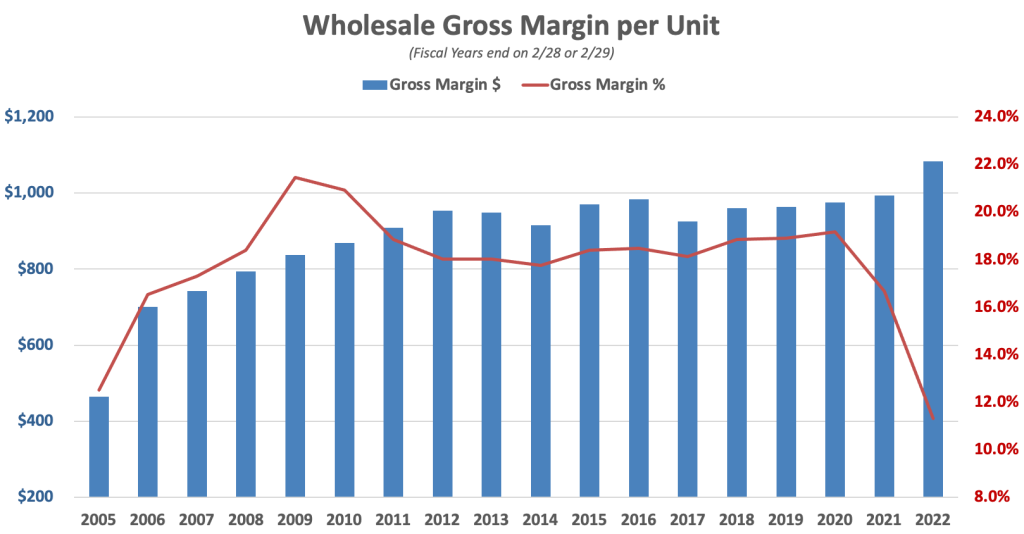

The following exhibit shows wholesale gross margin on a per-unit basis, both in dollar terms and as a percentage of average selling price:

We can see that gross margin dollars are at a record high on a per-vehicle basis, but gross margin as a percentage of average wholesale selling price is running at levels far below the level of the 2010s. From a review of management’s comments, it appears that they are primarily targeting gross margin dollars per unit for both the retail and wholesale channels. It is not clear if or when the wholesale gross margin percentage will return to the 18-20% range that prevailed during the 2010s.

CarMax Auto Finance

Since the majority of customers shopping for a vehicle cannot pay cash for the purchase, providing easy and competitive financing is an integral part of operating in the retail channel. The auto finance industry is comprised of banks, captive finance divisions of new car manufacturers, credit unions, and independent finance companies. CarMax Auto Finance (CAF) primarily competes with banks and credit unions that offer direct financing to customers who are purchasing used vehicles.16

CAF income is derived from interest and fee income from the $15.8 billion portfolio of receivables, less interest expense paid on the debt used to fund the portfolio, a provision for estimated loan losses, and direct expenses. At the end of fiscal 2022, CAF serviced 1.1 million accounts. During fiscal 2022, CAF financed 42.6% of retail used vehicle unit sales, a metric known as the penetration rate.

Customer applications for credit are initially reviewed by CAF. Applications that are declined or conditionally approved by CAF are then evaluated by third-party finance providers. When an application is referred to a third party provider, CAF is either paid or pays a fixed fee per contract. “Tier 2” providers pay a fee to CAF while “Tier 3” providers receive a fee from CAF. Tier 3 providers serve customers with low credit scores and CAF is willing to pay a fee to facilitate their financing because it provides incremental retail sales that would otherwise not occur. Regardless of whether a loan is retained or referred to another provider, CAF services all loans it originates.

The following exhibit shows key metrics for CAF over the past decade:

Key observations:

- Total managed receivables is the size of the overall loan portfolio, whether retained by CAF or referred to third-party provider. Managed receivables have nearly tripled over the past decade.

- Net loans originated and vehicle units financed gives us a picture of the percentage of vehicle sales that CarMax is financing through CAF each year and the approximate amount of financing per vehicle. The penetration rate has been relatively stable over time.

- The weighted average contract rate line indicates that the interest rate charged on the overall portfolio has been increasing and recently reached 9%. The margin between the weighted average contract rate and CAF’s funding costs for securitizations influences CAF income as a percentage of average managed receivables which was 5.6% in fiscal 2022 and has been on an uptrend.

- Credit scores, loan-to-value, and term. The weighted average credit score is around 700 which is considered to represent fair to good credit. The loan-to-value ratio is the amount of the loan relative to the selling price of the vehicle. This figure hovered around 95% for many years but has recently dipped below 90%, indicating more conservative underwriting. The weighted average loan term has held steady in the 65-66 month range.

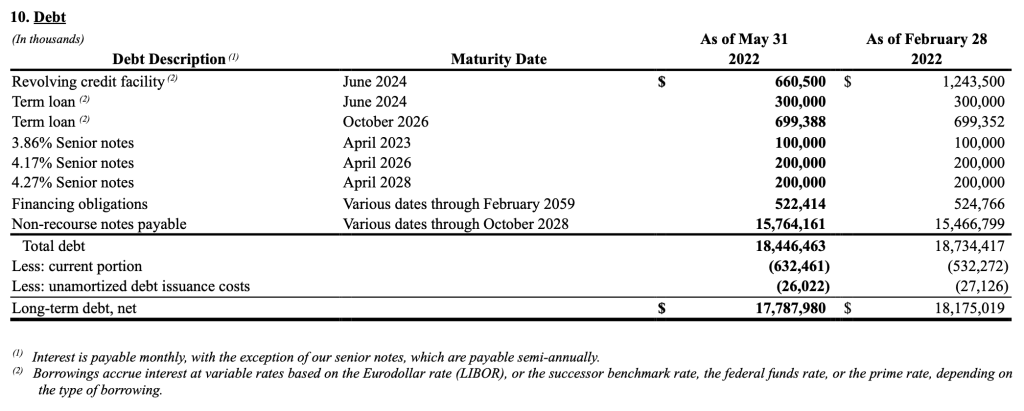

CAF auto loan receivables are primarily funded through securitization transactions that are structured to legally isolate the auto loan receivables. Investors in the non-recourse notes have no recourse to CarMax assets beyond the securitized receivables plus the amounts on deposits in reserve accounts and restricted cash held by CAF. In addition to securitization, CAF has access to warehouse facilities to fund non-recourse notes. As of May 31, 2022, there were $15.8 billion of non-recourse notes payable related to securitizations.

While the mechanics of CAF are complex, we can draw some conclusions based on the data and CarMax’s history over the years. First, it is apparent that CAF is integral to CarMax’s ability to successfully sell cars through the retail channel. Given the fact that most customers require financing, it is critical to have a financing unit capable of either funding loans directly or referring customers to a third party. Second, securitized funding is very important to CAF’s operations. Auto loan receivables have grown significantly in support of the company’s overall expansion and funding for these receivables must continue to be available to facilitate future growth.

The inflation of used vehicle prices coupled with growing unit volume has led to an increase in auto loan receivables and a commensurate increase in securitizations. Continued access to the securitization market is critical for CarMax’s business model.

One side-effect of the recent price appreciation of used vehicles is that fewer customers are “upside-down” on their loans at any given point in time, meaning that it is less common for customers to owe more on their loan than the value of their vehicle. This has increased the average recovery rate when vehicles are repossessed and reduced loan losses. The array of stimulus programs, including direct payments to individuals, also ameliorated the negative effects of the brief pandemic recession.

Balance Sheet and Capital Allocation

The following exhibit is a condensed version of the CarMax balance sheet over the past decade which displays key accounts:

CarMax carries significant debt, but it is important to note that the largest liability is represented by non-recourse notes which approximate the level of net auto loan receivables, as discussed more fully in the CAF section above. Other debt consists of a revolving credit facility, term loans, and senior notes. The composition of CarMax’s debt is shown in the exhibit below:

CarMax has produced significant free cash flow over the years but has not paid a dividend. Instead, the company has been a regular repurchaser of its shares, as we can see from the declining share count over the past decade. Share count stood at 159.6 million on May 31, 2022, down from 225.9 million on February 28, 2013.

In order to understand CarMax’s cash generation capabilities, we need to address a technical issue related to how changes in auto loan receivables and changes in the securitizations supporting those receivables are categorized. In the company’s consolidated statement of cash flows, changes in auto loan receivables are treated as cash flows from operating activities whereas changes in non-recourse notes payable funding those receivables are treated as cash flows from financing activities.

In my opinion, we need to consider changes in non-recourse notes payable to be operating cash flows, netted against changes in the auto loan receivables portfolio, as these are essentially both operating activities for CAF and the notes payable are non-recourse beyond the auto loan receivable portfolio and restricted cash.

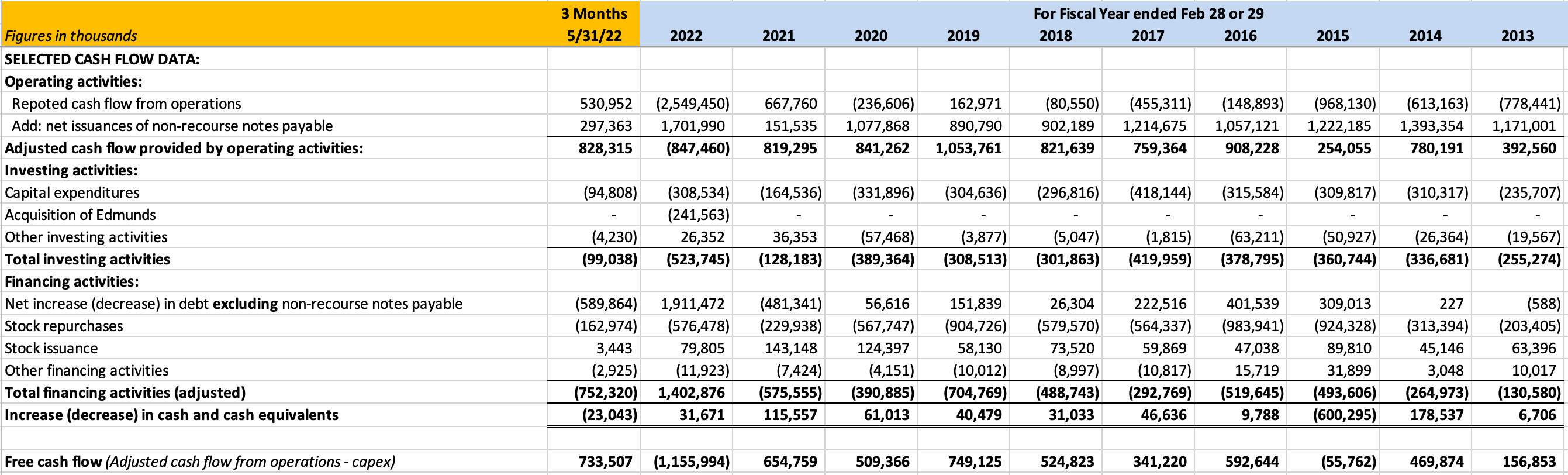

In the exhibit below, I show cash flow from operations, as reported under GAAP, along with an adjusted cash flow from operations incorporating the adjustment.

In the interest of conservatism, my free cash flow estimate deducts the full amount of capex from adjusted cash flow from operations even though a portion of capex is attributable to expansion of retail stores over the years. In fiscal 2022, CarMax made its first-ever acquisition when it purchased Edmunds for $241.6 million.

We can see strong free cash flow generation over time with the exception of fiscal 2022. During fiscal 2022, inventory increased by nearly $2 billion due to a combination of rapid inflation in used vehicle prices and to support higher sales volume. This increase in inventory was funded by taking on additional long-term debt. As I noted in my article on the automobile industry earlier this month, the rate of inflation in used vehicle prices has decreased in recent months. However, if there is another bout of high inflation in used vehicles, free cash flow could be negatively affected.

From fiscal 2013 through the first quarter of fiscal 2023, CarMax generated $3.5 billion of estimated free cash flow while long-term debt increased by $2 billion. During this period, the company used $6 billion to repurchase shares and raised $788 million through new stock issuance. In April, CarMax’s board expanded its share repurchase program by an additional $2 billion.17

Although not specific to CarMax, I should note that a new 1% excise tax on stock repurchases will take effect in 2023. It is unlikely that a 1% tax will change management’s calculations regarding returning cash via repurchases. However, the tax does slightly reduce the advantage of returning cash to shareholders via repurchases rather than dividends. CarMax has never paid a cash dividend.

Growth Opportunities and Risks

CarMax is the largest retailer of used vehicles in the United States but has a relatively low market share due to the fragmented nature of the industry. The primary ways to achieve growth are to increase market share in regions where the company already operates and to move into new markets. For example, in fiscal 2023, the company plans to move into the New York City metro area by opening three retail stores.

Management is forecasting growth over the next three fiscal years. CEO Bill Nash made the following remarks during an earnings call on April 12, 2022:

“We’re revising our FY ‘26 targets to reflect a range of 2 million to 2.4 million combined units with revenue between $33 billion and $45 billion. These ranges reflect the macro factors we had earlier that could result in ongoing volatility in consumer demand and vehicle pricing. In regard to market share, I’m excited for the future and confident that we will expand it beyond 5% by the end of calendar 2025.”

Although CarMax has a proven model and has been increasing its online capabilities significantly in recent years, to the point where customers can purchase a vehicle entirely online and have it delivered without ever setting foot in a dealership, there is a potential for disruption due to online-only rivals.

Assessment of the risk level of online-only competition is subjective and may involve generational differences in consumer behavior. From my perspective, buying a vehicle is something that most people do rarely. For example, in the 33 years since I obtained a driver’s license, I have owned five vehicles. Other than buying a home, purchasing a vehicle is typically the most significant transaction most consumers will make and part of the reason it is intimidating is because it happens rarely.

Consumers typically dislike purchasing a vehicle because it is an unpleasant and time consuming hassle. By removing the haggling from transactions and making pricing transparent for trade-ins, the cost of a vehicle, and financing, CarMax has eliminated most of the pain points consumers hate about car shopping while also making it possible to see and test drive a vehicle in person before making a purchase. To me, this seems like the best of both the online and physical worlds.

It is true that Carvana offers consumers a seven-day money back guarantee and permits buyers to take a car for a short test drive before accepting delivery. However, CarMax offers the ability to see the vehicle in person, to take it for an overnight “test drive” before making a purchase, and allows returns for the first thirty days.

I have reviewed the CarMax and Carvana websites and find them similar in terms of being able to view inventory and take initial steps to make a purchase. A customer can execute the transaction online with both CarMax and Carvana, but with CarMax has the additional option of visiting a dealership to see and drive the vehicle in person before making the purchase. If a typical consumer buys a car every five or six years, it doesn’t seem like a huge issue to go into a dealership as a final checkpoint. In fact, providing that option seems like a strong competitive advantage for CarMax.

It must be noted that many transactions that initially seemed implausible to complete online have, in fact, moved online over the past two decades. If younger generations feel comfortable purchasing vehicles sight-unseen, then retailers that lack a physical retail presence could have a cost advantage. However, it is important to understand that online-only automobile retailers must still maintain inventory and operate reconditioning facilities. Carvana also maintains “vending machines” that allow customers to pick up vehicles rather than have them delivered.

A secondary risk involves automated vehicles. Greater automation, including the ability of a car to drive itself most of time, could dramatically change the way in which individuals interact with vehicles. It is plausible to believe that private vehicle ownership will decline especially in urban and suburban locations. Large fleets of automated vehicles could transport people to their destination efficiently. It would no longer be necessary for individuals to incur the significant cost of vehicle ownership and having an expensive asset sit idle 95 percent of the time. However, despite Elon Musk’s aggressive claims, full automation of the vehicle fleet in the United States seems unlikely to occur for well over a decade, if not much longer.18

Conclusion

CarMax disrupted the used vehicle market and grew rapidly during the 1990s by reducing the major pain points facing consumers. As an independent, publicly traded company over the past twenty years, CarMax has provided shareholders with attractive long term returns in a tax efficient manner by avoiding dividends and returning capital via stock repurchases. Although the company is now the largest retailer of used vehicles in the United States, it is clear that the overall market is large enough for substantial future growth.

Management has taken the risk of online-only entrants seriously and now allows customers to complete the process of trading in a vehicle, purchasing a vehicle, and arranging financing entirely online. The omni-channel approach makes it possible to begin the process online and complete it at a retail location where vehicles can be seen and driven prior to making a final commitment. Given the rarity of purchasing a vehicle, it seems likely that most consumer will prefer to inspect and drive a five-figure purchase, although this might be a matter of generational preference.

At a market capitalization of $16.2 billion, the valuation is not particularly demanding given the company’s recent growth trajectory and trailing net income of $967 million over the past four fiscal quarters. The business model seems sound and sustainable, but investors need to avoid complacency and keep a close watch on consumer acceptance of online-only automobile retailers.

According to Alan Wurtzel, Circuit City was destroyed by hubris and complacency. CarMax is, in a sense, the surviving “child” of Circuit City and its management must remain alert to the risk of disruption to its own business model in the future.

Downloads

A PDF file containing this profile can be downloaded by using the link below:

Excel data used in this report is now available using the link below:

Copyright, Disclosures, and Privacy Information

Nothing in this newsletter constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.

Your privacy is taken very seriously. No email addresses or any other subscriber information is ever sold or provided to third parties. If you choose to unsubscribe at any time, you will no longer receive any further communications of any kind.

The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

No position in CarMax.

- Circuit City Stores Fiscal 1996 10-K [↩]

- Circuit City Stores Fiscal 1997 10-K, Note 1 [↩]

- Circuit City Stores Fiscal 2002 10-K, CarMax Statement of Earnings [↩]

- Circuit City Stores Press Release dated October 1, 2001. [↩]

- The Rise and Fall of Circuit City by Jessie Romero, published in 2013, provides a brief history of the company. Also see ‘Undead’ Circuit City Won’t Rise If It Forgets What Killed It by Rodd Wagner, published in 2016, for some interesting details about the company’s history. [↩]

- Store count retrieved from https://www.carmax.com/stores on August 13, 2022. [↩]

- All financial data comes from the CarMax’s SEC filings. CarMax operates on a non-standard fiscal year which ends on February 28 or 29. The figures cited are for the four fiscal quarters that ended on May 31, 2022. Total vehicles sold of 1,605,619 during this period were comprised of 894,489 vehicles sold at retail and 711,130 sold at wholesale via auctions. [↩]

- Alan Wurtzel wrote a history of Circuit City, From Good to Great to Gone, which was published in 2012. I have not read the book but have added it to my list. [↩]

- Carvana’s 2021 10-K, Business Description, p. 14 [↩]

- CarMax CEO Bill Nash’s Fiscal 2022 Letter to Shareholders [↩]

- Estimated Monthly Used-Vehicle SAAR and Volume published by Cox Automotive on July 15, 2022. The figures for July 2021 to June 2022 were taken from a data download retrieved on August 14, 2022. [↩]

- Edmunds is a leading online resource for automotive research which was acquired by CarMax in 2021. The Edmunds “true market value” appraisal feature has a good reputation for accurately estimating used car values. [↩]

- If anything, the CarMax integration with Edmunds might be a little too complete. I had to go through a couple of extra steps to obtain a “true market value” estimate without asking for a CarMax instant offer. There is a risk that consumers will no longer view Edmunds as a trustworthy source of objective data if the integration with CarMax becomes too aggressive. [↩]

- CarMax Fiscal Q1 2023 earnings call, June 24, 2022. [↩]

- CEO Bill Nash: “Wholesale volume was also pressured by our decision to reallocate some older vehicles from wholesale to retail to meet consumer demand for lower price vehicles.”, Fiscal Q1 2023 earnings call, June 24, 2022. [↩]

- For management’s perspective on CAF, I recommend reading the CarMax Lending Platform slides from the company’s virtual analyst day held in January 2022. [↩]

- CarMax Q4 2022 Earnings Call, April 12, 2022. [↩]

- In 2017, I wrote The Autonomous Vehicle Revolution to discuss some of these trends. If anything, over the past five years I have grown more skeptical of the prospects for automation to “revolutionize” vehicle ownership anytime soon. [↩]