The stock has dropped 45% since quarterly earnings were released a month ago. Is the business model still intact or has Mr. Market overreacted?

This article is a follow-up to a business profile of America’s Car-Mart published on June 8. Business profiles are meant to be stand-alone articles rather than companies that will be regularly “covered” on a quarterly basis. However, on occasion, I will publish business updates when there are interesting developments.

To keep updates relatively brief and informal, I will avoid repeating content that can be found in the original profile. Readers who are interested in America’s Car-Mart should read the profile before reading this update.

Car-Mart’s Volatile Stock

Stock prices tend to move around far more than underlying business fundamentals. That’s certainly true when it comes to America’s Car-Mart. The long-term operating history of the company shows variability but nothing like the gyrations of the stock. As we can see from the five year chart, recent stock price volatility is nothing new:

Car-Mart’s stock approximately quadrupled between its pandemic lows in early 2020 and its highs of 2021. This year, the stock mostly declined before rallying sharply when fiscal 2022 full year results were announced in May. But the market intensely disliked the company’s Q1 fiscal 2023 results which were announced on August 17 and the stock dropped ~45% over the past month.

Let’s try to unpack what’s going on by forgetting about the stock price and looking at recent business results.

Quarterly Results

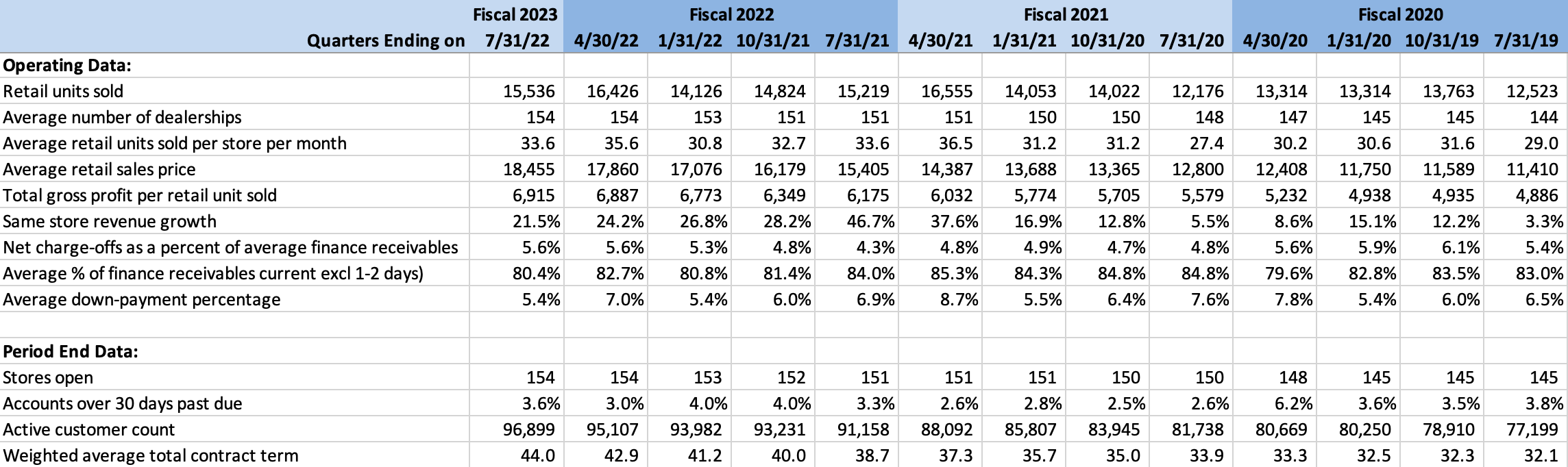

America’s Car-Mart’s fiscal year ends on April 30. The first quarter of fiscal 2023 ended on July 31, 2022 and the company released financial results on August 17. Rather than reiterating the narrative in the press release or looking at one quarter’s results in isolation, I decided to compile quarterly data for the past three fiscal years.

The following exhibit shows key operating metrics for Car-Mart since the quarter that ended on July 31, 2019. The purpose of presenting the data for three fiscal years is to see trends that took place prior to the pandemic as well as what has happened since.

Let’s drill down into several of these data points:

- Retail units sold exhibit seasonal tendencies with the third fiscal quarter normally being the slowest. However, we can see a clear uptrend in units sold over the course of the thirteen quarters in the exhibit. Although ten dealerships have been added over this period, units sold per dealership have also been in a general uptrend indicating increasing productivity.

- Average retail sales price has increased dramatically from $11,410 in the quarter that ended on 7/31/19 to $18,455 in the quarter that ended on 7/31/22. I wrote about the underlying trends in used car inflation in quite a bit of detail in The Automobile Industry which was published on August 4.

- Customers continue to pay with net charge-offs increasing moderately in recent quarters but close to levels that prevailed prior to the pandemic. Similarly, the average percentage of finance receivables that are current has remained within the historical range.

- Buyers are stretching further to buy cars due to prices rising dramatically. Down payments percentages are down, and contract terms are up. The average contract term rose from 32.1 months three years ago to 44 months for the latest quarter. However, the 30 days past due percentage is within its historical range.

- Car-Mart continues to add customers. There were close to 97,000 active customers at the end of the latest quarter compared to just over 77,000 three years ago. This is a dramatic improvement that was achieved with only ten additional dealerships, an indication of improving productivity.

Let’s take a look at the income statement over the same period:

A few observations:

- Gross margin has been under pressure due to used car inflation. Car-Mart’s buyers are strapped for cash and the company has been pricing competitively. However, as seen in the previous exhibit, gross margin per retail unit sold has been increasing. Management targets gross margin dollars, not gross margin percentage. Increasing car prices has led to gross margin percentage compression but gross margin dollars and interest income has increased.

- SG&A as a percentage of sales has been declining as the company has gained operating leverage. As mentioned in the original profile, if sustained this improvement in SG&A has the potential to drive significant improvement in operating margins over time.

- Net income declined on a sequential basis due to lower gross margin, somewhat higher SG&A, and a higher provision for credit losses. Variability in provision for credit losses is typical. The metrics to watch in terms of credit quality, shown in the prior exhibit, seem to be within the historical range.

Competing Narratives

Car-Mart managed the pandemic period and the sharp inflation of used car prices very well, all things considered. Retail units sold have increased from 12,523 in the 7/31/19 quarter to 15,536 in the latest quarter. Retail units sold per dealership per month has increased from 29.0 to 33.6 over the same period and management believes that this figure has the potential to rise to 40-50 per month. The average dealership is serving 629 customers and management believes this figure can rise to ~1,000.

Active customers have increased from ~77,000 to ~97,000 over a three year span that included tremendous challenges. My interpretation of the key operating data is that Car-Mart has proven that its value proposition is attractive to its core demographic base of lower income, credit challenged customers in rural areas and small towns.

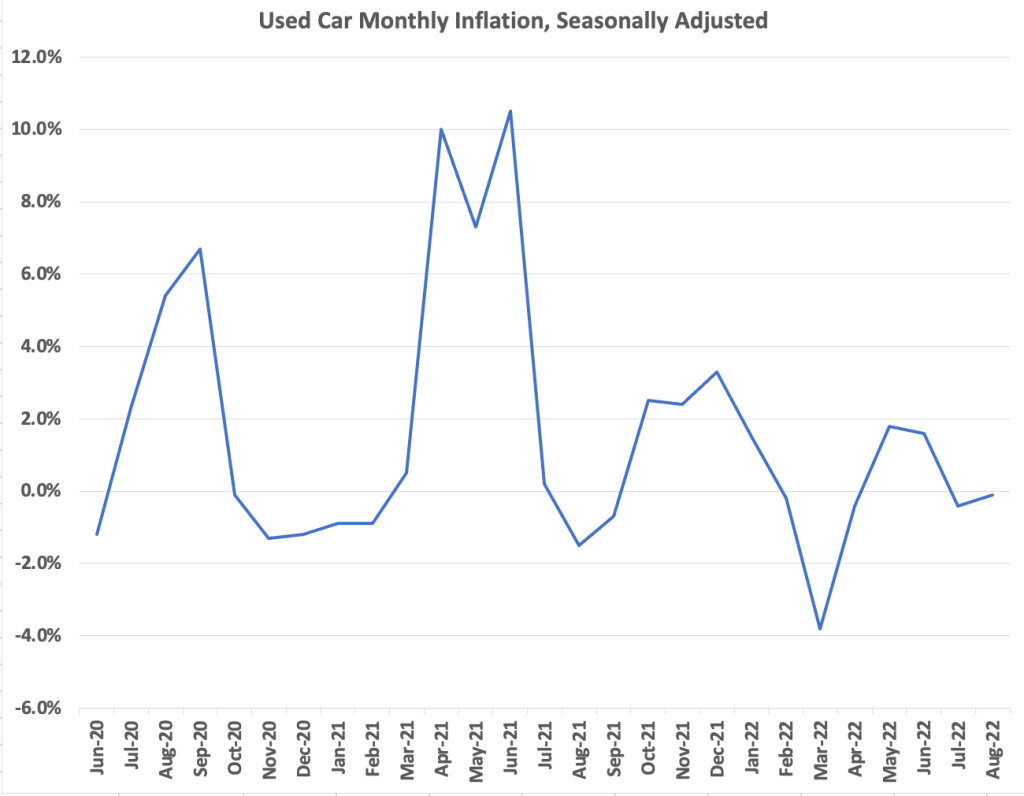

Despite what seem to be solid operating results, the market might be fearful of deflation in used car prices. The following chart shows inflation for new vehicles, used vehicles, and the CPI as reported by the BLS. These are annual figures for the trailing twelve months for each data point:

On a year-over-year basis, we can see that used vehicle inflation has come down dramatically. The following chart shows the month-over-month inflation for used vehicles and shows that there have been periods of used car deflation recently:

What are some of the problems that could occur in the used car industry if used car prices start to decline precipitously?

- Customer defaults could increase. Customers who are deeply “upside down” on their loans — that is, owing far more than the value of the vehicle — are more likely to default on loans.

- Recovery rates could drop. If defaults increase and more vehicles are repossessed, recovery rates might drop. In an environment of deflation, trying to sell vehicles that have been repossessed could add to a general glut further driving down prices.

What does management think about the prospect of deflation and the effect it would have on the business? The company made the following comments in February:

“While a potential rapid decline in used car prices is possible, we don’t believe that there will be a collapse in the values of cars that we purchase for our consumers. There has been an overall shortage of good, basic, affordable vehicles for well over a decade. In our opinion, there is solid and increasing market demand for these vehicles. However, deflation, all things being equal, would be good for our business and customers. We would be in a good position to capitalize on the volume opportunities this scenario would present. Our economics get better as prices decline and, relative to others in the industry, our recoveries on repossessions are a smaller percentage of our overall profitability.”

If management’s view is correct, deflation is not likely. But even if there is deflation, management believes that it would be a net positive for the economics of the business.

We obviously cannot take management’s view of the situation as gospel, but what they are saying is generally consistent with the nature of the company discussed in the full profile. Car-Mart sells basic transportation to a demographic that must have vehicles to get to and from work. These vehicles are not discretionary purchases.

The more significant risk for Car-Mart is a recession and high unemployment. In such an environment, Car-Mart’s customers will find themselves in financial distress and more of them will have no choice but to default. The full profile discusses these issues in more detail and includes data that encompasses the financial crisis, a period during which Car-Mart remained profitable.

Conclusion

With a market capitalization of $451 million, book value of $481 million, and a history of consistent profitability across varied economic conditions, Car-Mart presents a more compelling value proposition than when I published the full profile in early June. At that time, the market capitalization was $656 million.

To be sure, there are many risks in today’s macroeconomic environment. High inflation is causing the Federal Reserve to finally act by raising interest rates and the August CPI report earlier this week caused market participants to believe that the Fed will have no choice but to be more aggressive. If the Fed’s actions push the economy into recession, unemployment will increase. The combination of lingering high inflation and higher unemployment could produce a stagflation that would be especially harmful for Car-Mart’s lower income demographic.

Every investor has to assess which narrative is most plausible. Investing based on macroeconomic factors is very difficult which is one reason it makes sense to look for companies that have performed well over multiple economic cycles.

The reason I decided to profile America’s Car-Mart is because it has performed well over a long period of time through multiple cycles. So, from a long-term investor’s perspective, short-term declines in the stock could present an interesting opportunity.

Copyright, Disclosures, and Privacy Information

Nothing in this newsletter constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.

Your privacy is taken very seriously. No email addresses or any other subscriber information is ever sold or provided to third parties. If you choose to unsubscribe at any time, you will no longer receive any further communications of any kind.

The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

No position in America’s Car-Mart.